Dear Valued Clients and Friends,

Two years ago this week, my eldest son graduated from high school, and I used the occasion to draft a letter to graduates. It remains one of our most trafficked Dividend Cafes ever. It was never intended to be only for high school graduates, but rather a broad letter of financial, investment, and practical advice for anyone “entering adult life” (i.e., high school graduates, college graduates, young adults having some sort of paradigm shift in their professional or educational endeavors, etc.). I would argue it has equal application for those entering or leaving the military, entering or leaving trade school, or beginning a new entrepreneurial endeavor, as well.

Two years is a long time. I mean, two years ago, the national debt was barely $31 trillion (oh, the good old days). DEI and ESG were still considered good things by some. And ChatGPT was still shiny. The fact of the matter is that all of the principles I highlighted two years ago remain the top messaging priority today (and I will do a quick recap shortly). But a few new inspirations have entered my mental orbit since I penned that letter two years ago, and it seemed timely to update it. As is often the case, the audience that I feel will benefit from this week’s Dividend Cafe is not at all limited to any one group. No matter what your stage of life is, I think there is some evergreen wisdom here that I encourage all readers to take in.

So with that said, graduates, non-graduates, and people who were already adults when the movie, The Graduate, came out, let’s jump into the Dividend Cafe.

|

Subscribe on |

Credit Cards Have Not Changed in Two Years

My aforementioned letter began with some very practical advice centered around the most crucial of decisions that almost every 20-35 year old will deal with, that will be a bigger factor in their financial peace and opportunity for the next couple decades of life than anything else you can come up with: Whether or not to run up credit card debt. Now, this seems like it shouldn’t have to be included, because perhaps the assumption is that no one chooses to run up credit card debt; rather, they are forced to by challenging circumstances.s

This is, of course, the biggest [you know what] any of us has ever heard. Now, no doubt, there are many who have seen high-interest debt accumulate due to truly difficult and even unavoidable circumstances (unexpected job loss, healthcare, family predicaments, etc.). I have seen more things than most people could imagine, so I recognize the “exceptions” that exist, and yet I find it recklessly irresponsible to treat exceptions as if they were the rule.

The vast, vast, vast majority of credit card balances are a result of discretionary purchases, a disdain for delayed gratification, and a low regard for thrift. Period. The data is unambiguous here.

As I mentioned two years ago, this should be avoided. Like. The. Plague. It strips you of agency, of freedom, of flexibility, of future optionality. It pulls forward into the present what could be much better in the future. It strips you of the mathematical miracle of compounding as you spend more and more years paying off compounding to the lender instead of doing compounding with your assets. Avoid credit card debt, and live within your means. It is good for your health, your mental well-being, your future financial freedom, and your present financial freedom.

And it is good for your soul.

A Problem Not of Your Own Making

Just to get right to the cliff notes, here is what I said were David Bahnsen’s five principles of home ownership two years ago:

- Do not buy a house, condo, or any other form of residential real estate without a minimum of 20% down. 25-30% is better.

- Buy a home if you want to have a great place to live and raise your family, but not because it will make you a lot of money.

- Do not buy a home you can’t afford because of what other people are doing

- Amortize your mortgage and pay down the loan principal if you have any possibility or intention of staying in the home for more than three years.

- A house should be a home, not a trading card.

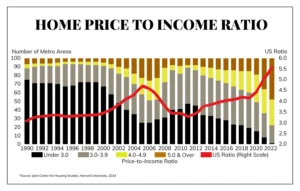

What I would add to this section is that the challenges for young adults in the housing arena are now far worse than they were two years ago, and far worse throughout this entire period than they have ever been. Some have worked hard, secured impressive employment (and compensation), saved diligently for a down payment, preserved their credit score, and earnestly desired a certain starter home or some aspirational residence they can call their own, only to see an affordability headwind that is unfathomable to those not caught in their [boomer] bubble. Between much higher interest rates than we have seen most of the last 25 years, price appreciation that boggles the mind, and a significant challenge of new construction and replacement, a trifecta of issues has made home ownership expensive, intensifying the need to be smart in what you do.

The home appreciation you think you’re missing out on right now, compared to the last generation, is not real. The cost of shelter (all-in) as a percentage of income is dramatically higher than it was 20 years ago, 30 years ago, and 40 years ago. Incomes may rise, but the percentage of one’s income they can or will spend on their home payment has, shall we say, hit a plateau. Houses that averaged 3x one’s gross income are now nearly double that, a 5.6x ratio that is even higher than the 4.5x we peaked at just before the housing bubble.

None of this is to say that one should not buy a home. It is to do two things:

- Temper the expectation about future price appreciation.

- Encourage a mentality and financial framework that fosters fiscally responsible purchasing.

I have said plenty over the years about the policy errors primarily driving this affordability issue with housing. Those things are not your fault (though when you are older, and own your own home, and a second home, and have made it, please do not go to a city council meeting and complain about a new development that may go into your community; stay pro-growth – cradle to grave, not cradle to couch or cradle to golf course).

Investing Behavior

The idea of avoiding panic and euphoria remains timeless, and is hardly reserved for young adults. More “older” adults have blown themselves out from the financial mistakes of panic and/or euphoria than anything you will ever encounter.

But let’s unpack this a little more. Where does panic come from? Fear. Where does euphoria come from? Greed. And are greed and fear financial attributes or are they human character traits and core emotions? The actions of panic and euphoria are fatal. The root causes are embedded in the human condition. So no thyself, and work tirelessly to avoid them.

I would argue that the services of a wealth advisory firm that diligently and relentlessly keeps you from such is a pretty good idea, but then it would sound like I was talking my book and promoting our own services (for more information, please click here). I think I am funny. Anyways, in all seriousness, the steps one takes to avoid the destructive errors of panic and euphoria include, besides the use of a wealth advisor who will not lie to you, an actual portfolio philosophy (imagine that), a written investment plan, an asset allocation that keeps the things that could go wrong from destroying the things that can go right, and a discipline that transcends the emotions of day-to-day headlines. It avoids get-rich-quick schemes, and it has the moral fortitude not to look at people who have seemingly gamed the system well as something to covet.

Covetousness is a sin. Don’t do it. And most people with tales that you think you want to covet are lying. One day, I will write a book.

Some Dividend Meat on the Investment Bone

If you feel ready to understand how capital compounds over time, I encourage you to look into dividend growth investing. It is hard to make money by being a minority owner of a business unless that company makes money. And if the company does make money, it has to do something with its profits. Dividends are not about making money or not making money – they are an option (the preferred option) as to what to do with these profits. Sure, companies need to retain some earnings to fortify their balance sheet, to reinvest in the business (for a period), and maybe to buy back stock every now and then if done responsibly and strategically. But dividends represent real profits of a business that become a real profit to you, not a permanently delayed claim on future profits. Of course, one could always sell a company at a profit to achieve a real profit, but then what happens? You own less of the company! If it is a good company, why would you want to own less? A dividend is a perpetual risk reduction, and it never forces you to dilute or divest your ownership. Any realized capital gain is, always and forever, reduced ownership (this is a tautology).

Accumulating a diversified and high-conviction portfolio of perpetually growing dividends from masterfully run businesses is an extraordinary way to compound capital over time, to create a future stream of income, and to build your own balance sheet. If you need a resource to better understand it, you’re already in the right place.

Did Someone Say Crypto?

Yes, actually, a lot of people have. And I still owe the Dividend Cafe an exhaustive treatment of this 2020s fad that so few understand and so many love. But for our purposes today, ask yourself these questions:

- Is the reason I may want to buy some cryptocurrency, digital coin, or other “asset” that has a tech-sounding name to it because I believe it will get me rich quickly?

- If I want to buy something that I believe will appreciate in value quickly, do I have an answer as to WHY I believe it will appreciate quickly?

Some may claim to have a fundamental, disciplined, theoretical case for ownership, and some may believe they can answer the “why” of it all. They will make their decision accordingly and live with the consequences. You will find that most people who have a lot of conviction in their thesis do not feel a big need to argue about it on social media. But regardless, if you are in the camp of, “Well, some of my friends made a lot from XYZ (whatever XYZ is), and I want to make a lot quickly even if I do not understand it,” I simply recommend you pass. Know what you own, and why you own it.

Mark Cuban said out of the dotcom moment as company after company threw million-dollar parties with almost no revenue, just in time for the Nasdaq bubble to burst and trillions of dollars to be set on fire, never to recover: “The bigger the party, the bigger the scam.” Well, I see a 2025 corollary to be: “The shinier the object, the bigger the scam.” Pump and dump is not the stuff sustainable investments are made of. Credibility matters. Avoid the grifters. Sometimes they sound smart. They aren’t.

Last but not Least

Even though I am a professional wealth advisor who has devoted my life and career to using financial markets as a tool to create solutions for people who have varying goals and objectives, the thing I am most passionate about as I close this letter is not investment-related, per se. Maybe because I was in my 40s when I wrote that last letter and am in my 50s now, I feel a bit more jaded, or at least more concerned. Is it Artificial Intelligence that I am concerned about? Is it the get-rich-quick grift I see all around me? Is it the housing affordability I talked about earlier? Is it crypto shenanigans? Is it class warfare? Is it a resentment of productive economic activity? Is it the national debt? Is it economic ignorance?

All of these things float across my inbox and your headlines and around my mental orbit, all the time.

But I am not worried about AI. It will create more jobs than it makes obsolete.

I am not worried about get-rich-quick nonsense. People learn from their mistakes, and candidly, they often don’t learn apart from them.

What I most worry about is a rejection of the dynamism, optimism, and productivity that gives our lives meaning. Don’t do that. As alluring as daydreaming about a career as a social-media influencer may be, avoid the cynicism that creates such an idea to begin with. View risk-taking as a noble thing, even when risk beats reward. Root everything you do in your life and career to virtue, knowing that the most valuable asset you have is your own character – and it should never be for sale. Ever. Be a truth-teller, even when it hurts. Treat others with civility and respect, even if they have different views from you or, God forbid, root for different sports teams.

Go produce goods and services that meet a human need. And have the time of your life doing it. That’s what this is supposed to be about.

Quote of the Week

“Develop into a lifelong self-learner through voracious reading; cultivate curiosity and strive to become a little wiser every day.”

~ Charlie Munger

* * *

I am stewing on a few different ideas for next week’s Dividend Cafe, but I do know that Monday’s is going to have a lot to cover around the economy, the jobs data, Elon/ President Trump, and so much more. In the meantime, enjoy your weekends and reach out anytime. This virtuous pursuit of the good life is the core of what we believe in at The Bahnsen Group. One might even say that to that end we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet