Dear Valued Clients and Friends,

The bulk of our attention lately has been more market-sensitive, from an analysis of the AI bubble to concerns around private market investing, to the realities index investors face, to the merits of holding to a good investment philosophy even when there is market noise. And since the Dividend Cafe is market commentary for investors, these topics all seem down the middle of the fairway of what we exist to cover. That said, the macroeconomic state of affairs has not gotten a lot of attention lately, and frankly, I miss it.

Now, we did look at the cultural reality behind our labor markets nearly two months ago, and just before that was my last “Fed” issue (one can never get enough discussion of monetary policy; it’s a good thing I’m not single). But you’d have to go back to the summer for the Dividend Cafe’s last exhaustive coverage of inflation, the uncertainty in the labor market, and the impact in the economy from tariffs. So we are ready to “check in” on the economy, and do it in a way that you cannot find in the media. What “way” am I referring to?

Believe it or not … sometimes there are reasons to evaluate the economy besides trying to dunk on a President one does not like, or besides trying to cheerlead for a President one does like. From jobs to inflation to GDP to interest rates, I cannot think of a major economic category or data point that makes its way into the news these days that is not covered for the exclusive purpose of political trolling. This may be the last bipartisan activity left in our society – treating economic data like it is all one big campaign rally (regardless of which side it allegedly helps or hurts).

I want to do an economic check-in because I think it matters for our … wait for it … understanding of the economy! Connecting it to a report card on a Presidency in real time is beyond stupid, since what is up one month may be down next quarter, and what is down at one point in time may be up another. The cause and effect of whatever is being evaluated in the economy matters to how we think about revenues, corporate profits, hiring plans, capital investment, and one-year, two-year, and three-year projections. Looking at a headline data point with no thoughtful analysis merely for the purpose of saying, “look, my guy is crushing it!” – or – “look, your guy is terrible!” – reflects a societal sickness, if you ask me.

But we are healthy and ready for objective analysis in today’s Dividend Cafe. No political idolatry here – just some attempt at gauging where things stand. And while I may be celebrating our commitment to political objectivity in advance of today’s commentary, I will warn you of the big shortcoming before you start reading:

It isn’t like the conclusions about the state of the economy are particularly clear. In fact, some may accuse us of adding to the ambiguity. If so accused, I will probably plead guilty. But the news is what the news is.

So with all that said, let’s jump into the Dividend Cafe …

|

Subscribe on |

It all Starts with Jobs

Tell someone who cannot find a job that they need not worry because “gross domestic product is up 2.7% annualized for the quarter,” and they might punch you in the face. Now, all that said, get an economy that is consistently growing +2.5-3% and you probably do have a pretty decent jobs environment, but that is not exactly how it works. An economy growing well is probably measuring a good jobs environment, as jobs and wages all at once reflect greater production of goods and services (the definition of wealth and growth) and also enhance the sustainability of such (people with jobs and wages are in a position to produce and consume; people without are not). Ultimately, I am very convinced that the state of the jobs market is the foundational data point on which so many other economic data points sit. And I can think of no other data point that both reflects and creates economic conditions more than jobs.

The challenge for 2025 has been the data around those conditions. First, we were exposed to a series of reports in the summer that were vastly better than had been expected in the aftermath of the Liberation Day/trade/tariff adventures. Then we were exposed to a bunch of revisions to those numbers that completely and totally changed the narrative on 2025 jobs health. Then we got a bunch of big picture revisions that totally changed the narrative of 2024 jobs health!!! And then, after a roller coaster of surprisingly good data, then surprisingly bad data, and then the reversal of last year’s good data, we shut down the government for six weeks and went without any public data at all. And in the middle of all this (between the revisions and the shutdown), we fired the person in charge of the Bureau of Labor Statistics, nominated a new person, and rescinded that nomination as a lot of things came to light about their qualifications.

It’s not been a strong few months for credibility around labor market data.

And as I said, this is the most important data point we are after – the one in the middle of this three-ring circus. Good times.

