Dear Valued Clients and Friends –

As I am preparing to hit send on Friday, the market is following a big tech-led sell-off from Thursday with another tech-led sell-off on Friday. By the time you are reading this the numbers could have reversed, they could accelerate worse, or they could just be sitting still. But no matter where this goes today, or in the days/weeks ahead (obviously there is no surprise in the notion that technology valuations are having air let out of them), it is not the biggest story in capital markets right now.

The current action matters to this week and maybe even next quarter, but it is the state of 0% interest rates that impacts capital market assumptions for quarters and years to come, and I am quite confident, the entire next decade (or longer). And this is not a wonky, quantitative, math-nerd thing (“capital market assumptions”). It is at the core of risk expectations, of return expectations, of portfolio construction, and of the entire approach investors will take to achieve their goals for years!

I am anti-drama. Anyone who knows me knows I find melodrama off-putting. I am not predicting the end of the world and I am not calling for a new, easy way to get rich. I am stating something that I find incontestable – a secular 0% bond yield changes the rules of the game in a lot of ways, and fiduciary advisors will have to make adjustments. That is what this Dividend Cafe is really about – the adjustments coming, and why.

In this week’s Dividend Cafe we will address all of this and more:

- Market week in review – is this the tech correction we have been anticipating???

- A vast and thrilling ride through the world of zero% interest rates, and what this new monetary regime means for the economy, the future, and oh yeah, all investors!

- A tale of two economies

- Something to really worry about

- The danger of stock splits

- The Pro and Con case for the bank sector

- Economic Report Card for the Week (special attention to today’s jobs report)

- Politics & Money – update on the election betting odds, scenarios for election night, and general volatility expectations

- Chart of the Week – a little history of Nasdaq corrections …

A perfect way to launch your Labor Day weekend … Let’s jump in, to the Dividend Cafe!

Market Redux

The market closed last week at 28,650. On Thursday it has reached 29,200 before declining 800 points on the day. As of press time Friday, the market is down another 500+ points, so down ~900 on the week. But the Nasdaq is the bigger story in that it reached an all-time high of 12,074 on Wednesday, and as of press time is sitting at 10,900 (down ~10% in just over one day).

I am agnostic as to whether or not this is the Nasdaq/big tech correction I have been anticipating. I am not agnostic as to whether or not one is coming. Valuations are mean-reverting things, and excessive valuations are really mean-reverting. The other question is whether or not a tech sell-off will bleed into other parts of the market, or signify a long-anticipated (by some) change in market leadership. I suspect it would be a little bit of the former at first, followed by a whole lot of the latter.

But as far as the health of the overall market, day by day volatility in over-valued tech stocks is not going to be the bellwether, and really short term gyrations in broader stock indices won’t be either. If we see meaningful tightening in credit spreads, that is a validating indicator of risk-off, and that is what I am watching.

*Strategas Research, Daily Macro Brief, Sept. 4, 2020

So you’re excited for low rates, right?

I don’t know that one could have a more dovish outlook on what the Fed is going to do in the years ahead than I have. I not only believe the Fed’s zero percent posture is having a huge impact in equity markets right now, but I believe they are going to maintain a zero percent level for as long as the eyes can see. And for borrowers of money, this certainly seems like a really good and exciting thing – I get it.

What I feel morally and professionally compelled to do is explain what some of the costs to this extremely accommodating stance by the Fed may be. I am not critical of what they did with rates in March and I am not ignorant as to where we are as a society and an economy that has created the situation we have. And while I do believe we face significant implications by becoming so extremely Fed-dependent over the last 20+ years, I believe the Fed was responding to circumstances to end up in this role far more than they were creating circumstances (email me/DM me if you want any elaboration on that, any time).

But here is the thing – if you believe in Milton Friedman 101 that there is no free lunch, we simply cannot have all the benefits of a 0% short term interest rate without some cost or payoff from it. And many people have focused (correctly) on the fact that a 0% short term interest rate punishes savers. Low-risk, conservative investors bear the brunt of this policy measure by losing income on CD’s, money market funds, bank deposits, and Treasury bonds. All true. All necessary to point out.

But that is honestly a very small part of what is going on. The 0% interest rate also:

(1) Removes the buffer of protection that central banks, the equity market, and the economy at large have long enjoyed … Having a policy tool in your toolbox to counter-act inevitable economic distresses has been a hallmark of monetary policy for decades; that tool is no longer available. Think of it like having a fire extinguisher in your house, and you use it for a fire that comes; but now you live in the house again, you know a fire comes every 4-5 years (bear with me in the analogy), but you no longer have the extinguisher – you can’t replace it.

Generally lowering rates in times of deteriorating conditions has been a buffer for equity prices, always helping to form a bottom, and generally facilitating an equity reversal. In the ten times equities have dropped significantly the last century, the average move down in short term rates was 2.9% … We obviously can’t move 2.9% lower when the rate is already at zero.

What policy tool is available if rates can’t go lower? The purpose of the question is not to suggest there isn’t one; it’s merely to point out the mathematical fact that pushing up the present value of future equity warnings with a declining discount rate is not an option if the discount rate cannot decline further.

(2) Inflation and real rates rise and fall together in normal times, but once the short term rate hits zero, the relationship falls apart and basically inverts. Deflation, when rates are at zero, forces real rates higher, even as conditions are deteriorating. This has been the deflationary spiral of Japan for roughly 30 years.

The Generational Bond Challenge

U.S. “bonds that act like bonds” provided an incredible diversifier effect in the United States when the [blank] hit the fan earlier this year. Our bond yields entering the COVID crisis were low, but they were well above zero, and as those yields came down the positive price impact to bonds was substantial. But, look at Japan, which entered the COVID moment already at the zero bound. There was no such benefit from holdings bonds in a diversified portfolio. Europe, less so (they were between the U.S. and Japan in yield levels entering the storm and therefore saw an impact that was in the middle as well). Simply put, bonds can not go up when rates are already at the zero bound.

*Bridgewater Associates, Grappling with New Reality of Zero Bond Yields, July 2020, p. 6

Many astute bond investors over the years have used the disparity of monetary and fiscal policies around the globe to solve for certain country deficiencies in bond yields by investing in the sovereign debt of other countries. That option is more or less negated now by the global universality of zero percent interest rates. In fact, over 80% of total government debt around the world now offers less than a 1% yield (I can pretty much assure you the lion’s share of the other 19% is in emerging markets).

*Bridgewater Associates, Grappling with New Reality of Zero Bond Yields, July 2020, p. 6

Summary: 0% yields mean that bonds provide neither returns nor risk mitigation

You mentioned plan B?

The Fed’s “plan B” will be more Quantitative Easing (bond-buying), Yield Curve Control, and perhaps even more aggressive use of special purpose vehicles to “buy assets.” I know many believe they will eventually go to Negative Interest Rates, but I believe they see the downside of that effort in other countries and will avoid the same mistake. Perhaps I am being optimistic.

The level of aggressiveness the Fed takes on in future economic distresses will be the most significant economic event(s) of the next decade. The idea that they will rely on the traditional rate cuts is now fantasy – they are out of room. And the idea that we will not have economic distresses defies history. It is incredibly logical and rules-based to assume that we will, and they will act, and because of the rate predicament they are in, will turn to more aggressive actions in the future.

Dude, you’re depressing me

Here is the thing … Just as the Fed’s plan B is a new playbook – more policy tools to make up for the lost flexibility the zero bound has created – investors need a new playbook. The newfound lost efficacy of “bonds that act like bonds” to do anything other than “preserve nominal capital” is but a by-product of central banking policy. We can fight it. We can deny it. We can lie to ourselves about it. Or we can take action.

The Bahnsen Group is going to take action.

What does that mean?

It starts with recognizing what the allocation to “bonds that act like bonds” should be given the new rules. What portion of capital does an investor need or want purely for capital preservation, devoid of risk mitigation, and return generation in any meaningful sense?

