Dear Valued Clients and Friends,

I think we can consider this the official end of summer. Today is the last market day of August, we are entering Labor Day weekend, and most importantly, college football season starts tomorrow. I am sure many of you wish this would be another Dividend Cafe where I combine the history of USC football with the history of markets (a Div Cafe classic if I do say so myself), but alas, that was a one-and-done! It doesn’t mean we don’t have some special things in store!

We have a very strange market to cover this week: Some discussion about the future, the state of the economy, the cost of protection, the truth about the national debt, and so much more. It isn’t very topically focused, but it sure covers a lot of fun topics.

Jump on into the Dividend Cafe!

|

Subscribe on |

Who had this on their bingo card?

Microsoft, Amazon, Nvidia, Google, and Tesla have all come out of this earnings season below their price before earnings season, and in some cases, meaningfully below it, and yet the total market is higher! It has been an extraordinary month for non-tech sectors, an improved breadth in markets, and, yes, strong performance across the defensive sectors (health care, consumer staples, utilities, and REITs).

Financials had dipped in the prior dip but have since made that up (and then some). Technology overall dipped a lot and has mostly made that up, despite the laggards in five of the seven “magnificent seven” mega-cap names. The real leadership has been defensives.

But that was August

Clients and long-time readers should know how I feel about this, but it is worth repeating: I don’t have the foggiest idea what will happen within markets in September or in the final months of the year. What happened in August is about what happened last month, not what will happen next month. And anyone who believes immediate past performance offers some predictive value not only needs to read a compliance disclaimer but study history too. It doesn’t. It never has. It never will.

Now, is there a reason to believe that a position of leadership in the market is due for a transition? Well, there are about a hundred reasons if one puts stock in things like valuation, historical ratios, relationships, etc. As a fundamentalist, I am very inclined to say that a shift to more value-oriented sectors relative to over-priced growth sectors is sensible, predictable, and even inevitable. I am just not inclined to say it happens this month. But so far, yes, it appears to be a meaningful indicator of market leadership transition.

A question about the future

I have pointed out several times that while there are different circumstances and particulars that have created different outcomes, the more frequent result in the immediate year after the Fed begins cutting rates is for markets to go down. Exceptions have been highlighted for what they were – unexpected stimulus, etc. But the majority of the time a rate-cutting cycle begins it is in response to weakening economic conditions, thereby not giving the market an assurance of a rally just because the discount rate comes down. If the weakening economic conditions the Fed is trying to get in front of are reducing corporate profits it is quite likely that markets are going down regardless of the interest rate.

But a fair question is this: Does this mean that rate cuts only precede tough market conditions if the economy is in, or going into, a recession? More or less, this has been the historical reality. However, despite a high correlation between an actual recession and downward pressure on corporate earnings (which would weaken markets), I do believe it is possible to have weakening earnings without a recession. I wouldn’t bet on it, but it can happen. The important things to remember about this rate-cutting cycle (in no particular order):

- Markets didn’t exactly decline a lot during the rate-hiking cycle; therefore, there may be less room to rebound when the cutting begins

- The markets have had more time to price in these pending rate cuts than almost any period like this, ever. This “pause” has literally lasted fifteen months – not exactly “shock and awe” monetary policy.

- Economic conditions have slowed but not weakened. They have softened but not fallen. They are less robust but not terrible. In other words, no one really knows what is happening next. A 4.3% unemployment rate that stays around 4% is going to prove a lot more benign than one that gets to 5% and stays north of there for a long period.

- S&P earnings growth is already expected to be 13% next year. S&P valuations are already north of 20x. Multiple expansion is not likely, regardless of economic fundamentals in the near future.

- There is another monetary tool on the table besides just interest rates, and that is quantitative easing. The use of that tool, either to continue tightening, or to stop tightening, or to start loosening, is a huge wildcard.

A loss of income you forgot about

When we talk about risk assets going higher because interest rates are lower, we are focused on (a) valuation (i.e., lower rates are supposed to mean higher valuations), and (b) debt service costs (i.e., borrowers pay less in interest when rates come down). What we always, always, always forget in this conversation is that one person’s debt is another person’s asset, and one person’s expense is another person’s income. Leveraged borrowers may save in interest expense, but there will also be a loss of income to account for on company balance sheets, insurance portfolios, the bank accounts of savers, etc. It’s almost like there is no such thing as a free lunch.

Not out of the woods

The VIX (so-called fear index) spent most of the year between $12 and $13, which is extremely low. In the market sell-off of late July/early August, it exploded higher but then settled down in the last few weeks. But it should be noted (and I say this as a good thing, not a bad thing), it settled back down around $16, not $12 or $13. Protection is not selling for an astronomical price like the first week of August, nor is it selling for almost free like it was earlier in the year.

International exposure

We continue to believe the profit growth, equity valuations, market demographics, and leverage to a potentially weakening U.S. dollar are best in emerging markets relative to other international markets. There may be pockets of opportunity in Europe, Japan, the UK, and China, but there are significant headwinds, as well, and markets have clearly felt the same way for over a decade. To the extent there is appetite for this risk, and the goal is growth, not stability or current income, emerging markets provide the better risk/reward trade-off internationally than developed country options. This may be advice on a repeat loop, but it still strikes us as good advice.

A sneak peak of awfulness

I have begun to work on my quadrennial white paper on the pending election and its impact on markets. A theme that will be present in the paper is that for all of the policy differences between the two candidates, the one area where no investor is likely to anticipate significant daylight between the two is the impact on the national debt. In other words, if one believes (as I do) that the most significant economic issue facing the country long-term is the impact on growth that excessive indebtedness represents, this just isn’t an election where that will be discussed, addressed, debated, tackled, or remedied. It may very well be an intense topic for debate in the 2028 election, but 2024 is not that year (sad to say).

That said, I believe a few factoids here are worth understanding:

- The current pace of > $1 trillion annual budget deficits are BEST CASE, and they assume NO RECESSION. The numbers are, at least for now, even worse than $1 trillion, and the economy is growing.

- We will see 200% debt-to-GDP per all estimates any left-wing, right-wing, no-wing, two-wing, chicken-wing, or buffalo-wing analyst, think tank, economist, or milkman has to say. It is simply unavoidable because of math, barring a significant intentional effort to keep it from happening.

- It took 232 years to reach out first $10 trillion of debt. it took nine years to reach the next $10 trillion. It took four years to reach the next $10 trillion. It takes just months now to add each new trillion on top.

Treasury worries

For all of the talk about foreigners not wanting U.S. debt anymore, with $27 trillion of U.S. public debt outstanding, over the last nine years when China’s level of ownership of U.S. debt peaked, their holdings of treasuries have dropped by a grand total of $400 billion.

Treasury worries part two

One of the bigger concerns than who would buy U.S. debt has been the cost of debt in a rising rate environment. Indeed, the U.S. was spending $1 billion per day on interest a few years ago and spends $2 billion per day now (per day, in case you missed it when I said it a few words ago). But that said, 22% of U.S. debt is in Treasury bills – ultra short-term paper. At $6 trillion paying, let’s call it 5%, and let’s say the Fed Funds rate is 3% by the end of 2025, that means $6tn will roll into 2% cheaper paper, meaning $120 billion of annual savings in interest expense …

Why does the Treasury need a cooperative central bank? That’s why!

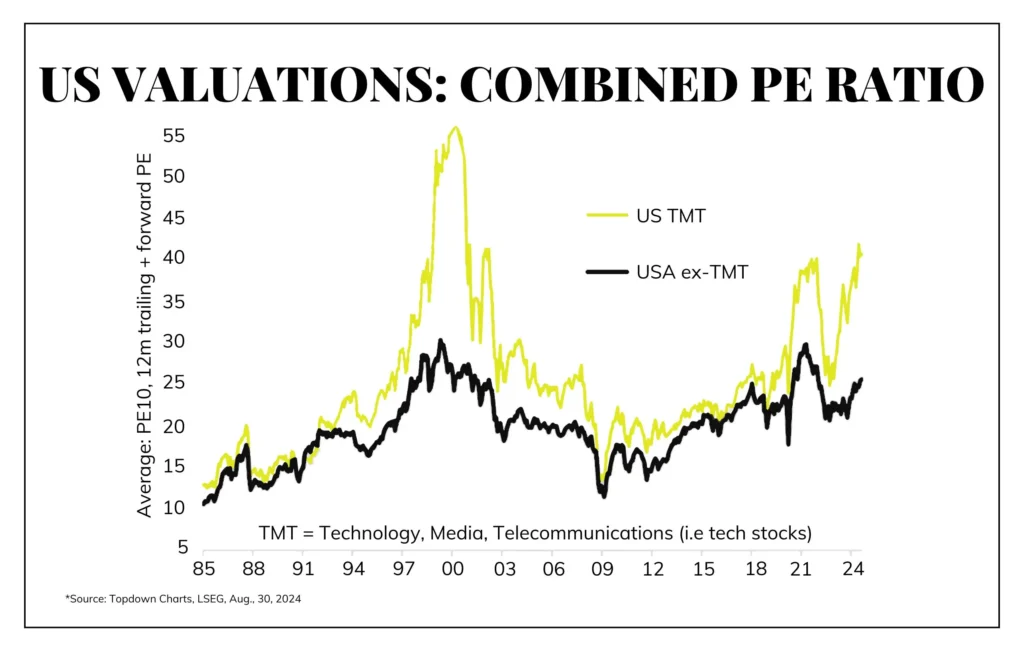

Chart of the Week

Again, this needs to be pointed out when we talk about excess S&P 500 valuations… Not all S&P sectors are created equal in the valuation discussion. Or close.

Quote of the Week

“I should note that the cemetery for seers has a huge section set aside for macro forecasters.”

—Warren Buffett

* * *

I am excited for September because I consider the fall the greatest time of year. I felt that way when I was young because I loved school and hated summer. And I feel that way now that I am old because I love football, and the fall weather is my favorite. I do not know what to expect when USC takes on LSU this Sunday, but I do know what Joleen and I will be doing. In the meantime, enjoy your long Labor Day weekend. I hope your summer seasons are ending with joy and gratitude, and I cannot wait for what lies ahead this autumn (and football season). Fight on! (to that end, we work, literally).

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet