Dear Valued Clients and Friends –

A very traditional Monday Dividend Cafe today with a very standard trip around the horn!

Dividend Cafe on Friday looked at the notion of an “independent Fed,” why it can’t exist, why it hasn’t ever existed, and what needs to be done to right-size the Fed in the new chairman’s regime. The written version is here, the video is here, and the podcast is here.

I was on Maria’s Wall Street show on Friday from the Reagan Library talking markets. The link is here. I was on Varney/Fox Business this morning talking markets, June calendar action, and dividend growth vs. high dividends. That link is here.

Off we go …

|

Subscribe on |

Market Action

- Markets opened down -150 points this morning and recovered a bit throughout the second half of the day after hemming and hawing in the first half.

- The Dow closed up +46 points (+0.09%) with the S&P 500 up +0.26% and the Nasdaq up +0.42%

*CNBC, DJIA, June 1, 2026

- The S&P 500 continued its torrid pace from April, jumping +5.15% in May, and is now up +10.7% on the year and over +20% from its low point of the year.

- We currently have the highest household allocation to stocks we have ever had, and valuations are essentially near all-time highs (by some metrics, we are not as high as pre-March 2000 valuations, and in others, we are there or higher).

- If you hear that “small cap has not kept up with its mega cap counterparts,” just know that the Russell 2000 is now up +70% since its 2025 low. For those who have forgotten, 2025 was, ummmm, last year.

- The ten-year bond yield closed flat today at 4.46%. The yield had spiked by 5 basis points intra-day but gave it all back by the close.

- Top-performing sector for the day: Technology (+2.48%)

- Bottom-performing sector for the day: Utilities (-3.05%)

- The combination of concentration, valuation, and magnitude of rally shows some numerical comparisons (h/t Cullen Thomas):

![]()

- I saw a report over the weekend from someone whose social and cultural commentary I often like a lot, and whose technology world expertise is often quite stellar, but whose general macro market takes have been among the most reliably bad I have ever seen (name withheld to keep with a rule my dad taught me). His latest take is that emerging markets could face a dollar-debt squeeze from oil prices that brings European banks down and creates a 20-40% drop in the S&P 500. Emerging markets, by the way: Up +25% YTD.

- With a h/t to Michael Burry and Peter Boockvar, the SpaceX, OpenAI, and Anthropic IPO’s are looking to raise more than 300 internet IPO’s from 1999/2000, after adjusting for inflation. This is not a reference to the proposed value of these three companies – just the amount they are looking to raise in the IPO’s, which are somewhere around just 5% of total market cap being floated to the public.

Top News Stories

- Iran has threatened to “completely block the Strait of Hormuz” and said the peace talks are over. President Trump has said negotiations continue, but he is ready to move forward with a new step since Iran has taken so long, and has said he will keep the blockade.

Public Policy

- The Florida Attorney General has filed a lawsuit against OpenAI over various AI risks and harms.

- There are conflicting news stories on this, but my sources tell me the White House will walk away from the $1.8 billion “anti-weaponization” fund that has created so much pushback, and that a federal judge has imposed a temporary pause pending a hearing.

