“Half the world does not know how the other half lives.”

— François Rabelais

From time to time, it’s useful to step back from the weeds of portfolios and seek a broader perspective; today’s endeavor may even be more of an exercise in what we take for granted in our typical investment approaches. As an investment community, we spend so much time looking at asset classes, underlying holdings, and – especially these days, given the prolific ETF business – indexes, it’s surprisingly easy to lose sight of how limited our vantage point can become over time. Given we represent specks of dust on a planet that is but a speck of dust in an unfathomably massive universe, we in the US assign an insane amount of importance to whether a stock index (e.g., the S&P 500) is up or down a percent in a given day.

Rabelais was writing about people, not portfolios, but the observation holds. Across the world, investing tends to be done from a relative perspective. Thus, half the world may not know how the other half invests, but my guess is this sentiment holds across much smaller fractions of the global population – with biases at the regional or even country-specific level, and most investors don’t fully appreciate how much of the world’s wealth exists outside the places they typically look.

Today, we’ll attempt to grasp the composition of the financial universe to gain insights into what we may be missing. It may not change anything about the way we invest, but it could help us understand a bit more about why we own what we own (WYOWYO) or open our minds toward other asset classes (ahem, Alts), and that’s always a good thing. Here we go!

First, the ridiculous

This video, which contemplates the value of everything on Earth ($15.8 trillion billion, which is $15.8 with 18 zeroes after that), is pretty interesting, but beyond the scope of today’s discussion, as that accounts for every element on or within our planet. We need to focus on something more pragmatic, like what people actually own.

What the World Owns

We can look at global wealth by breaking it down into a handful of familiar categories:

- Businesses, meaning ownership of productive enterprises

- Real estate, ranging from homes to farmland to office buildings and infrastructure

- Loans and credit, from mortgages to private corporate lending

- Bonds, issued by governments and companies

- Cash and currencies

- Natural resources and real assets

- And a growing collection of legal and financial structures that don’t fit neatly into any single box

None of this is exotic, yet (after a lot of searching), it’s still not a perfectly clear picture. Here are some things that seem like reasonable estimates, via Copilot and several websites, including Ocorian, Savillis, McKinsey, and the IMF (with data from 2023-2025).

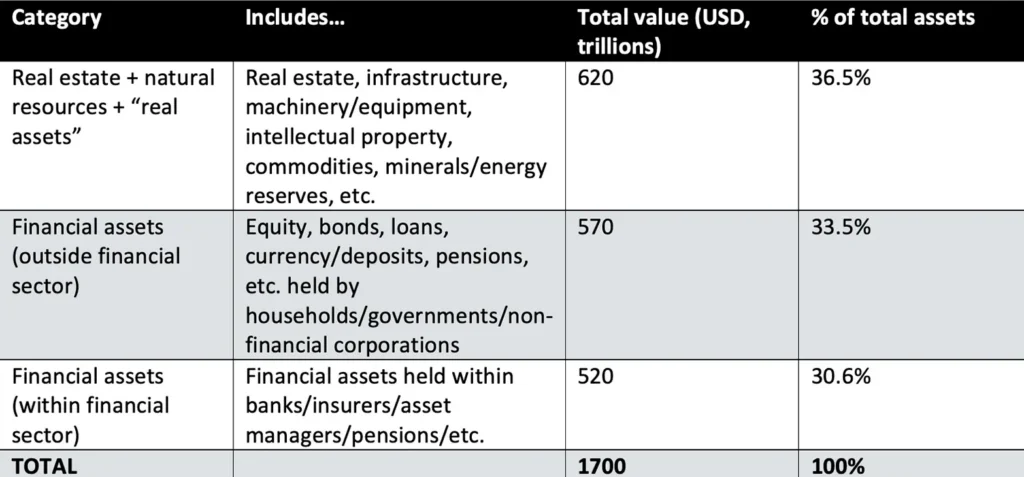

Global balance sheet: $1.7 quadrillion assets (i.e., 17 with 14 zeroes after it). Note there can be overlap and even offsets in these (think debt vs. equity), but here are some highlights to get our bearings:

- Real assets (minerals, energy reserves, commodities, IP, etc): ~$620 T

- Real estate: ~$393 T, including residential ($287 T), commercial ($58.5 T), and agricultural land ($48 T).

- Public businesses (listed equities): $115 T

- Private businesses: we can back into something in the range of $300-$600 T for these, but it’s very difficult considering a lot of the value overlaps (think real estate and real asset holdings in these businesses)

- Global debt: ~$250 T

- Private debt ~$150 T

- Public debt (sovereign & corp/other bond markets) ~$117 T

- Private markets (private equity/debt/infrastructure/real estate funds): ~$14T. Note that ~75% of this is PE and excludes dry powder.

