As we have all witnessed, the outbreak of the coronavirus in China and the subsequent global spread of the disease, has caused massive volatility in the world markets, including the U.S. stock market. The reason for this extreme volatility at this moment is that markets do not like uncertainty and react violently to uncertainty. This is not the run of the mill volatility in reaction to valuations and earnings reports.

In the history of the markets, disruptions have occurred intermittently over the years. These disruptions are painful and unsettling, and often cause investors to react out of fear to the unknown, causing them to liquidate their positions and gravitate towards cash. This can often have a long-lasting detrimental effect on their financial situation because they sell at a low and will have difficulty re-entering the market at higher prices when the market inevitably comes back with a vengeance in the future. Investors need to remember that markets have been the source of generous returns that have rewarded those who have persevered through disruptive market movement over time.

What is volatility?

Volatility refers to the pace at which prices of stocks move higher or lower, and how wildly they swing. Volatility is different from market risk. Risk is the probability that an investment will result in a permanent loss of capital. Without taking on some risk, there can be no return. When we invest in a stock, we are investing in a company and its earnings. Reported earnings and forward guidance from companies tell us what we should be looking for with respect to market direction regarding the company’s stock price.

The coronavirus will not validate or invalidate an individual company’s stock price, however, in the current environment, earnings fundamentals will not be the only driver of the markets. Earnings will be subject to distortions due to the disruption caused by the virus and resulting closures, transitory as they may be.

For a bit of recent historical context on market volatility, the following is a brief summary of the recent timeline:

- In 2018 the DJIA was down 5.6% and the S&P was down 9.08%.

- In 2019, the DJIA was up approximately 24% and the S&P was up approximately 33%.

- In January 2020 the month started off with gains and in mid-month, the expectation was that the DJIA would hit a historic 30,000.

- The last week in January saw several down days as fears of the coronavirus intensified, but the market ended up with the DJIA up 0.4% and the S&P up 0.3%. Equities were boosted by a string of impressive earnings reports that helped them look past their coronavirus fears.

- February was a mixed bag of up and down days ending the month with indexes down at least 10% in what is known as correction territory.

- March saw the same pattern with a few up days and then, of course, the DJIA entered a bear market on Friday, 3/13, followed by Monday, 3/16 seeing a 3000-point drop which is the worst point drop day in market history, and Tuesday, 3/17, seeing the market up 1049 points (at the time I am writing this).

So, as you can see it has been quite a roller coaster ride where fear of the unknown eclipsed good earnings reports or any other relevant good news because we are all facing an unfamiliar environment involving a global health situation while awaiting results of a proactive strategy and the cessation of the spread of the virus.

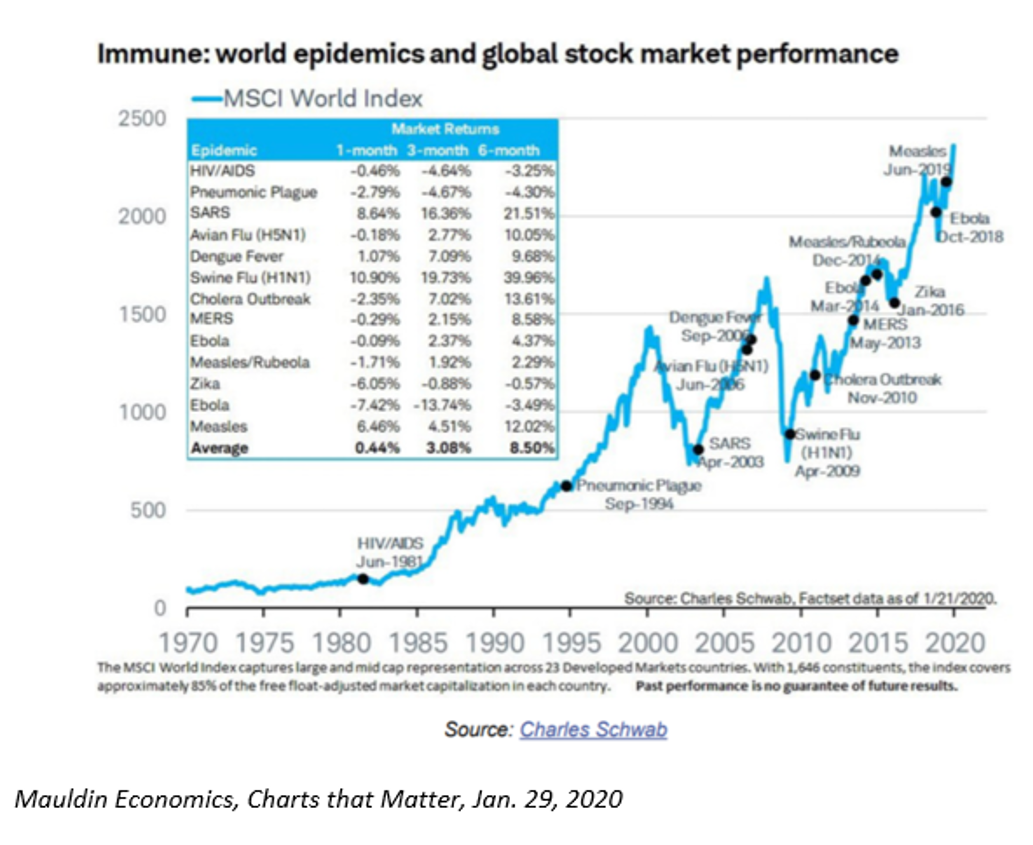

There have been crises over the years such as Brexit, trade issues, the Greece situation, oil issues, and other health scares such as Avian flu, SARS, Swine flu and Ebola with related market disruptions and subsequent market recoveries.

What is the current situation in the markets?

There is a confluence of factors occurring simultaneously to create the market activity we are experiencing. Due to a leveraged financial system, we are witnessing forced selling that occurs when positions are purchased with borrowed money. Margin and debt calls require a forced sale of assets to pay them, and that results in the sale of assets that aren’t distressed, i.e., good assets being sold, to pay the margin or debt. If one needs cash, they will sell the holdings they can make the most on, and are more sellable, and when enough people do that, it becomes a vicious cycle. Other factors include momentum selling which exacerbates intraday volatility and ETF activity which adds to the mayhem. Once the selling began, these factors magnified the outcomes.

What is being done to alleviate the situation?

- Monetary Policy

- The Federal Reserve has cut rates to 0%-25%, re-instituted quantitative easing (bond-buying program to keep financial markets running smoothly), announced a coordinated effort with five other central banks to make it cheaper for foreign banks to borrow U.S. dollars so they don’t become reluctant to transact with each other, encouraged banks to turn to the Fed’s discount window to borrow funds directly from the central bank and established a Commercial Paper Funding Facility to buy up the 90-day commercial paper. All of this is done to provide liquidity and functioning credit markets.

- Fiscal Policy

- A variety of measures are in the works including a request for $850 billion, extended tax filing deadline, direct support to the airline and hospitality industries, $1000 checks to married couples making $100K or less, and to single people making $50K or less, and payroll tax relief.

- Slowing/stopping the spread of the virus by social distancing, greater testing, and a national lockdown.

What future scenarios are possible?

Nobody can really predict the future but there are a few ways that this can play out.

- Most people agree that we did not enter this violent market reversal with an economy having the weakness of the 2008/2009 economy, hence we could have GDP contraction in Q2 and a rebound in late Q3-early Q4 due to the heavy fiscal and monetary support, with normalization by year-end.

- Worse case is GDP contraction in Q2 and Q3 with a slow recovery and a recession for 6-12 months.

- Best case is there is a Q2 GDP contraction, a sudden Q3 V-shaped rebound, the health damage is contained, and normalization occurs sooner rather than later.

What should we be focusing on as investors at this time?

It is prudent at this moment to keep to your investment strategy despite the temporary damage (which may last for longer than we like) and understand that fear and panic will lead to emotional decisions that will cost a lot of money over the long-term if an investor liquidates instead of showing discipline and rationality. For those who can withstand volatility and not vacillate from angst during disruptions, this could be a very good buying opportunity.

A well-diversified portfolio with equities, fixed income and alternative investments (uncorrelated investments to the market) is the prudent strategy for a more resilient portfolio. We believe in investing in the fundamental strength of companies by looking to their balance sheet, leverage ratios, and dividend-paying and dividend growth capacity. Dividend growth stocks will provide income even during market disruptions. Events such as the coronavirus can very well effect strong businesses in the short-term, but strong fundamentals will prevail over time.

Market timing is a fool’s errand as it is impossible to determine when to exit and re-enter at optimal times. If you are tempted to sell, what is the plan for re-entry, and does it make sense to re-enter at 10-20% higher prices? Better to invest in companies with strong fundamentals instead of being a stock speculator. There may be ebbs and flows in stock prices, but over the long-term time horizon stock price fluctuations will not impact the long-term trajectory of a company’s performance; look to enterprises that have the capacity for innovation, cash flow generation, and profitability

Investors should consider whether they would be bothered by markets rallying higher after they sell their positions resulting in permanent realized loss and not just a temporary paper loss. Is the volatility in the market causing them actual and realized economic detriment, or is it more anxiety caused by incessant media coverage? If you as an investor look to an extended timeline such as a year, which is a reasonable time horizon albeit even short, do you believe this will still be the situation in the market and are you prepared to incur permanent losses for a problem that will ultimately be resolved over time?

If you have a long-term plan, it is prudent during this uncertain time, to take a breath, keep to your strategy, and not make rash decisions motivated by fear. As with all things in life, this too shall pass, and, it is imperative that our view is long term.

Keep well.