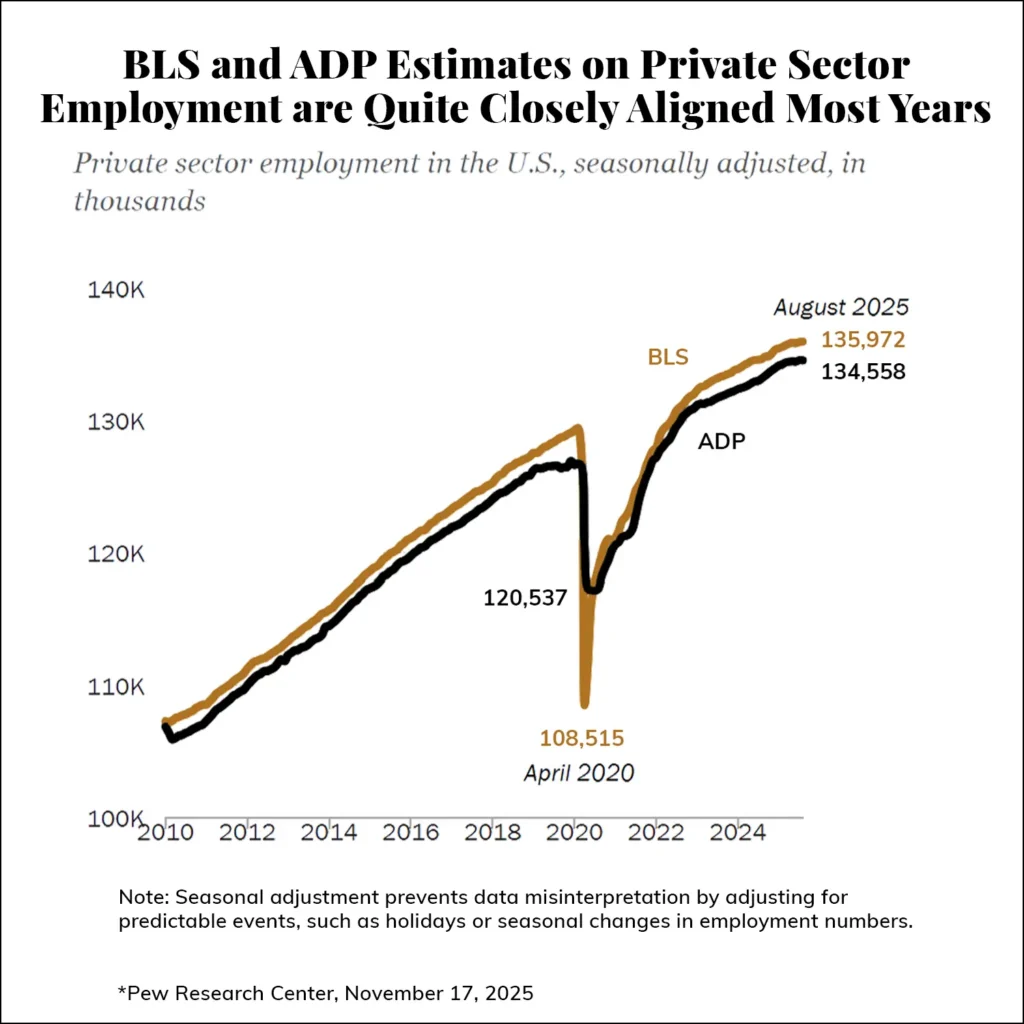

While we have been in this holding pattern with governmental job data (most notably the monthly BLS data), various private-sector data points have become more important than ever. Leading that charge has been the ADP Private Payrolls data. The largest payroll provider in the nation, they have as much real-world data as anyone on W-2 employees actually on a company’s payroll (because they generate the paychecks). How closely correlated has their private sector data been to the data we usually get from the BLS? Well, quite correlated, actually …