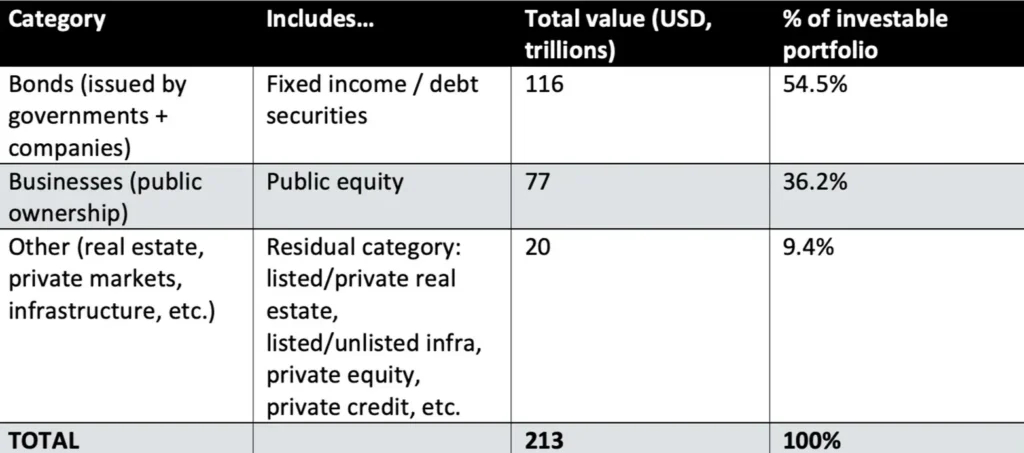

Investable Capital Markets (MSCI, 2023)

*Source: UBS, Allianz, St. Louis Fed, ECB, CEO World, Chart created by author, April 27, 2026

The World Balance Sheet (McKinsey, 2024)

*Source: UBS, Allianz, St. Louis Fed, ECB, CEO World, Chart created by author, April 27, 2026

Synthesizing the above

- Public businesses are relatively small in comparison to global real estate, real assets or the overall global wealth picture.

- Private debt is larger than public debt, though not by an exorbitant amount.

- Private businesses are worth multiple times that of public businesses.

- The “investable” world is roughly a 40/60 (40% equities & Alts / 60% fixed income) vs. the “standard” 60/40 model we often see for investors.

- From multiple perspectives, it seems real estate and real assets represent roughly 1/3 of all wealth on Earth, and the other 2/3 is everything else.

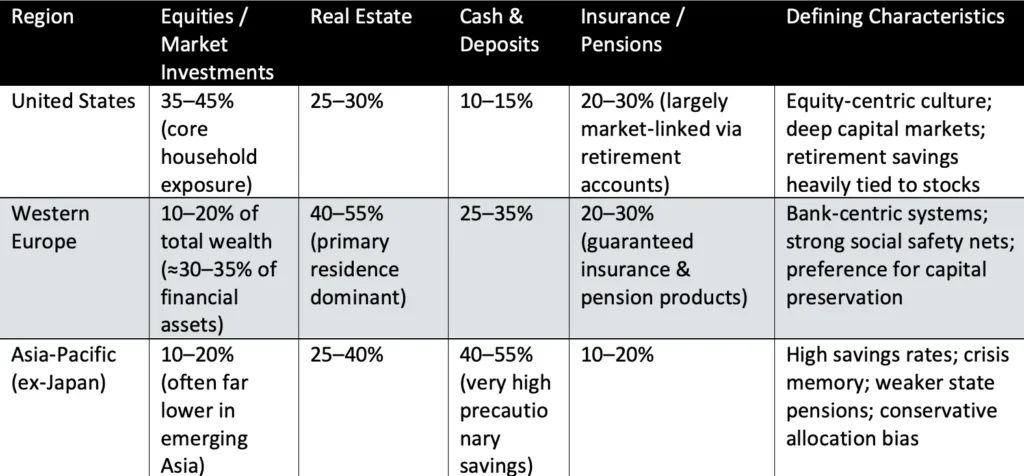

Oh, regional thinking

I thought it would also be interesting to see if we could identify some regional differences in how investors position their assets, and the results are in the table below. Concisely, though, US investors tend to have a higher equity allocation than Western Europe or Asia, with Asia being the most conservative, and real estate looks to be the most consistent allocation globally. That may be somewhat intuitive, as people need to live somewhere (not that they necessarily need to own their home).

*Source: UBS, Allianz, St. Louis Fed, ECB, CEO World, Chart created by author, April 27, 2026

The passive thumb on the scale

Considering the above, aspirations of a true index or “passive” investment posturing would likely be unpalatable to the biggest proponents of passive indexers. And some may find that to be completely ironic (unlike Alanis Morissette’s song of the same name, which we can thank the Reddit community for officially deeming to be only half ironic).

It turns out that my 60% S&P500 / 40% Barclays Bond Aggregate “passive” portfolio is wildly overweight the US, equity, debt, public markets, and significantly underweight private businesses, real estate, and real assets vs. the global balance sheet. And by not altering that exposure over time, one is also actively allowing the best performers to become increasingly dominant pieces of the portfolio. So, call it low cost or call it indexing, but don’t call it passive because there are real allocation choices being made in these portfolios.

Good news

Particularly within our Dividend Growth strategy, we invest in a lot of public equities (actively 😊), and we love the attributes they provide to us. We aren’t seeking to own a global index, but it also shouldn’t be overlooked that many of these are large multinational corporations that provide exposure to real assets, global currencies, resources, debt, and the thoughts, actions, and adaptation of what may be many thousands of humans via a single liquid ticker symbol. It’s an amazing concept.

Thus, I don’t think one needs to own all the pieces of the official “global index” portfolio to have a lot of those exposures. But I also don’t think those who can afford illiquidity and could benefit from the attributes of private-market investments should shy away from a healthy allocation to such investments in their portfolios (obviously implemented appropriately with good managers), as more than half of the global balance sheet is privately held.

Much like Rabelais’ observation, this is simply about building awareness beyond our typical framework.

Until next time, this is the end of alt.Blend.

Thanks for reading,

Steve