Since that number will be less for many (most?) investors, that invites questions as to what to do with the replacement capital. If one brings “bonds that act like bonds” from 40% of their asset allocation to 20%, what does one do with that remaining 20%? Do they add to equity volatility in order to capture the dividend income or growth potential? Do they replace “bonds that act like bonds” with credit? If so, do they do so under the pretense that they have the same risk they had before, or are they self-conscious of different risk dynamics?

Our view is that a full re-setting of risk and reward expectations has to take place – and that out of that process, a lower return tolerance or a higher risk tolerance has to result – one or the other.

And this is the good news – if the conclusion is a “higher risk tolerance” – how can that be modified, mitigated, altered, and managed to be as suitable as possible? Hence, alternative income strategies – with risk – but maybe not the same equity volatility risk that is at the heart of most portfolio anxiety.

More unpacking of this, and what it means on a portfolio level, tomorrow.

A Tale of Two Economies

There is plenty of good news out there, for those who are willing to hear it. Granted, the good news is in the context of the prior bad news, but that is what it is; good news does not become less relevant to our present or our future just because the good news was in response to bad news. And the 11.2% increase in monthly durable goods orders in July was encouraging. Shipments were up 2.4% and capital goods orders were up 1.9%. That is very necessary if there is to be a foundation for a post-COVID economic recovery. Auto sales. New home sales. These things are perhaps surprising, but they are not just good – they are robustly good.

