Dear Valued Clients and Friends –

Lots of Public Policy today and a typically fun Monday trip around the horn!

Dividend Cafe on Friday did a deep dive into the state of the Fed, the drama playing out there, and the implications (or lack thereof) for investors. The written version is here (my favorite, especially this week), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

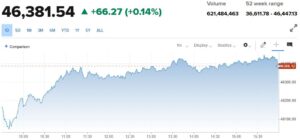

- The market opened down -300 points today and rebounded off of that throughout the day.

- The Dow closed up +66 points (+0.14%) with the S&P 500 up 0.44% and the Nasdaq up +0.70%

*CNBC, DJIA, Sept. 22, 2025

- Peter Boockvar pointed out that the S&P 500’s bottom in March 2009 was at 666 (something I have always known), and that on Friday the S&P 500 price level hit 6,666 … So do with that what you wish.

- Don’t look now, but earnings growth looks significantly better for small-cap companies in 2026 than it has for quite some time. And though much of it is the base effect (i.e., the low level of earnings from which small-cap companies are growing), the relative growth in 2026 compared to large-cap companies is expected to be much, much stronger.

- The ten-year bond yield closed today at 4.15%, up one basis point on the day.

- Top-performing sector for the day: Technology (+1.74%)

- Bottom-performing sector for the day: Communication Services (-0.92%)

- The Consumer Staples sector ratio to the S&P 500 is the lowest it has been since March 2000.

- That the Mag7 is making new highs at the same time the Russell 2000 (small cap) is making new highs is perhaps the most unique thing playing out in risk assets right now (whereas that mega cap standout performance has been at odds with small cap performance for several years)

- Momentum and Beta are the strongest factors as of late. And that will last until it doesn’t.

Top News Stories

- The memorial service for Charlie Kirk became the major news event on Sunday, and President Trump will be addressing the United Nations in NYC tomorrow.

Public Policy

- The announcement of a new $100,000 fee for H1-B visas was the most significant policy announcement of the last week (don’t worry – the TikTok news is coming next). The program used to recruit top talent from overseas will see this cost implemented for new hires, not current members of the program or renewals, according to a White House clarification given this weekend. It will also be a one-time cost, not an annual cost. It was also understood (but not confirmed) that doctors will be exempt from the requirement.

- Though everyone has been careful to point out that no deal is yet signed, President Trump insists that President Xi of China is on board with the TikTok deal framework that will allow the Chinese-owned app to stay in American device app stores and on American devices, with a new ownership structure that will include several U.S. companies (Oracle, Andreesen-Horowitz, and Silver Lake). Oracle will become the “security provider” and will “independently monitor the source code of the app.” They will further “retrain” the algorithm and store the user data on a cloud controlled by them. ByteDance (the Chinese company) will maintain a 20% interest in the equity of the U.S. operation. The full list of new investors is not yet set.

- Whether or not the government will shut down in a little over a week is not a story I will spend a lot of time focused on because I have done this way, way, way too many times. The only thing unique this time is that it is Republicans seeking a clean funding bill and Democrats seeking various concessions to agree to fund it. There are obvious political reasons for why each party will go about the way they will, but to me, there is just almost no doubt how it will all end (government will get funded), and the only question is what kind of grandstanding and early campaigning we will be forced to endure from rank performance artists along the way.

- The annualized amount of tariff revenue now being collected is over $350 billion and should settle between $350 and $400 billion at current levels. Some have taken to referring to this as revenue to the United States Treasury, which is true in the same sense that the income taxes we pay are revenue to the Treasury. However, as is always the case in double-entry accounting, the credit to the Treasury is a debit to American businesses, and the impact of this $350-400 billion cost to American businesses is the question that needs to be addressed.

Economic Front

- The BLS announced that they were delaying this week’s release of inflation data. Candidly, that has happened before (including one time last year), but when it has happened before, it was accompanied by a specific release date indicating when the delayed data would be forthcoming. That did not happen this time, which is, well, odd.

Housing & Mortgage

- On one hand, First Trust reported today that new rents declined -8.4% in Q2, which they accurately say would be the steepest quarterly decline on record. But on the other hand, I couldn’t find any source, verification, or data to support that. What they appear to be referencing is a 2.1% quarter-over-quarter drop in the BLS’s New Tenant Rent Index series (I assume they are taking the quarterly number and annualizing it). I do believe (see the notes on Miran’s address to ECNY today under Fed, below) that the shelter input to inflation is coming way down, but I don’t believe anyone actually believes they are dropping (or have already dropped) 8% …

Federal Reserve

- I listened live to new Fed Governor, Stephen Miran, give his address to the Economic Club of New York, today. He made his case for why a Taylor Rule methodology, with revised inputs to his read of where certain economic data points are going (with a focus on actual residential rents, and the impact of immigration/border changes), ought to call for a 2.5% Fed funds rate (or so). That he sees the inflation reading coming down to 1%, taking 0.33% out of the total inflation level, is something I agree with entirely (we just had the biggest negative print to rents we have seen).

- I laughed on Friday when I saw the headline (“Japanese bond yields hit their highest level since 2008”) and then saw the yield – the 10-year is at 1.64%.

Oil and Energy

- WTI Crude closed at $62.38, pretty flat on the day

- Midstream last week was a mixed bag, with Canadians doing very well and U.S. MLPs mostly down.

Ask TBG

| “Thank you for your usual good work making complex issues at least a bit easier to understand. I was surprised you didn’t mention the impact on monetary policy of continuing $2 trillion+ deficits. That continuing deficit spending makes me wonder if we need rate cuts or not and what impact they will have.” ~ Jeff H. |

| I do believe I erred in not discussing this in Friday’s Dividend Cafe, because I think there is simply no doubt that one of the more structural challenges the Fed faces is aligning monetary policy with the structural fiscal reality they are forced to deal with. While it is not unique to this quarter or this meeting or this rate cut, the embedded reality is that, as much as massive resets of commercial real estate or levered loans matter, there is no question that the term structure and cost of borrowing of the $30 trillion of U.S. public debt matter too. And I do believe a structural accord between monetary and fiscal policy exists. And I believe this accord contributes to Japanification, even when the accord is softer than the one in Japan. |

On Deck

- The August PCE data will come this Friday (the Fed’s preferred inflation measurement)

I was on Varney this morning discussing valuations and appeared on CNBC this afternoon, where I was again asked about valuations and buyable areas of the market.

Reach out with any questions, any time.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.