Economic Front

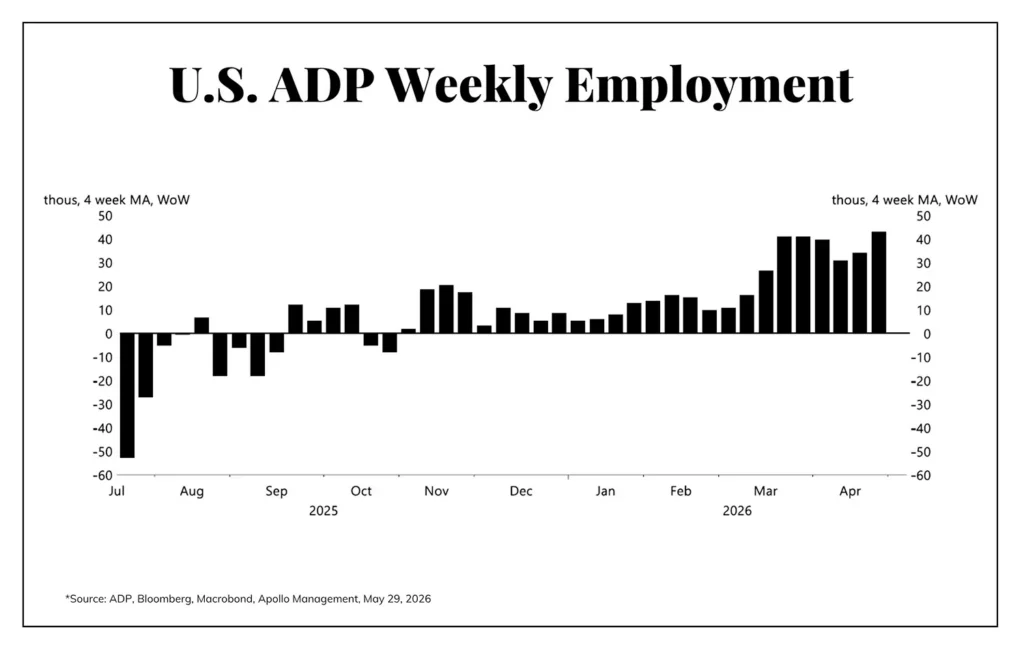

- This chart from Torsten Slok of Apollo is a great example of why I have turned more optimistic on the state of labor markets. We are not seeing the hiring I want to see with small business, but hiring has picked up, and as has been the case throughout history, it is largely a situation of disruption creating new opportunity.

- The May ISM Manufacturing Index was above estimates at 54, with New Orders up almost three points on the month. Stockpiling in preparation for Middle East concerns and supply chain disruptions appears to be behind the recent data, but I do think several months in a row of modest improvement in manufacturing data point to some marginal benefits from the bonus depreciation of OBBBA and, of course, AI capex. 16 of 18 sectors showed expansion.

- Now, to those saying, “yay, this means we are seeing a resurgence in manufacturing hiring finally!” – not so fast. The employment index for manufacturing was negative for the 32nd month in a row. Those numbers have worsened, not improved, since protective tariffs were implemented.

Housing & Mortgage

- It is very rare for national home prices to decline. It simply does not happen on a national level very often. Nevertheless, the Case-Shiller Index was down -0.2% last month. In the FHFA index, things were just barely into positive territory.

- Rent growth is only up +1.9% from a year ago (Zillow), which will help to bring the overall inflation rate down from what it would otherwise be, since Shelter has such a high weighting in the data.

Federal Reserve

- My whole Dividend Cafe on Friday was Fed-related, so I’ll leave this one alone today, except to say we are up to a 50% chance of some rate hike between now and the end of the year.

Oil and Energy

- WTI Crude closed at $92.42, up almost +6% on the day

- Midstream was hammered last week (down -7%). On the month, though, oil was down -17% on the month, yet midstream was only down -2.9% and remains up over +20% YTD.

- Crude oil inventories continue to dwindle, and record low levels of inventory are upon us. The good news is that the price impact from the Strait’s closing has been mitigated by large and continued drawdowns of pre-existing inventory. The bad news is that this appears to be nearly at the end of the road.

Ask TBG

| “What do you think about Warsh considering trimmed inflation?” ~ J.B.M. |

| “Trimmed inflation” is a way of measuring inflation that removes extreme price changes – “outliers” that disproportionately impact the aggregate number either on the high side or low side. I believe this is a very good idea, and while not a total replacement of the aggregate inflation data, it provides an additional data point that should help inform a Fed narrative more holistically. This reduces data volatility, gives a more accurate sense of monetary inflation (which is what the Fed is supposed to be concerned with), and ultimately provides more useful data in their process. I would not favor living exclusively off of this data, but I do not favor excluding it either. |

On Deck

- The May jobs report from the BLS will come this Friday

- Clients will receive their Weekly Portfolio Holdings Report on Wednesday, per usual.

- Dividend Cafe this Friday will feature the commencement speech I am giving at Pacifica Christian High School’s graduation tomorrow night.

Reach out with any questions, and to all graduating this week, I say, congratulations!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.