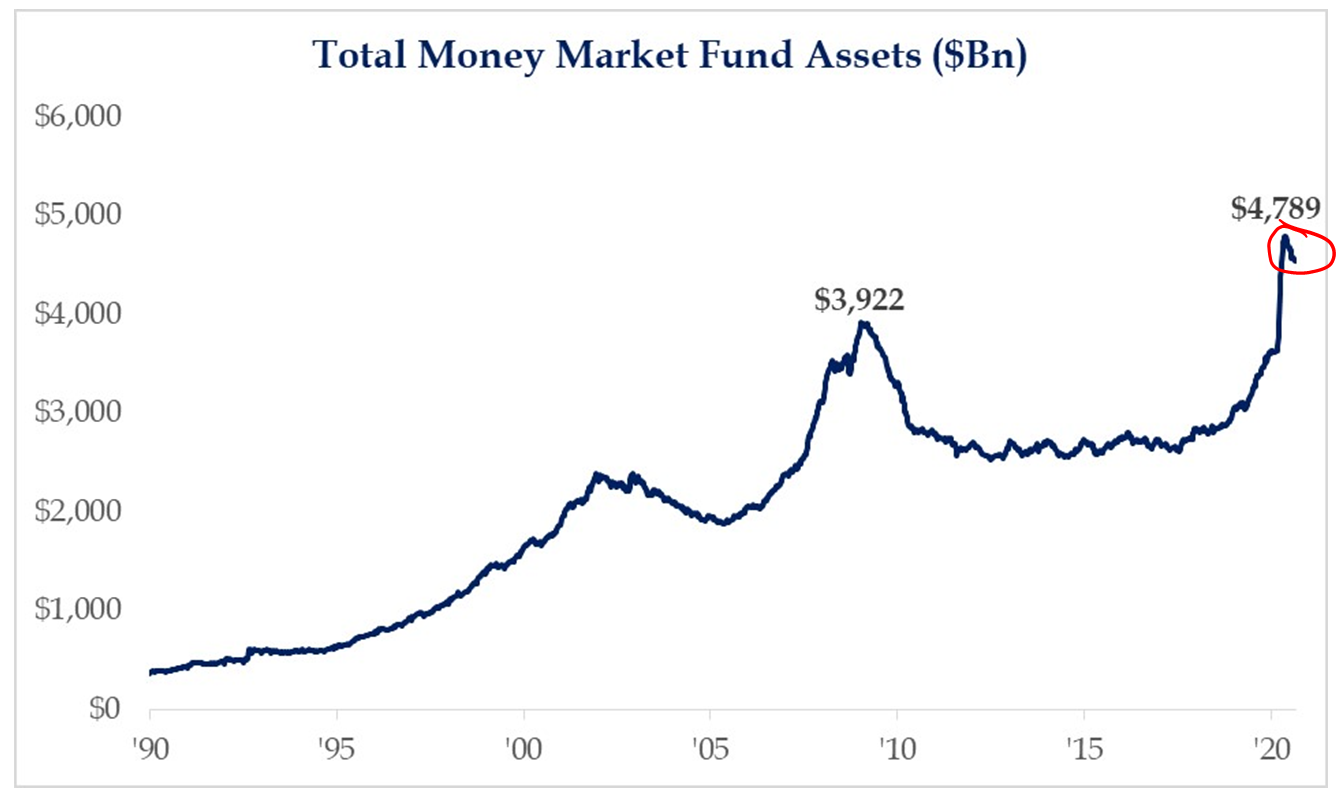

Cash levels in visual form

I reiterated last week the high levels of cash on the sideline right now – and how the comparison to past levels did not contextualize the growth of market capitalization – and that the cash levels have begun to modestly come down. I thought a visual was in order.

*Strategas Research, Daily Macro Brief, August 31, 2020

If you want to worry about something, worry about this

One of the historically biggest indicators of euphoric silliness, and something that is all of a sudden come back into markets, is how excited investors get about something that has no material impact on anything whatsoever, and that is, of course, stock splits. Two very high profile companies split this week, and I have no doubt more are coming (the average stock price in the market is at an all-time high). It excites people because they believe it means something (it doesn’t), their excitement pushes stock prices up, higher prices draw more people in, and then basic math sets in and there are multiple levels of disappointed people.

If investors do not know that 1 x 5 and 5 x 1 both equal the same thing, we have bigger problems than you think. Well, many actually don’t. Be careful of the ramifications.

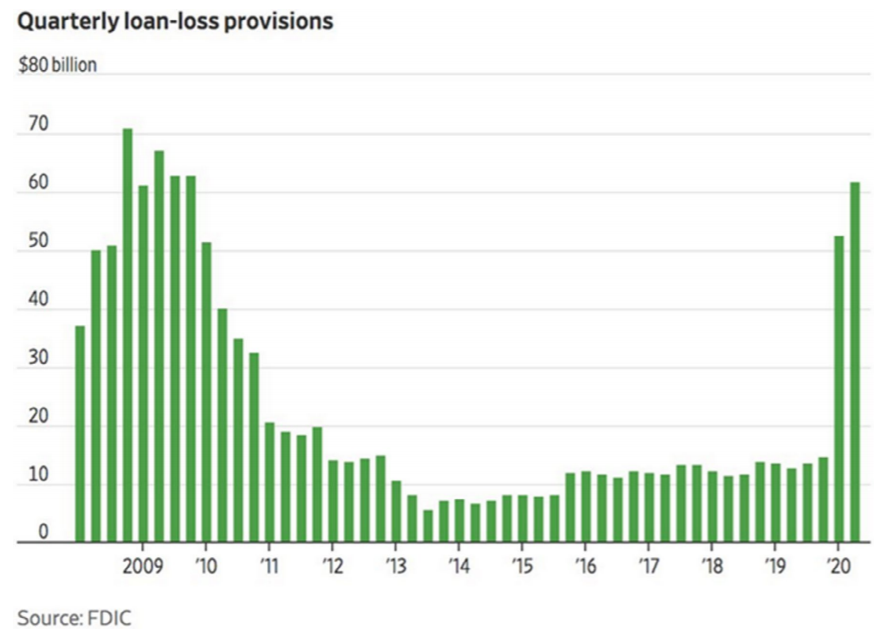

The Case For (and Against) Banks

The struggle that big bank stocks have had this year since the COVID moment began is well-known, and the chart below essentially captures the reason for the struggle, and in my mind, the reason for the opportunity. As you can see, banks took “loan loss provisions” the last two quarters – marks against earnings in anticipation of some loan defaults from customers – basically equal to the provisions they took during the financial crisis! Perhaps the uncertainties of COVID will indeed lead to losses this bad (and banks will already have made provisions against this), but perhaps, those provisions vastly overstate what losses will actually be, and re-statements from excess loss provisions will be a tailwind for future earnings. Time will tell.