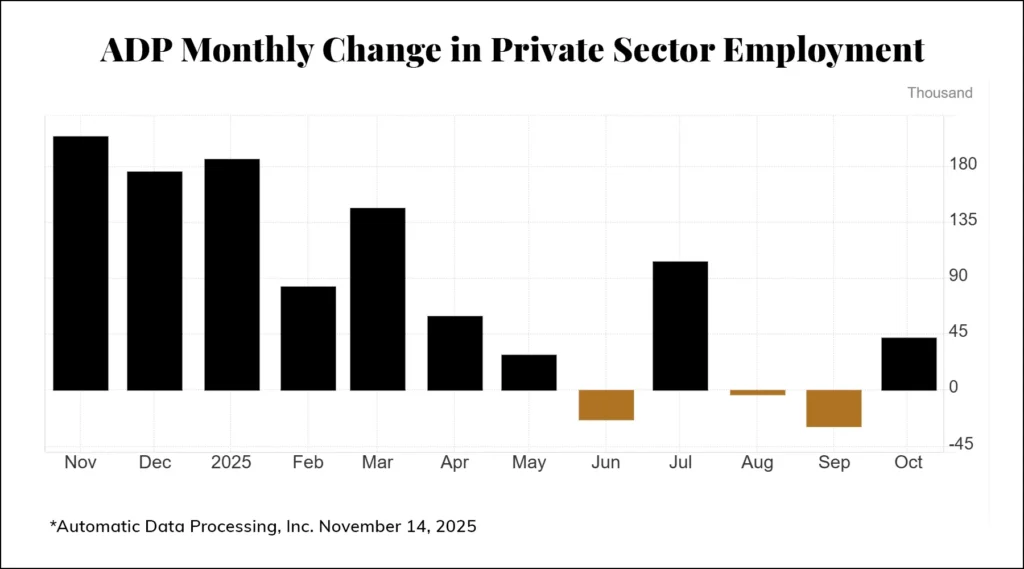

And what has ADP been telling us this year about the state of private sector employment growth? More or less – that there hasn’t been any. The numbers began to decline at the beginning of 2025 and then went negative this summer, basically reflecting a near-zero number from June through October.

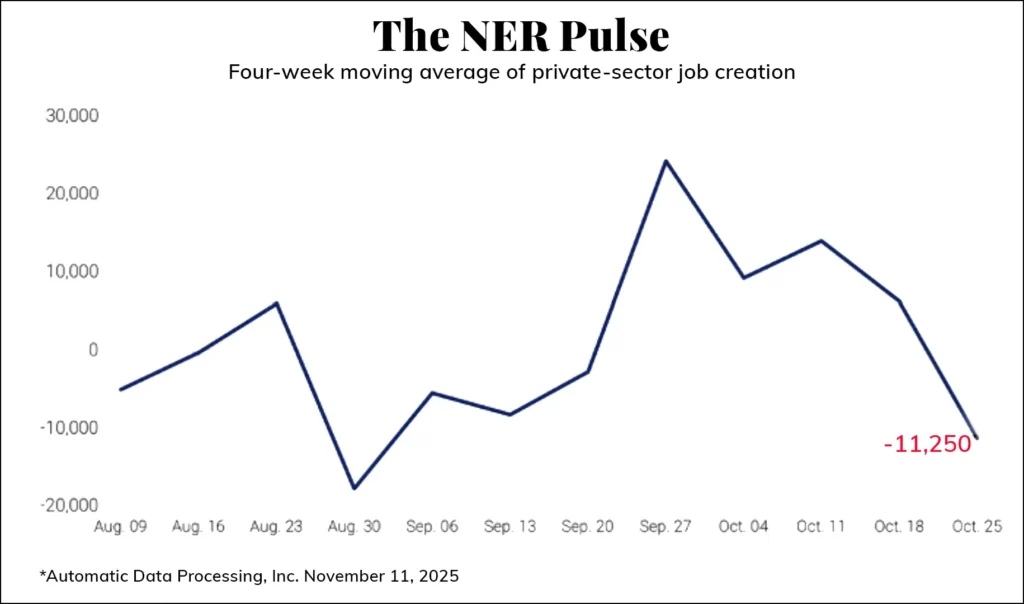

The week-over-week change ADP provides (reflecting four-week averages) indicates a net figure that is negative by about 10,000 jobs (this week’s weekly number was negative 2,500).

