Dear Valued Clients and Friends –

Summer is here, graduates are free, and the only thing holding people back are $13 cheeseburgers and the end of campus protests. But I am sure everyone is excited for their summers, from graduates ready to go explore the world to those of us in NYC who just love walking around midtown in a suit, wondering when they will invent an “outdoor air conditioner.” As one who believes “freon” was a more remarkable invention than the iPhone, it’s a hot time of year. But markets never sleep, and the lessons one can extract from the study of markets don’t take a summer break. So grab your iced tea and let’s jump on into the Dividend Cafe!

|

Subscribe on |

Our old friend, Minsky

I confess that prior to the financial crisis, I had not read a ton of Hyman Minsky. There is much in his work I am not super fond of, and I naively believed in my formative years of studying economics that Minsky could be skipped because I had read so much Keynes. In other words, I didn’t need someone not named Keynes to know why I was not a Keynesian, and Minsky was another post-war Keynesian elite who believed [wrongly] in government intervention in markets as a cure to cyclical challenges.

But during and after the financial crisis, Paul McCulley, who then worked in the same building I did (he was Chief Macro Economist at Pimco at the time, and I was a Managing Director at Morgan Stanley in Newport Beach, and we were in the same building), turned me on to Minsky. Now, Paul is another SERIOUS Keynesian, and by that, I mean that Bill Gross used to say that “Paul is more Keynesian than Keynes.” Paul is probably the economist I have enjoyed reading the most over the years, and I don’t think I ever agreed with a single thing he said (as a matter of foundation). He was utterly brilliant, rigorous in his analysis, an infectiously interesting writer, and just committed to a set of first principles that were wrong in every way imaginable. And I learned a lot from him.

Anyway, Paul McCulley introduced me to the concept of the Minsky Moment in 2008 as he wrote with precision about this basic, seemingly indisputable idea: “Stability breeds instability.” I will always be grateful to McCulley for introducing me to Minsky and, ultimately to Minsky for his remarkable work on the fragility of financial markets.

The term “Minsky moment” refers to the point at which financial markets move from stability to instability. For Minsky, the period of stability creates the complacency that makes instability inevitable. Now, I do not agree with Minsky on how to remedy this dynamic (i.e., government intervention), but his framework of understanding debt as either hedge borrowing, speculative borrowing, or Ponzi borrowing is unimprovable.

Anyways, as you will soon see, I am very much of the opinion that a long benign period in equity investing and particularly the multiple expansion of technology has bred a complacency that has intensified the instability of the markets for many. Now, Minsky really focused on the role of debt in exacerbating systemic instability, and for good reason. This is the big reason that merely referring to “an overpriced asset” as a Minsky moment or a destabilizer is not quite accurate. That overpriced asset has to draw enough borrowing to it that destabilizes adjacently in the event of distress. And I simply do not believe there is evidence of that in the present moment.

Paradoxical outlook

It is not entirely unfair to say that my lay of the land looks something like this:

- Current pricing of the technology sector – high risk to investors short-term

- Current pricing of the technology sector – low risk to the economy long-term

- Current level of government debt – low risk to investors short-term

- Current level of government debt – high risk to the economy long-term

There are two main things on my radar—current market pricing and long-term government indebtedness. One is, I believe, a short-term market risk and not a long-term economic risk; the other is a long-term economic risk and not a short-term market risk. Good times.

The lay of the risk land

Credit spreads are currently 3.15%, just 10 basis points or so off of the lowest level we have seen. Much of 2022 saw spreads well above 5%

The VIX is currently around 13, near the lowest it has been since 2019.

Correlations among stocks have become very low, which is a good opportunity for stock selection but a flag for indexers. The correlation between stocks and bonds is very high, which is a flag for allocators.