*Over My Shoulder, Mauldin Economics, Sept. 2, 2020, p. 3

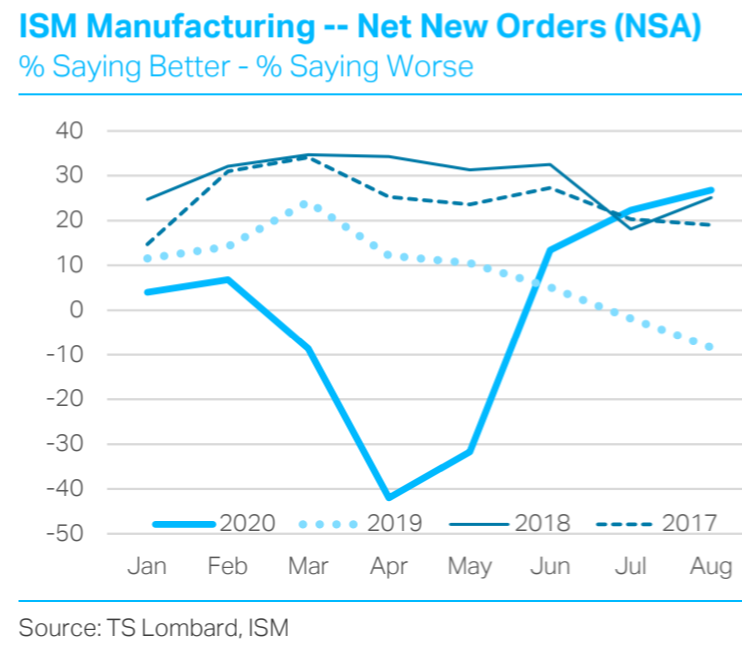

Economic Report Card for the Week

As I wrote last week and will reiterate this week, the manufacturing data (August ISM) was strong, outperforming expectations, and now represents a complete recovery to pre-COVID levels (in New Orders). But what we need to see to believe this is real, sustainable, and even exciting: (1) A catch-up in manufacturing hiring indicative of real manufacturing activity, and (2) An increase in borrowing that reflects businesses primed to lever up for growth. Those two factors would certainly be validating.

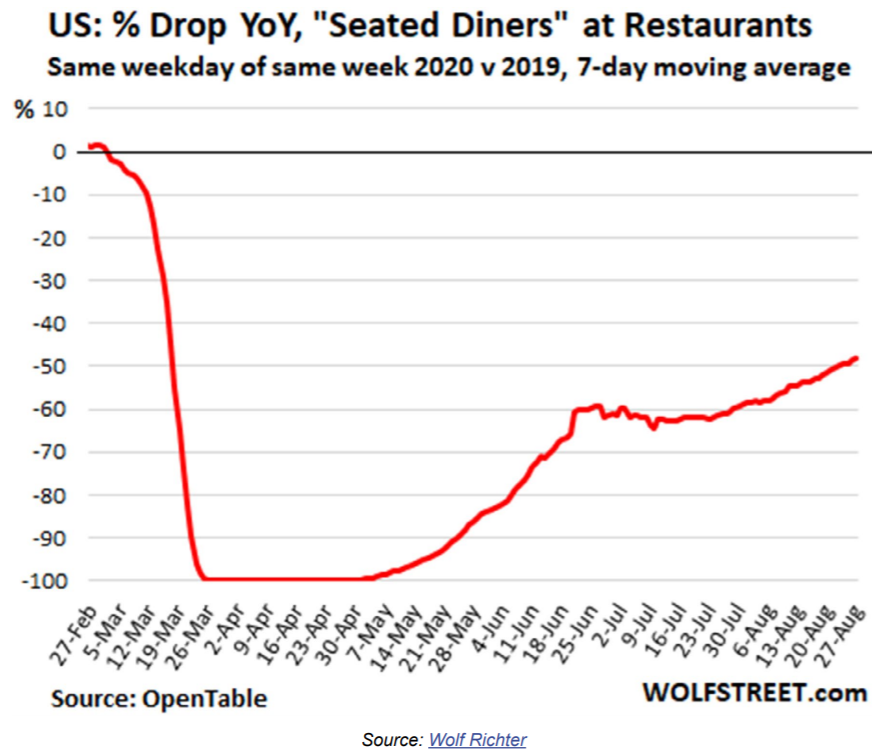

50 down, 50 to go. Put differently, restaurant reservations dropped 100% during the national lockdown, it rebounded 40% when the partial shutdown took place, it flat-lined throughout the middle of the summer behind the partial re-shutdown in California and New York and the modifications in some other states, and now has picked up an additional 50%. So, still down 50% is way, way, way too much; but up 50% is, well, better than not.

And last, but certainly not least, today’s unemployment report for the month of August revealed 1.4 million jobs added in August and an unemployment rate that came down to 8.4%. The number of jobs added were just slightly higher than expected, and the unemployment rate was significantly lower than anticipated. The job losses being identified as “permanent” rose 534,000 (now sitting at 3.4 million people). The structural impact on the labor economy from COVID and the shutdowns will ultimately come down to how right the people labeling their own job loss as temporary vs. permanent end up being.

In the weeds, retail added 250,000 new jobs, bars/restaurants recovered 175,000, and business services added 200,000. Wages are up 4.7% year-over-year, but that is pretty deceiving in that it is what happens when so many low wage jobs disappear from the calculus.

Politics & Money: Beltway Bulls and Bears

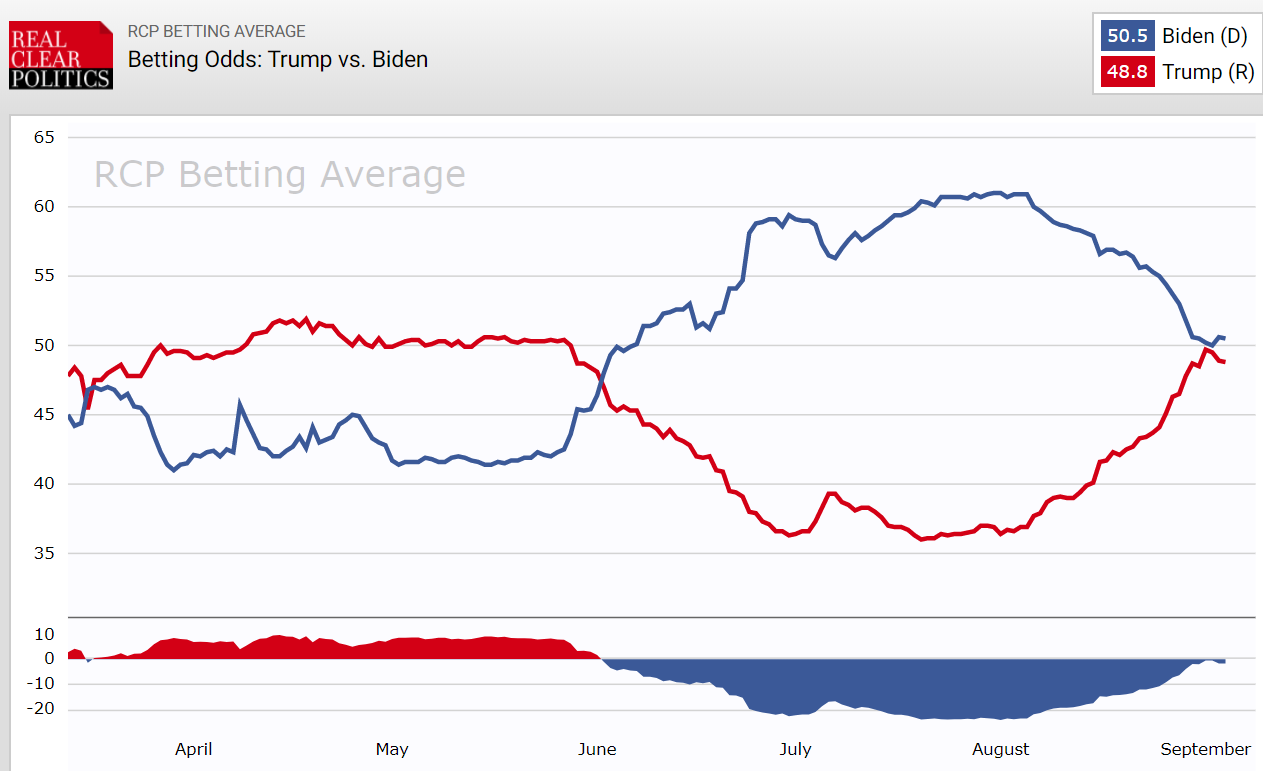

- The Presidential polls have tightened a bit, but not to a point where one could call the race a toss-up. Biden may prefer a 10 point lead to a 7-point one, but Team Trump would prefer Biden have a 3-point lead versus a 7-point one. Some battleground states have moved a little; some not so much. But the betting odds have tightened a great deal, within 2 points now. All things considered, one’s view of the race right now comes down to how much they trust polls, or people’s answers in the polls, and of course what happens over the next two months.

*RealClearPolitics, Election 2020, Sept. 4, 2020

- One element that will not be a huge focal point of my post-Labor Day white paper on market implications of the pending election, but does warrant some real investor consideration, is what it means should we end up with a contested election. I do believe that the odds have substantially increased that it will at least be a close election. A protracted electoral process around recounts, court disputes, and other such noise would certainly create short term havoc in markets. We know of the concern the President has around untabulated mail-in ballots the night of the election (should some of the close battleground states be: (a) Very close, and (b) Have a lot of “pending” mail ballots, it really would be impossible to declare a winner the night of). Those in California know of many races (if not most?) lately taking as much as 2-3 weeks to crystallize results in the last two election cycles. We know Hillary Clinton recently advised Joe Biden “not to concede under any circumstances.” In other words, if it is close, there is ample reason why both candidates may need to let the process play out beyond election night. I would actually not consider it a “possible” outcome that we do not have an official winner on election night; I would consider that the “probable” outcome (that we NOT know the winner on election night) – at least at this juncture. What could/would change that is if one candidate or the other develops a significant lead in the battleground states, but the present tribalization and a low number of undecideds make that very unlikely, in my opinion. Some November uncertainty/volatility, irrespective of actual outcome, seems likely to me.

- Now, let’s say that there is enough clarity on election night to determine that the Republicans will be keeping the Senate … At that point, the uncertainty of a Presidential winner (and potential national unrest) may still spook markets for a time, but the known factor would be “dividend government” – the market’s favorite political scenario. The most market-impacting aspects of a Presidential change would not be as relevant if that were already baked in. But really, election night could create any combination of outcomes here: Two C’s would be most volatile.

- a – Biden winner

- b – Trump winner

- c – Presidential winner unclear

- ———————————–

- a – GOP keeps Senate

- b – Dems take Senate

- c – Senate winner unclear

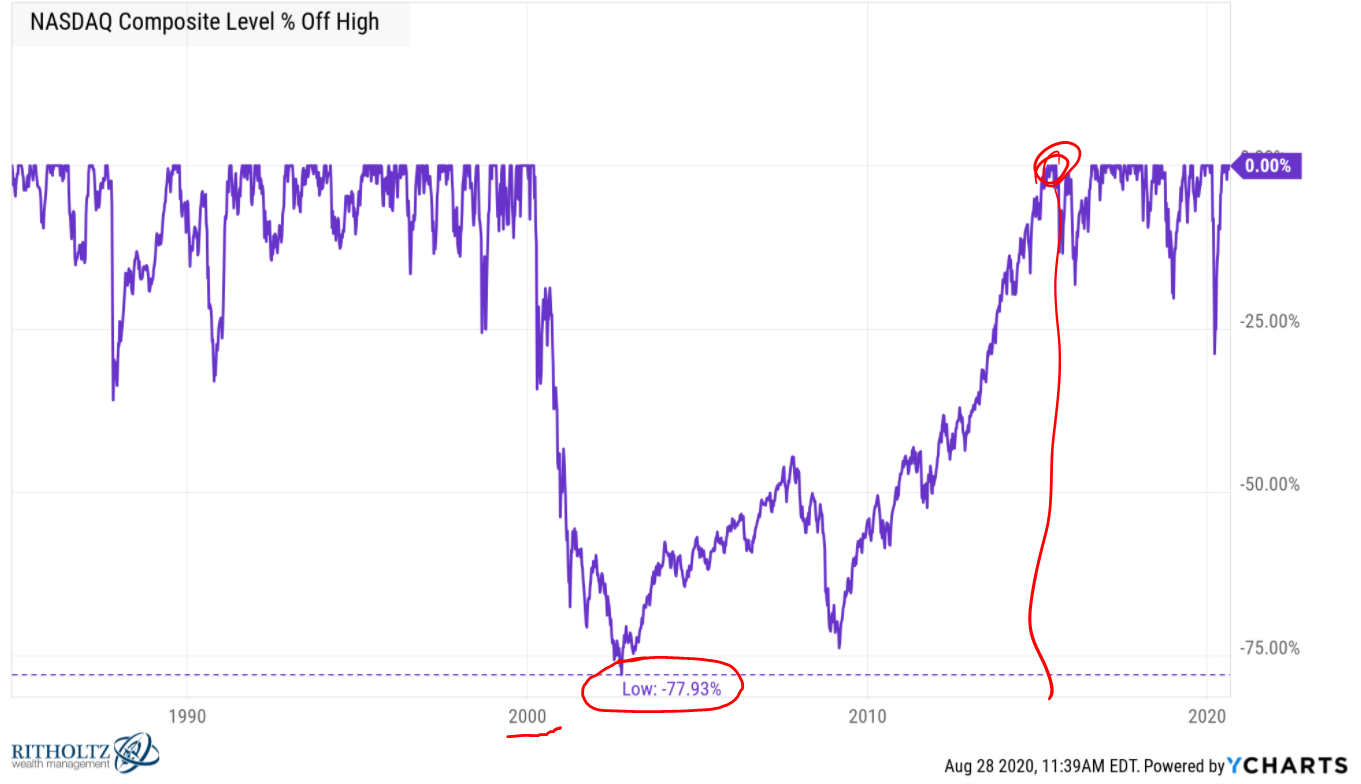

Chart of the Week

I thought this week’s Chart was a powerful reminder of not just how dramatically things can drop when the air is let out of a bubble, but how long it can take until full recovery takes place – in some cases, 15 years – to get back to even. This chart shows the Nasdaq’s move below its high over the last 30+ years.

Again, I have no idea if the distress in the Nasdaq the last two days is the beginning of a significant sell-off, but I do believe one is coming.

Quote of the Week

“To be a success in the predictions business, never write both a number and date on a single sheet of paper.”

~ Alan Greenspan

* * *

I want to wish all of you a wonderful long holiday weekend. Generally, the Labor Day weekend is the sort of transitory hand-off from summer to fall, but so many things didn’t feel normal about summer, and plenty of things don’t feel normal about fall. Not having a USC football game this weekend pretty much keeps this from feeling like Labor Day weekend for me, but it does appear some conferences are ready to stand up and play football this fall (we shall see in the weeks ahead).

With all of the abnormalities that exist right now, I hope you and yours are well, finding the normalcy you need, and ready for some form of a fall season. I love the fall. I hope I will love this year’s, too. Like most things in life, my attitude will determine how that goes.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet

The Bahnsen Group is a team of investment professionals registered with HighTower Securities, LLC, member FINRA, SIPC & HighTower Advisors, LLC a registered investment advisor with the SEC. All securities are offered through HighTower Securities, LLC and advisory services are offered through HighTower Advisors, LLC.

This is not an offer to buy or sell securities. No investment process is free of risk and there is no guarantee that the investment process described herein will be profitable. Investors may lose all of their investments. Past performance is not indicative of current or future performance and is not a guarantee.

This document was created for informational purposes only; the opinions expressed are solely those of the author, and do not represent those of HighTower Advisors, LLC or any of its affiliates.