The big idea and why it matters: Credit instruments can help serve different purposes, as they vary widely in risk, income, total return, liquidity, and pricing structures. Lending inherently involves risk, and embracing diversification while avoiding things that sound too good to be true is prudent.

“I’m in debt. I am a true American.” -Balki Bartokomous

Today, we are forging ahead on the quest to draw additional credit-market conclusions before moving into what is (in my experience) the most divisive asset class, private equity. On a throwback Thursday, who better than Perfect Stranger, Balki Bartokomous, to remind us in a joking way of the broad opportunity set the US debt/credit markets offer. Let’s see how broadly prices and other characteristics can vary during different environments and again raise the red flag on yield chasing. Here we go!

Critical credit conclusions

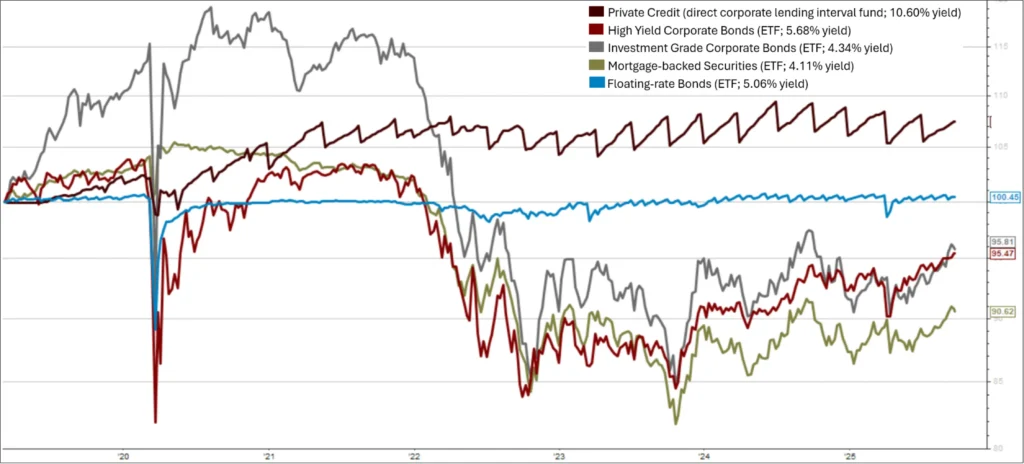

We touched on some yields available in various credit structures as we wrapped up Part 3, resulting in a general sense that yields tend to rise as we move from higher to lower quality and into areas of less liquidity. However, just as the current dividend yield of a stock tells us very little about the company itself, yield is but one of many important attributes for making sense of a credit investment. As an example, let’s look at how prices have trended in recent years in some of the areas we covered last time: higher and lower quality corporate bonds, floating rate bonds, mortgage-backed securities, and private credit.

We’re looking at approximately 6.5 years of history (since March 8, 2019), which is as much data as we have for the private credit fund. However, this timeframe is particularly useful because it encompasses both the onset of COVID and the impact of rapidly increasing interest rates in 2022.

(Source: FactSet, 9/22/25)

Keep in mind that the above chart shows only price – not total return – so it ignores the interest payments. Still, it’s a good thing if an investment maintains its value while also paying the income it’s supposed to. Some takeaways:

- High-quality (investment grade, aka “IG”) Corporates: were really crushing the competition until COVID appeared in early 2020. Then, after a rapid (violent) drawdown and recovery, these bonds already seemed to be losing some steam before rates took off in late 2021. Visually speaking, this IG Corp ETF fell from a peak of about 119 to 85 at the low – a drawdown of over 28% and not what one is typically hoping for from “higher quality” bonds.

- High-yield (junk bonds, aka “HY”) Corporates: didn’t experience as much of a pre-COVID runup as the IG bonds, but then their drawdown was only about 18% from peak to trough (~103 to 84); that aligns with expectations. Although I cannot speak to the historical statistics, recent data indicate that this HY ETF has less than half the effective duration and nearly double the yield of its IG counterpart – both of which help cushion prices during rising rates.

- Mortgage-backed securities (MBS): experienced a relatively smooth ride through COVID but have since endured a nearly 22% drawdown (~105 to 82), trailing the overall price recovery. We can infer that this particular ETF held higher-quality agency (government-backed) MBS because the selloff in non-agency (i.e., non-government-backed) MBS (and especially legacy subprime MBS) during COVID was brutal, with drawdowns of over 50% in the funds I was monitoring at the time. Lo and behold, the recent factsheet shows that this ETF is comprised entirely of agency holdings.

- Floating-rate bonds: reflected only about a 12% drawdown during COVID (from 101 to 89), but maintained very steady pricing throughout the 2022 period of rising rates, which hit the other ETFs in the chart so hard. There is a clear visual distinction between the path of the blue floating-rate line and that of the other ETFs in the chart. The subtle zigzagging you see from mid-2022 onward is due to the expected interest payments (technically, what we’d call the dividend of the ETF) being priced in and then paid out monthly. Rinse and repeat. But it’s also interesting to see that – before mid-2022 – that phenomenon is barely discernible because rates were so low!

- Private Credit: fared best during COVID, with a drawdown of about 4% (from ~103 to 99). Why? Because the pricing mechanism is very different than public markets. Private Credit has the luxury of taking a deep breath and assessing the value of each loan based on fundamentals, such as borrowers being current and expected to continue paying for the life of those loans, as well as anticipated recovery in the event of defaults. Private credit managers/lenders will also actively manage the loans, step in to help underlying businesses, and take action to amend, extend, and potentially even improve overall terms (for the lender) in times of turmoil. The floating-rate nature clearly helped during the rising rates of 2022, as this private credit fund was unscathed. Last, note the pronounced zigzagging due to the relatively high yields we discussed last time.

In public markets (as with the above ETFs), prices are susceptible to being skewed by the most recent trades. And if other bond owners are accepting bad prices for the underlying bonds and ETFs themselves (think forced selling and panic selling in times of distress), then those are the prices the market will reflect.

Don’t chase yield.

I remember speaking with several investors in the COVID moment who had purchased very high-yielding, publicly traded closed-end funds as a source of the portfolio income they needed. Aside from my personal findings that these instruments often eat away at themselves even in normal times (i.e., you get a very high income as promised, BUT the value of your investment slowly deteriorates at the same time such that you are losing money), when the world temporarily shut-down and markets collapsed, those investors learned that the leverage and panic selling can quickly lead to prices declining over 50% with no understanding of if, when, how, or why they should ever recover. Knowing why you own what you own (WYOWYO) goes a long way when the going gets tough.

What about yield-chasing on steroids?

If you thought chasing yield was a bad idea before, 2025 will not cease to amaze you. The Bloomberg headlines that got my attention are “GenZ Chases 90% Yields to Quit Work,” and “The New American Hustle: Dividends Over Day Jobs.” The sad part is that these aren’t hyperbolic. Please don’t quit your day job yet and allow me a moment to be the voice of reason.

We love dividends (and more specifically, Dividend Growth) at TBG, and parts of these articles do reference more standard high-dividend funds. However, they go on to explore new ETFs that yield 90% or more. If you’re wondering how that is sustainable, you’re asking the right questions (hint: it’s not). Both the funds’ creators and investors seem to know that this is a mechanism of returning (hopefully all of) people’s money back while destroying their principal. Umm, what? It makes no sense. But, you know, YOLO.

And, finally, what about “guaranteed” high yields?

The only thing that keeps me from overtly calling the above strategy a Ponzi scheme is the outside chance a given investor is getting their own money back, rather than being given other people’s money (but, if new investors are effectively funding older investors, then let’s call a spade a spade). If you come across someone touting guaranteed high yields, then I’d yet again advocate for caution. That strategy turned out very badly for investors, some of whom sunk their entire savings into what was simply theft and the funding of a lavish lifestyle for the founder. Even if you think an idea is the greatest thing ever, I’ll stand by my long-time position that you want to keep these things to roughly a 5% portfolio position.

PE is Next

There is so much credit we haven’t even touched on, including the massive world of municipal bonds, but hopefully the above covers a broad enough spectrum to convey essential points without being overly complicated: Credit instruments can help serve different purposes, as they vary widely in risk, income, total return, liquidity, and pricing structures. “Credit” naturally involves risk, and embracing diversification while avoiding things that sound too good to be true is prudent.

Stay tuned for yet another edition, when we’ll move into private equity and more good times for all!

Until next time, this is the end of alt.Blend.

Thanks for reading,

Steve