The S&P dropped a whopping -5.5% in April, representing its largest drawdown of the year so far (i.e. a drop from any peak point to any trough point). I hope readers know that when I describe a -5.5% drawdown as “whopping”, I am either being sarcastic or revealing myself as one who doesn’t read history. And I read history. I may not read science fiction, or novels, or romance, or crossword puzzles, but I do read history. A -5.5% drawdown is barely worthy of being called a drawdown. The S&P drew down -33.8% in early 2020 but that was abnormal the other way – you know, with them shutting down the world and stuff. It drew down -25.4% in 2022, but that was a big negative year for markets. It even drew down -10.3% last year, and last year was a big positive year for markets. But down -10.3% in the midst of a positive year is extremely common – some would call it par for the course.

Tight spreads, a low VIX, high correlations, and little to no drawdown are all part and parcel of the same market dynamic—one filled with optimism, hope, positive assumptions, low regard for risk and valuation, and complacency about circumstances not warranted by reality.

I told you I read history

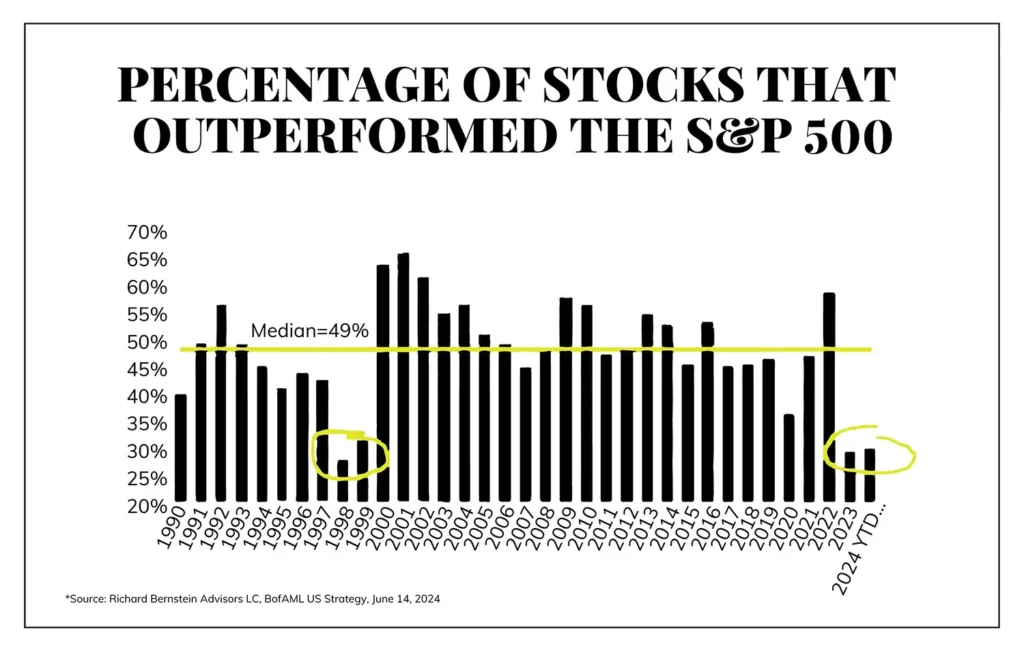

I have addressed the market’s top-heaviness a lot. It is a challenging risk metric because it doesn’t feel like a risk reflection until it is revealed as such in hindsight.

But across the board, I think it is safe to say that investors seem very calm about certain circumstances that perhaps should not be taken so calmly. Low volatility is one thing; complacency is another.

And this, to me, is its own message to indexers:

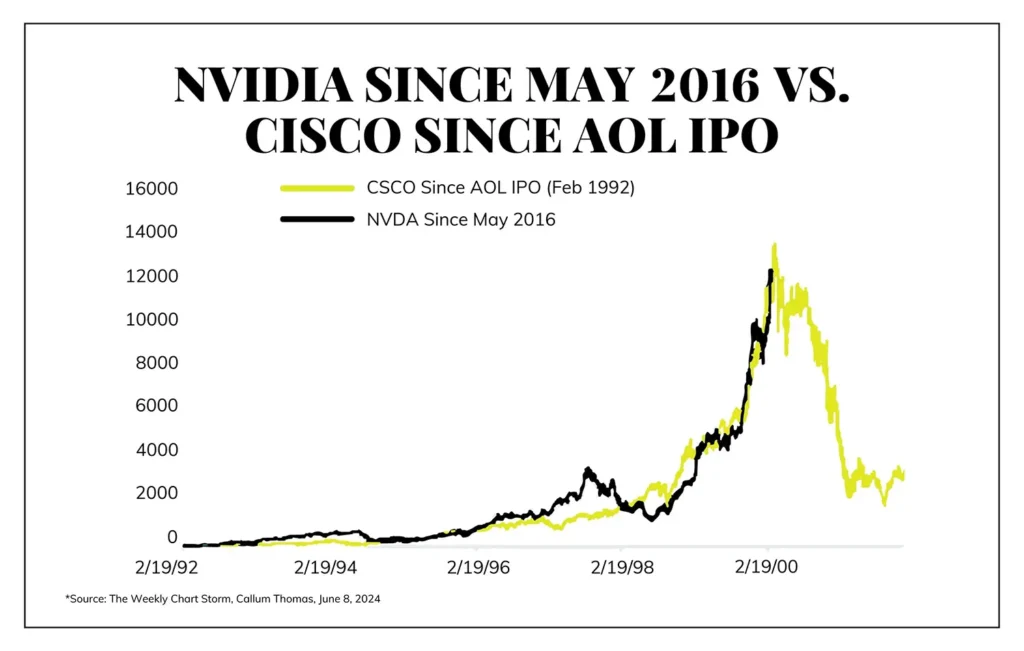

And I guess you could say this is worth looking at, too:

In Conclusion

Two things are true at once: there is a complacency amongst risk-takers right now that is concerning, and that is likely not systemic. That risk is concentrated with those taking it and, in my opinion, is not going to end well. But on the other hand, the Minsky moment, whereby the stability, peace, and good times of this tech moment lead to a much more unstable outcome, does not appear to be fully at play here. One thing that has to be said for the excesses of the tech world over the years – they have almost entirely been EQUITY driven, with very little DEBT component. And debt creates financial fragility. Debt creates Minsky moments.

The governments of the world have not just monopolized entire industries and segments of public life—they may have monopolized Minsky moments, too.

Now a few other items worth an honorable mention …

Sign of the Times

Ten years ago, just 3% of the volume of total U.S. shares traded on the stock market were worth less than $1 (so-called “penny stocks” where volatility and speculation are extremely high and reliability and common sense are extremely low). Today, 14% of such volume is in these devices of speculation. So if one believes that investors are all thinking straight and behaving wisely at the same time that the volume of penny stock trading has risen by over 400%, I have a bridge to sell (or take public as a penny stock).

Yield curve reminder

In March 2022, the yield on a 2-year Treasury went higher than the yield on a 10-year Treasury. We have now been “inverted” that way for 27 consecutive months, the longest streak of a continually inverted yield curve in history.

Geopolitical convergence myth

Let’s be extremely clear about the state of global politics – just as the U.S. is deeply polarized and divided, so is the rest of the globe lacking in any sort of monolithic uniformity. Yes, various populist or right-wing parties experienced electoral pick-ups last week in the European Union. But at the same time, a very left-wing party and candidate were just elected the new President of Mexico. The more market-friendly regime in India (and its long-time Prime Minister, Narendra Modi) significantly underperformed expectations and now faces a coalitional government versus the consensus that has been anticipated. Polling indicates conservatives in the UK are facing an electoral bloodbath in a few weeks, even as things went terribly for far-left parties in Germany, Spain, France, and Italy a week ago.

It is extremely rare that a lot of political rhythms line up together at the same time, domestically or globally. It can happen, but it is rare. And I would say it is even more rare in a country, and a world, as divided as we are now. I suspect our own elections in the U.S. face a similar dynamic that the globe is seeing now – divergence and unpredictability that reflects a lack of consensus, not the existence of one.

Domestic political convergence

I do plan to continue the tradition of a pretty extensive white paper this August or September about the election and its impact on the economy and markets. I believe it is going to be a valuable piece for readers this year and I candidly love writing it. There are all sorts of differences in the candidates and the parties these days about issues, temperament, personality, focus, and ideology. There are specific issues that warrant specific analysis of policy differences. The one area where I am not convinced there is a lot of difference is the approach to budget deficits and government spending. I suppose what money is spent on or the composition of the deficit could or would look different under each possible political regime or combination, but where I believe we can be politically agnostic is in our expectations of ongoing trillion-dollar annual deficits attached to a $34 trillion current debt.

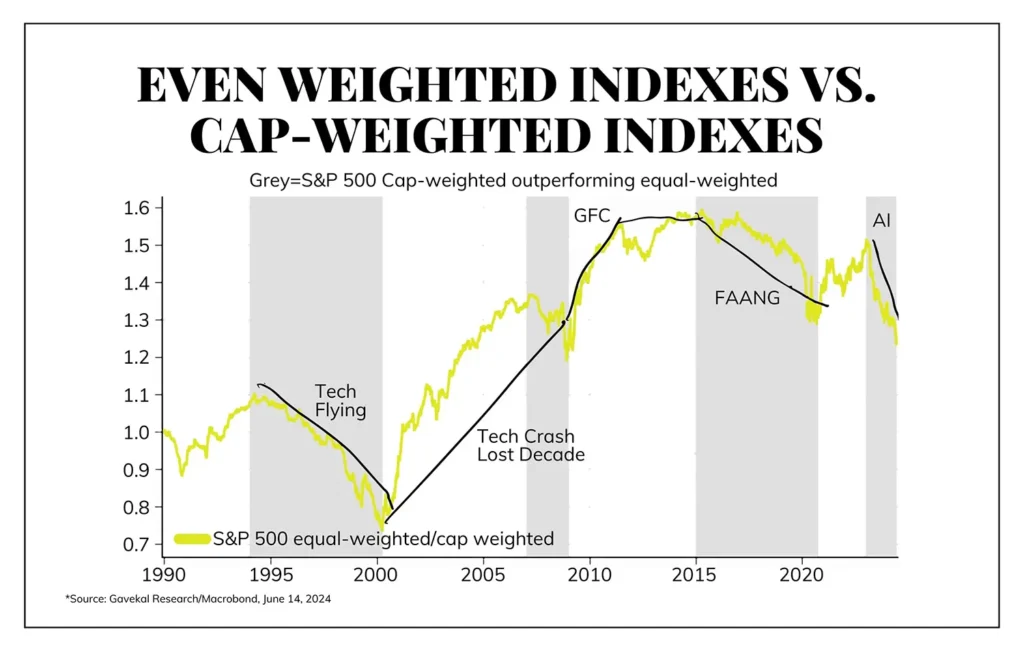

Chart of the Week

It may seem like how “even weighted” indexes do compared to “cap-weighted” is just some wonky term that nerds like me think about, and usually, accusations of me being a nerd are pretty spot on. But this is a big deal. We are not talking about the granularities of how market indexes are, or should be, constructed. Essentially, modern history is very clear – when “cap-weighted” indexes (the kind almost everyone owns) are killing equal-weighted indexes – it is a time that bubbles are forming at the top of the market. It can last for years. But it always ends the same.

(Don’t be confused by the chart – the yellow line is the EQUAL WEIGHTED then DIVIDED by the CAP WEIGHTED)

Quote of the Week

“Part of probability is that the improbable can occur.”

~ Aristotle

* * *

As we head into this Father’s Day weekend I am thinking about my late father, and I am sure many of you are thinking about your dads (whether they are still with us or not). It is a blessing to have the memories we have, and I know for me, a blessing to have his legacy still driving me, daily. Happy Father’s Day to all of you dads and all of you celebrating your dads. Summer is officially here.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet