Dear Valued Clients and Friends –

Because of the MLK Day federal holiday yesterday, this week’s “Monday” Dividend Cafe is coming to you on Tuesday. We go around the horn today, but, understandably, a lot of attention is being given to the big market sell-off in the aftermath of President Trump’s tariff threats against European countries.

Dividend Cafe on Friday was one of my favorites to write in a long time, as I looked at the history of media company mergers and suggested that sometimes, perhaps what is in shareholders’ best interests is not driving the decision-makers, and that dividends and growth of dividends have been, well, the media place to be. The written version is here (my favorite), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

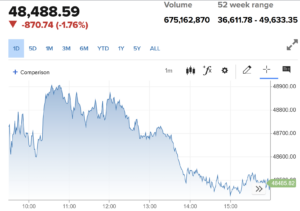

- Markets opened down -700 points this morning, made an early attempt to rally off of that, and then dropped throughout the day.

- The Dow closed down -871 points (-1.76%) with the S&P 500 down -2.06% and the Nasdaq down -2.39%

*CNBC, DJIA, January 20, 2026

- The challenges with Mag 7 names are not really predictive at this point and are rather descriptive. The Wall Street Journal actually covered this yesterday (I offered a little perspective in the article). On one hand, Google is up +67% over the last 12 months, and even though Nvidia is down -16% since October 29, it is up +30% over the last year. But look at the returns for the other five constituents of Mag 7 over the last 12 months compared to the overall market:

- Amazon: +3.4%

- Apple: +9.5%

- Meta: -0.31%

- Microsoft: +6.9%

- Tesla: -0.45%

The first two weeks of the new year hardly matter, but it is worth noting that the Mag 7 is down -4% as a group YTD (with only Google and Amazon up at all). I bring this up merely to comment on the rotation at play: the mathematics of the index shows that the largest-cap companies are not leading, and the healthy broadening in the market this has (so far) demonstrated.

- The top companies in the S&P 500 make up 26% of the earnings of the S&P 500. That is pretty good, right? Why do I fret so much about their concentration? They make up 40% of the S&P 500. That kind of disconnect (or anything close to it) has never been seen in history.

- The ten-year bond yield closed today at 4.29%, up six basis points on the day.

- Top-performing sector for the day: Consumer Staples (+0.12%) – only positive sector

- Bottom-performing sector for the day: Technology (-2.94%)

- I’m supposed to inform you that the Dow Jones Transport Average had hit an all-time high before coming into today. This, combined with price action in emerging markets, industrial metals, and even global shipping stocks, all point to some reinforcement of the global cyclicals story. What is missing to affirm this story? Higher bond yields. What do higher bond yields do to growth stocks? Pummel excess valuations.

- Today’s market action was really about the uncertainty around the latest Trump tariff threats and some degree of pricing the risk around Europe’s retaliation. Higher-valuation stocks got hit worse, as one would expect in such a sell-off. The President’s speech at Davos tomorrow will presumably tell markets if he is looking to rhetorically escalate or de-escalate from here. My expectations for this rather embarrassing saga going forward are one of these three things, though technically in a certain sequence it could prove to be more than one:

- More escalation as both sides dig in their heels around the threats and counter-threats, leading to more short-term market volatility and uncertainty

- A quick de-escalation as markets price the idea of a President who backs down on his latest threats in the face of tough market and economic reaction

- The first one, then the second one, with the time in between uncertain

Public Policy

- I will say, I think an underrated explanation for today’s accelerated market sell-off was the Supreme Court’s ridiculous announcement that they won’t have a ruling on the IEEPA rationale for tariffs until late February (exacerbating market uncertainty for no reason).

- President Trump announced over the weekend that he would implement 25% extra tariffs on any European country that doesn’t support the U.S. taking over Greenland. European nations replied that if that happened, “prior deals were off.” Yeah. The European Union met in Brussels on Sunday and appeared ready to fight back this time. Treasury Secretary Bessent urged our European trading partners to “take a deep breath” and to “let it all play out,” which I assume means, “come on, you guys, you know he is just saying things.”

- The U.S. is going to host a meeting on Feb. 4 led by Secretary Rubio with dozens of foreign leaders to discuss ways they can all reduce dependency on Chinese critical minerals.

- Bloomberg reported Friday night that the White House is planning on trying to cap credit card interest “via executive action.” It is not clear to me how this could be legal. It is certainly clear to me that it is a terrible idea.

- It is not clear whether HHS or the White House will issue any retractions, but a comprehensive review and analysis of prior assertions about Tylenol and autism was released Friday. A brilliant read for those interested.

Economic Front

- Industrial Production increased +0.4% in December (actually +0.5% but there was a -0.1% revision to November). Utilities Output rose dramatically, even as Mining Output was down a bit. Auto production declined -1.1%, and Manufacturing (ex-mining/utilities) was up a small bit. High-tech equipment production was the largest contributor to Industrial growth in 2025.

- Much thanks to Peter Boockvar for turning me on to this fantastic analysis of who is actually paying for the tariffs

Housing & Mortgage

- The expectation is that President Trump will use his speech at Davos to unveil plans for Housing Affordability. Some of the components I expect and/or sources of mine expect include:

- Relaxing capital requirements at banks, allowing them to buy more Treasuries and Mortgage-Backed Securities, which puts downward pressure on yields organically

- The aforementioned plan to make Fannie and Freddie buy $200 billion of MBS (this is, ummm, not organic)

- Changing capital gain tax rules on residence (indexing to inflation or exempting first-time buyers or both) – the inflation index idea is brilliant!

- Allowing people to use 401ks for down payments (not to borrow but to buy)

- Lowering tariffs on building products and construction input costs (okay, I just put this one in myself)

- We heard President Trump a couple of weeks back indicate his intention to block defense and aerospace companies from returning capital to shareholders. Now, apparently, Federal Housing and Finance Agency chair, Bill Pulte (who oversees Fannie and Freddie), is making the same threat against … the homebuilders. Yes, apparently, the homebuilders are going to be looked at for buying back stock when Pulte feels that it may be getting in the way of building new homes affordably. If you could see the look on my face when I read his proclamation.

- 71.1% of licensed real estate agents did not sell a single home in 2025, according to NAR. There are a lot of licensed agents who could call their work in this regard a “hobby,” but this statistic is pretty overwhelming and speaks to the substantial decline in housing activity.

Federal Reserve

- The prediction market odds for Kevin Warsh to be the next Fed chair shot through the roof Friday, and the odds for Kevin Hassett sank to 16% as President Trump shocked the media (and apparently the prediction markets) by saying, “I think Kevin Hassett is too important to me in his current job [at NEC].” The saga continues.

- There are some things here I can not share in terms of sources and deeper meaning, but I believe that Kevin Warsh becoming the Fed chair means more than just a market-credible chairman being selected … I believe it means some meaningful reforms across the Fed, substantial changes at the staff level, and a renewed emphasis on internal violations (ethics, security, etc.) that have become problematic. Am I optimistic he can “reduce the central bank’s footprint in the markets”? Not yet, but some people I know and trust very much are.

- The Bank of Japan owns $500 billion in ETFs (stock market holdings – which is 83 trillion Yen) on its balance sheet. They are about to begin selling these off as a reversal of the super-charged quantitative easing process. My friend, Peter Boockvar, estimates that at the current pace, they will have that done in 251 years. One thing he did notice, though – they more than doubled their money in this escapade.

Oil and Energy

- WTI Crude closed at $59.42, up a tad on the day

- Midstream was up a massive +3.5% last week, even as the S&P 500 was down -0.4% and natural gas prices were down -2%. Earnings season for the sector kicks off this week with the C-Corp behemoth, Kinder Morgan. Canadian midstream names enjoyed a big recovery last week after the Venezuela sell-off of the week before.

- No thanks to many people who have opposed this at every step, U.S. oil production is now 20% of global oil production. It was 8% in 2009. Nearly all of our increase has been used for EXPORTS. The decline in market share for gangster autocrat states and the increase in market share for the United States (leading to a legitimate, job-creating, wealth-producing sector of the American economy) is one of the great miracles of my lifetime, and yours.

On Deck

- TBG client portfolio rebalancing is taking place all week.

- TBG clients will receive their Weekly Portfolio Holdings Report tomorrow morning.

- Dividend Cafe this Friday is on “the gamification” of markets (unless Greenland/Europe/Davos/trade war/tariff stuff gets severe enough to necessitate an audible).

To Buffalo Bills fans: You were robbed

To Indiana Hoosiers fans: Wow. Just wow. One of the greatest sports stories, ever.

To all of you: Enjoy your Tuesday night, and reach out with any questions anytime.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.