One could speculate as to whether or not government sector data (that ADP does not cover) would improve the picture, but between the shutdown and the consummation of mass furloughs from earlier in the year, the more likely scenario is that inclusion of the government sector would make the picture worse, not better.

Government employees impacted by the shutdown are generally considered “employed” in surveys and data that take place during such a furlough. But there were no surveys conducted during the shutdown, and no reports from the period have come out yet, anyway. What is of interest is how earlier in the year “DOGE” programs relevant to federal government workers may have impacted jobs data. This is where there may be a bigger cause for concern. The “Deferred Resignation Program,” offered to two million federal employees, which would have paid them for eight months to stop working immediately, then removed them entirely, was ultimately taken by 154,000 federal employees (6.7% of the federal workforce). The theory that some of the summer’s weak employment was related to this was ultimately disproven, as the BLS treated those receiving their eight months of paid non-work as employed. Even when they do hit the BLS data in these Q4 numbers, they are supposed to be classified as “out of the labor force,” meaning they won’t raise the unemployment rate, but they will lower the size of the labor force.

All in, we only have government jobs down (so far this year) by 97,000. (less than 0.1% of total employment). The various noise around government jobs from DOGE to early voluntary retirements to furloughs to shutdowns have not been a contributor to the soft data, thus far.

Finally, in another private-sector report, the Challenger, Gray & Christmas Job Cut Report for October showed 153,000 job cuts, the highest since 2008. They show 1.1 million announced job cuts since the beginning of the year. About 30% of that is related to DOGE, particularly with government contractors. There is a sense in which the October numbers may include “front-loaded” terminations because companies are more hesitant to fire in November and December due to the holiday season, but it still represented a +175% increase from last year’s number and a +183% increase from September.

I would not take any single report as authoritative or conclusive. What I would say is that the total weight and bend of all reports, taken together, still lead one to either a “mildly cautious” view of labor markets (best case) or a “quite concerned” view (worst case). I don’t see room for a “sky is falling” outlook (from current known data – that can change), but I certainly do not see room for a “everything is rosy and this is the best jobs economy we have ever had.” It simply isn’t the case.

Addendum: On Thursday, the BLS released a report for September, so 6-7-week stale data. It showed 119,000 jobs for September, but with revisions for the summer being revised lower yet again (down by 33,000 more)

Housing is for Activity, not Price

We are annualizing at just over four million existing houses sold per year, the lowest level since the financial crisis, about 22% less than the pre-COVID average annual pace, and 37% less than the pace we saw from 2020-2022. The inventory of existing homes for sale appears to be up 10-11% from a year ago, which has at least put a lid on prices from going much higher. The average time to clear current inventory is 4.4 months, which is much better than it has been, but still below the average level (5-6 months) that we have seen for many years.

On the new housing front, 41% of homebuilders cut prices last month to get product sold, by far the highest we have seen since the pandemic. The average discount to sell a house was 6% off the listing price. This is on top of other incentives, since 65% say they are also using upgrades, closing costs, and mortgage rate buydowns to further prime the pump towards making a transaction happen.

What all this means to me is that the supply problem has modestly improved, but has a long, long way to go, and that the price level is capped for some time, and almost certainly headed modestly lower. And I say that as a good thing, because it is.

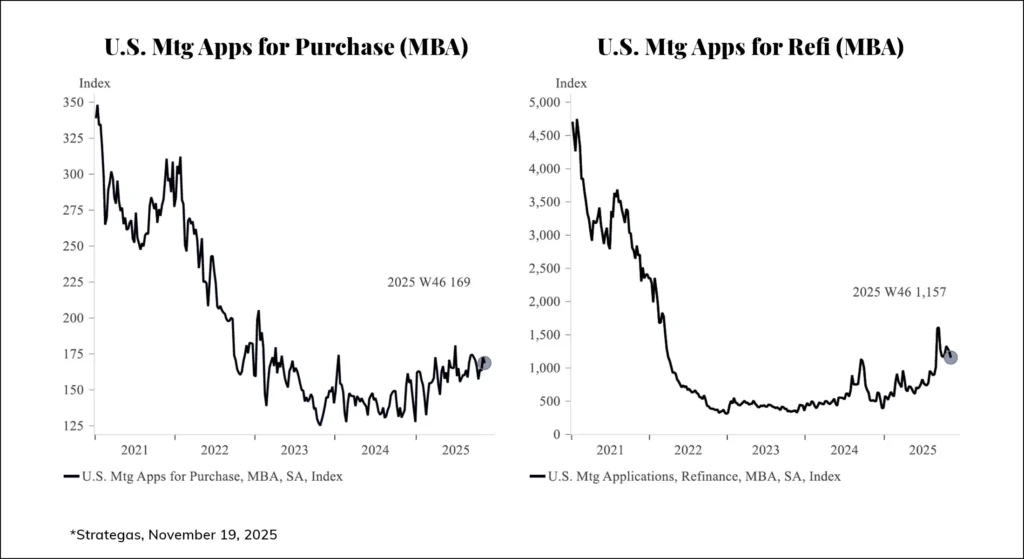

But homebuilder sentiment is very bad, mortgage rates remain much higher than needed to clear the “freeze” on seller activity, and mortgage applications (for purchase and refinance) remain unsurprisingly way, way down.

Housing does not matter to me in an assessment of the economy because I care about people being able to sell their houses at a higher price than they bought them for in recent years, or a higher price than the house was 2, 3, 4, or 5 years ago. Housing matters to the economy because: (a) The absurd price barriers to getting more people in the housing market, reasonably, have led to significant social, cultural, and political anxiety that I find totally avoidable with a proper national perspective on housing; and (b) Limited housing activity as we are seeing eventually bleeds into the real economy.

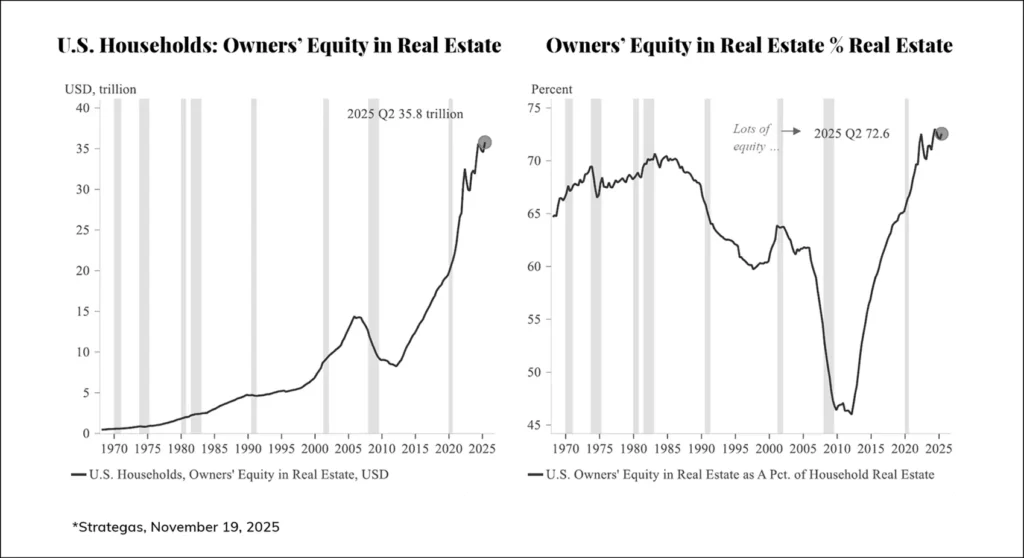

We are not going to see any kind of forced selling glut if housing prices correct by 5-15% (hypothetically). Owners have over $35 trillion in equity in their homes nationwide, and if that dropped to $30 trillion, people would not even notice. The national equity was just $10 trillion fifteen years ago.

The long-running narrative that “healthy housing means healthy price appreciation that is 4-5x the inflation rate and 4-5x annual wage growth” is (a) Dead. (b) Was always dumber than anything I can economically fathom. (c) Corrosive to the national culture, and (d) Unsustainable for anyone with a brain. The sooner home price appreciation hugs the wage growth line and the sooner sticker prices recalibrate to an equilibrium of supply and demand that is sensible, the better off the economy will be.

For those looking for a federal policy solution to this, it is not my belief that there is one. I can think of many things that can be done to make it worse, but very few that can be done (federally) to make it better.

Consumer Strength and the Coming Apart

Long-time readers of the Dividend Cafe know how little I care about consumer metrics, both activity reporting and “confidence” readings that supposedly indicate what consumers are about to do. Well over 90% of the time, “consumer confidence” simply measures if consumers say they feel good before they go spend a bunch of money, or rather, if they don’t feel good before they … also go spend a bunch of money. Their “feeling” is backward-looking, not forward-looking (what we call a lagging indicator, not a leading one); it is sentiment (by definition); and it ignores that what primarily drives consumption is having a job with a paycheck, followed by having things in the universe you want to buy. And having a job is a by-product of production (the more we produce, the more people we employ, and the more things we make for people to consume). In short, I am a disciple of Jean-Baptiste Say to my core, but really, I am a student of human anthropology, as made clear to me in the Garden of Eden, and I do not believe human beings were born in need of incentives to consume. We just seem to do that very well on our own, unless credit is constrained. And I will add: whatever I am saying about human beings’ consumption tendencies, times it by 3 or 4 when you are talking about American human beings. We are a consumerist lot, to say the least.

So, in my frequent endeavors to study markets, macroeconomics, and a wide array of data, I am consistently forced by factors beyond my control to listen to people tell me how important it is to understand how consumers are doing. It is a colossal confusion of cause-and-effect and of fallacious anthropology, but nevertheless it drives so much of modern economic narrative (“bad news, consumers feel bad this month,” or “good news, retail sales were up this month!” – two not all that hypothetical examples in a not very hypothetical sequence).

Alas, the data now is aligned with my construction. Consumer discretionary purchases and standard retail sales (core, which excludes automobile, gas, and restaurants, as well as total retail sales) all indicate strong year-over-year activity. McKinsey and Deloitte each have studies indicating healthy discretionary purchases, even as consumers say they are being cautious, which appears to be something people say as they double-click or Face ID their apple pay. A “cautious” purchase …. my favorite kind. And yes, the recent University of Michigan consumer confidence, which has as good a track record predicting consumer activity as the UC Regents do in hiring football coaches, did drop in the most recent report (from 53.6 to 50.3).

My suggestion is that the consumer is spending money, and the bigger questions for the economy are going to be:

- Short-to-intermediate term: Do jobs and wages hold up to sustain this?

- Intermediate-to-long term: Do we see capital expenditures diversify enough away from AI that our business investment and production supports continued economic activity?

And I would suggest, akin to the housing conclusions above, that if there is an issue to focus on with the consumer, it will be social, political, and cultural … Is consumptive activity for lower and middle income wage earners constrained by price pressures from tariffs and so forth, and is an elevated percentage of disposable income being diverted to rent and housing serving to compress other activity (the answer is yes, by the way) … That seems to me an ongoing thorn in the side of the political ruling party, as higher earners and asset-rich folks feel no such pinch. It is hard to be worried about the cost of bananas and auto fuel when you have no flipping idea what the cost even is, and the top few deciles of wage earners do not. This is not an impediment in any meaningful, marginal way to economic growth – it is a societal comment about which I am very focused.

GDP Growth and All That Jazz

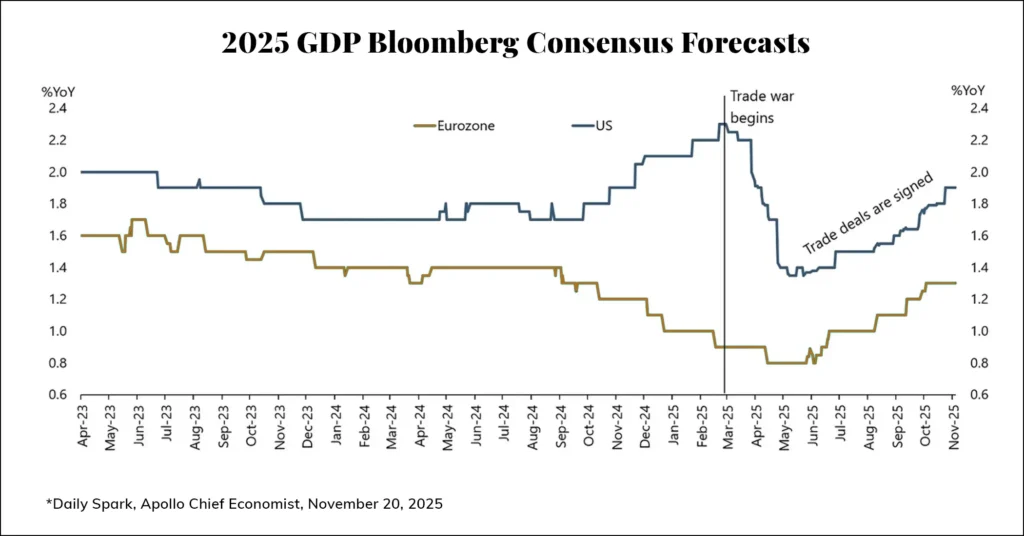

The formula for measuring gross domestic product has been covered a lot in the Dividend Cafe, and why it is a reasonably good measure of a society’s standard of living is something I am happy to defend any time. What has also been covered is how some ingredients within GDP are more “quarter-over-quarter” volatile than others, and how that is part of the deal. This year has lent itself to a ton of lumpiness because of U.S. trade policy which has incentivized “front-running” tariffs which has meant a spike in imports one quarter and a collapse in imports another quarter giving way to big moves up and down in given quarters (the same can be said for inventories), all the while the total annual aggregate number remains, well, muted.

Here you see how consensus forecasts for economic growth (all net of inflation) were picking up after the election, then fell like a lead balloon after “Liberation Day,” and have since modestly recovered, ending somewhere around +1.9% on the year.

Call 2025 a +1.8% year or call it a +2.1% year – and it does seem likely it will be in that window – what we have is an economy growing (so not in recession), and doing so more or less exactly in line with its post-financial crisis average – not better, but not worse – for now.

That post-financial crisis is about 40% less than the American post-WW2 average, though. And the day I stop reminding you of that is the day you should stop reading Dividend Cafe.

Conclusion

The economy is not collapsing.

The economy is not strong.

The economy has some upside possibilities embedded in it – deals with foreign countries resulting in greater-than-expected capital infusion and opportunity for productivity enhancement.

The economy has some downside possibilities embedded in it – tariff impact dragging growth and dull housing activity eventually bleeding into the real economy.

Jobs are not great, but not terrible.

And GDP growth is not great, but not terrible.

And if that is not the most apolitical bunch of accurate but underwhelming descriptors, I don’t know what is.

Quote of the Week

“You ask professors to study things, but you never put them in charge of anything.”

~ Dwight D. Eisenhower

* * *

I was on CNBC Thursday morning talking about Nvidia, AI, and dividend growth. I thought it covered the basics well.

We are excited for Thanksgiving week in the Bahnsen household, to say the least. I will be on the case for the Monday Dividend Cafe, and on Wednesday, as is the annual tradition, we will release the annual Thanksgiving edition of Dividend Cafe, relieving your holiday weekend of a Friday inbox load. In the meantime, USC has a very tough game up in Eugene, Oregon, on Saturday, and I am already thinking about how to make next week’s turkey better than ever. Wishing you and yours a wonderful weekend … Reach out, as always, with any questions you’d like!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet