Dear Valued Clients and Friends –

It was a heavy and somber weekend in the news cycle, and I address some of that below. As for all of our other topics, today’s Dividend Cafe makes it around the horn.

Dividend Cafe on Friday looked at the impact my late father, not a finance guy but actually a philosopher and theologian, had on my own investment philosophy. The written version is here (my favorite), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

- The market opened up +100 points today, but almost immediately gave that back and stayed between the flat level and down a bit throughout trading hours.

- The Dow closed down -41 points (-0.09%) with the S&P 500 down -0.16% and the Nasdaq down -0.59%.

*CNBC, DJIA, December 15, 2025

- I believe the story of the quarter is that all four of the big four in AI-infrastructure or hype – Nvidia, Oracle, Palantir, and Broadcom, reported numbers much better than expected (and those expectations were sky-high), and all three saw their stocks drop quite a bit.

- Almost everything in the market right now indicates rotation, not correction. Breadth has substantially improved, advance/decline ratios are quite good, and even-weight vs. cap-weight has improved dramatically, and small-cap has picked up vs. large-cap.

- The ten-year bond yield closed today at 4.18%, down 1.6 basis points on the day.

- As the short end of the curve has dropped (Fed) and the long end picked up a bit (improving nominal GDP expectations), that steeper yield curve has accrued to the benefits of the bank stocks (unsurprisingly). One high-profile bank stock (Bank of America) just got back to its 2006 high!

- Top-performing sector for the day: Health Care (+1.27%)

- Bottom-performing sector for the day: Technology (-1.04%)

- The market has never been down a year later when the S&P 500 was at or near an all-time high, and the Fed was cutting rates. The 2024 rate cuts into the 2025 market action have shown not to be an exception to this.

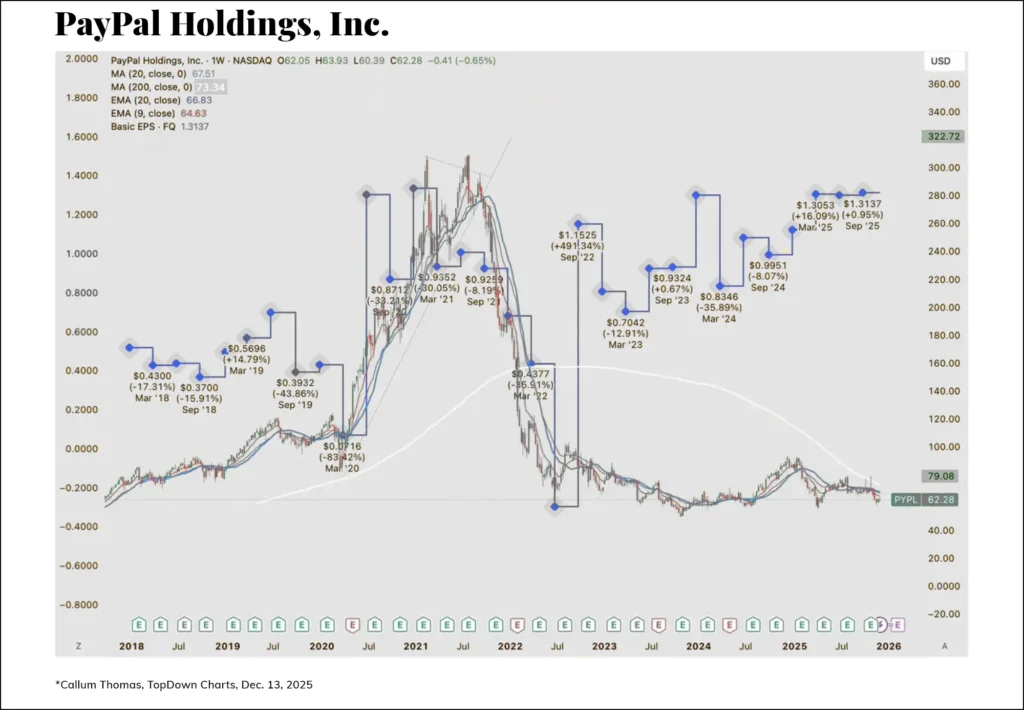

- I thought this chart from Callum Thomas had to be shared. Here you see the stock of a well-known company, PayPal, which saw earnings and the stock price clobbered in 2022. The earnings have since recovered, but the stock price has not. Why? Valuations matter.

Top News Stories

- There were so many tragic stories over the weekend that I hesitate to go into them at all, just to avoid depressing readers (or myself) in what is supposed to be a financial bulletin. But from the Brown University shooting to the ISIS attack on Americans in Syria to the Bondi Beach atrocity in Australia to the patricide/matricide of Rob and Michele Reiner to the outrageous conviction of Jimmy Lai, it was just a really tragic weekend.

- Outside of the weekend tragedies, the ongoing discussions in Europe about a potential Ukraine/Russia deal remain a major news story, with no real clarity on how it will end.

Public Policy

- As we get closer to the date that I think (hope?) the Supreme Court will rule the IEEPA rationale legally out of bounds for tariffs, it is worth reminding readers that Section 232 (“national security”) and Section 301 (retaliating against “unfair” trade practices) rationales will be used in replacement for the bulk of the tariffs currently under IEEPA. Now, some will not – it would defy logic and law to a point of such absurdity that even this moment wouldn’t allow for it. And even while the search for replacement pretext takes place (and implementation thereof), there would be some tariff relief to some companies in that period. But the administration has signaled that, regardless of what temporary reprieve comes from a Supreme Court ruling that goes against the administration, they intend to switch things around as quickly as possible to revert to a status quo on tariffs. For what it is worth, prediction markets are currently 74% that the Supreme Court will rule against the IEEPA tariff rationale.

- Where things are going regarding the Affordable Care Act subsidies remains a bit of a mystery. House Republicans are about to present their plan. There appears (to me) very low odds of Republicans agreeing on a path forward (some are willing to extend subsidies, some are not, and some want some modified version of subsidy enhancement).

Economic Front

- The trade deficit came in at $52.8 billion for September as government data continues to play catch-up from the shutdown of a month or so ago. Total trade is only up 0.4% on the year (not good), and down -10.3% from the March 2025 high (which you may notice, just so happens to be right before the Liberation Day saga began)

- China’s economic metrics for November showed a meaningful decline in consumer spending, and especially showed ongoing drag from its overextended property sector.

Housing & Mortgage

- 75 of the top 150 metro areas in the United States this year had declining apartment rents year-over-year. The metric used to measure rents in the CPI calculation is still claiming well over 4% increases in this metric. Some of these markets are seeing price relief/decline because they are legitimately over-supplied (Denver, Austin, Phoenix), and some are just lower-demand or were plain over-priced (Washington DC, Los Angeles, Sacramento). Either way, declining rents are what happen when rents get too high, because the solution to high prices is … high prices.

- The NAHB Homebuilder Sentiment Index was 39 in December, well below the “neutral” level of 50, and right around the same level as last month (38). The Present Situation is a big drag, while Expectations are much better. Rising construction costs from tariffs continue to be cited as a big drag, and of course, sidelined buyers due to affordability issues are a pressing concern.

- To that last point, 40% of builders said they cut prices last month, and the use of incentives to get a deal done rose to 67%, the highest since COVID.

Federal Reserve

- I have to say, while the Fed cut last week was well-known to be coming, Chairman Powell surprised markets with his more dovish tone and direction, just as at the last meeting he surprised markets with his more hawkish tone and direction.

- The Fed’s $40 billion/month of T-bill buying is not QE in the sense that it will not be growing the Fed’s balance sheet; rather, it is a liquidity management tool addressing reserve funding. It seems to me that there is a latent admission that something is not functioning properly with the repo facility.

- As mentioned last week, the Bank of Japan is set to increase interest rates this week, even as the rest of the world is cutting rates, though they remain in a negative real yield.

- President Trump is either pump-faking markets or has already changed his mind on Kevin Hassett as the next Fed chair. He went to great lengths Friday to trial balloon Kevin Warsh as his new frontrunner, despite previous heavy winking and nodding that Hassett was getting the gig. I think it could be either: that Warsh is back in the mix, maybe even the front-runner, or that he is faking it and Hassett is the fait accompli.

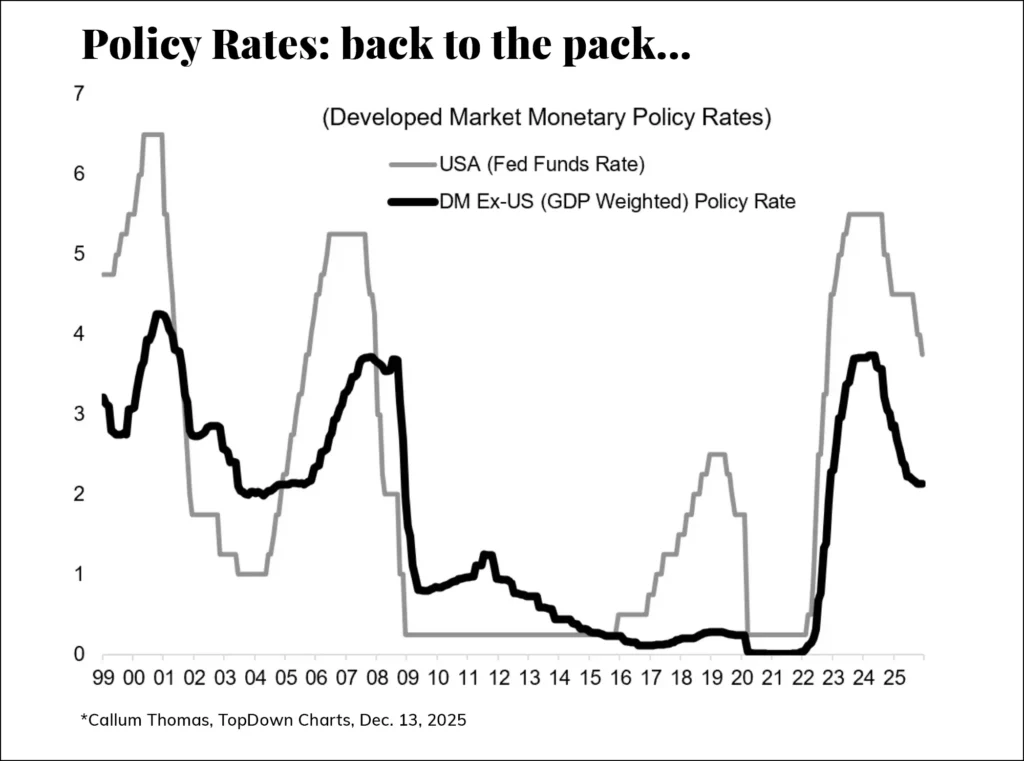

- As much as the Fed has cut over the last fifteen months, it remains higher than the rest of the developed world, having been so much tighter than the rest of the developed world before …

Oil and Energy

- WTI Crude closed at $56.61, down -1.44% on the day.

- Oil dropped over -4% last week and natural gas dropped -20%, but energy stocks were not down that much (midstream dropped -2% but some big integrated names like Exxon were actually up +2% on the week).

- Midstream names with high takeaway business in the Permian did well as Exxon announced plans to increase production in the Permian over the next five years.

- We are currently producing an all-time high of 13.6 million barrels of oil per day in the United States.

Ask TBG

| “Aren’t long-term interest rates the main driver of the dollar (higher rates, stronger dollar – and lower rates, weaker dollar)? Is that now changing? How should we think about the dollar relative to other currencies and the correlation with interest rates?” ~ Edward L. |

| Interest rates are a major driver of what the dollar may do, but they are not the only one. Trade balances, geopolitics, economic growth, inflation expectations, and a host of other economic criteria fit in as well. And of course, our own absolute direction of interest rates impacts the dollar in that context, relative to other currencies and their own interest rate direction. So I think the best way to answer this is to say, yes, interest rates matter a lot for the dollar, but no, they are not all that matter. |

On Deck

- The Dividend Cafe this week will look at the last 25 years of investing now that the new millennium turns 25 years old, and extract the biggest investment lesson from this period one could imagine.

- The last Weekly Portfolio Holdings Report of 2025 will hit client inboxes this Wednesday AM.

I mentioned the murder of Rob Reiner above. He had no shortage of amazing films that he made, so when I highlight A Few Good Men, I do not do so as a slight to any of the others. But I can sit and quote the entire movie, start to finish, and as several friends and family members would attest, I have done so (to their chagrin) while watching it with them. It was a masterpiece, and a defining film of the early 1990s and then the whole decade (may have been my first DVD movie purchase). A tragic ending to a simply incomparable directorial life. RIP.

I will be in New York City all week. There will be one final 2025 Monday Dividend Cafe next week, the 22nd. In the meantime, we will see you in the Daily Recap each day this week. Reach out with questions any time.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.