Dear Valued Clients and Friends,

I love writing a Dividend Cafe when I can write the two different responses I am going to get in advance. In other words, I can save a bunch of people the time of writing their hate mail because I have provided the two different versions for you in today’s Dividend Cafe, so you can just cut and paste which one of the two fits and send to me as is, allowing me to read my own email. I say this sarcastically because I don’t actually love the contradictory bipolarity of our day, but it has become increasingly predictable.

What I do love is using the Dividend Cafe to tell the truth, and I believe the new One Big Beautiful Bill Act – OBBBA (I assume you all know they seriously named it this) requires commentary and analysis rooted in truth. As is often the case, the truth is not something tied to a team. The bill has some big problems and the bill does some good things, and both things are true at once, and this is true for investors and market actors (objectively), and I would suggest it is equally true in the body politic (subjectively).

But the Dividend Cafe is here to focus on the former – the objective things that matter out of this “big” legislation as it pertains to the economy and markets.

But I wasn’t kidding … I have provided two versions of a letter to send me at the end of today’s Dividend Cafe. Many of you would be shocked how literal I am being at the two polar opposite communications I receive from Dividend Cafe readers every day. And for those of you not playing team ball who have comments or questions outside the provided script, those are certainly welcome, too. =)

So let’s jump into one big, beautiful Dividend Cafe …

|

Subscribe on |

The Bill’s Major Components

Before I get into some market implications and economic commentary, let’s start with a high-level summary of what the bill does, broken out into four major categories:

(1) Extension of prior tax cuts

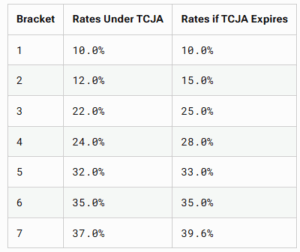

The reason this bill always had an embedded advantage in passing was that it extended the tax cuts of the 2017 Tax Cuts and Jobs Act that were set to sunset at the end of this year. Below, I provide a chart of what the rates have been since 2018 and what they would have gone up to without extension. But other sunsetting provisions that were also extended include a doubled level of standard deduction, a doubled level of child tax credit, a higher income qualification for the child tax credit, and other changes in deductions (SALT, mortgage, etc.). Had there been no action taken, 62% of taxpayers would have seen tax increases in the next tax year.

(2) Campaign tax cut changes

President Trump campaigned on “no tax on tips,” “no tax on overtime,” and “no tax on social security.” He added to his agenda after the election a desire to make auto loan interest deductible. These promises were addressed in the OBBBA via deductions up to a cap on income received via tips and overtime (more details below). The “no tax on social security” was never going to happen, but what the bill did as a substitute way to check that box was give an additional $6,000 standard deduction to those over the age of 65 with a phase-out for high earners (social security remains taxable).

(3) Pro-growth business tax changes

- 100% expensing of capital equipment purchases (and makes this bonus depreciation permanent)

- 100% expensing of R&D costs

- Enhanced deduction of corporate interest expense

- 100% expensing of factory construction

I believe this represents $100 billion of benefit to corporate America in 2025 and another $130 billion in 2026.

(4) Spending cuts (reduction of planned spending increases)

- Medicaid (delayed until 2028)

- Student loan

- Renewable energy changes

These “reductions of planned increases” ought to equal $1.5 trillion over ten years, or $150 billion per year (out of roughly $6.8 trillion of annual spending)

(5) An increase of the debt ceiling by $5 trillion

Congress is tired of fighting over the debt ceiling every year. The White House is tired of it. And because no one in the fight over debt ceiling has any interest in lowering the actual debt, removing (or at least giving more bandwidth) around the charade was tactically important. Mission accomplished.

Debunking the Myths

Myth #1: This bill primarily extends tax cuts for the wealthy

The top marginal income tax rate was 39.6% pre-2018, and it would have become the top rate again had Congress not acted. However, there also was an unlimited state and local tax deduction used mainly at the highest tax bracket (and even more so where someone owned expensive homes), and that tax break would have come back had everything from the 2017 TCJA bill sunset. The fact of the matter is that my taxes went up dramatically because of the 2017 tax bill, and would have gone much lower had the tax cuts not been extended. The problem is that there is so much nuance around all of this (the benefit of lower marginal rates against the loss of major deductions that vary in benefit based on one’s state tax burden and property situation) that it doesn’t make for a great narrative. Class warfare is always a good and simple narrative, even when it is a bald-faced lie.

Here are the tax rates we would have had (far right) had the bill not passed, and here are the rates in the middle column that will now be extended. As you can see, as a percentage savings, the largest benefits are in the second, third, and fourth lowest income brackets.

*Yahoo Finance April 9, 2024

Additionally, the standard deduction increase was and remains a major tax benefit for middle-class and lower-income individuals. The standard deduction had been increased from $8,350 to $15,000 for single filers, and from $16,700 to $30,850 for joint filers. But the OBBBA also added a temporary increase from those enhanced levels ($1,000 extra for single filers and $2,000 for married). The lion’s share of “wealthy” tax filers itemize their deductions. This standard deduction increase is targeted at taxpayers with less than $100,000 of taxable income.

Myth #2: CBO’s projections about growth are way off and this bill will not grow debt by $3 trillion – in fact, the growth will cause it to reduce debt levels!

Sorry, but that is just not true (as much as I wish it were). Those arguing this point (including NEC Director, Kevin Hassett) are appealing to past projections for growth from the CBO that have proven to understate the case for GDP growth impact from tax cuts (2017, 2004, etc.). I agree that the CBO errs on the side of caution when it comes to growth impact, largely because such things are very hard to score (especially over a long period, like, you know, ten years!). But first of all, scoring “new, additive growth” with extensions of tax cuts that already existed for years and years is very, very different than “actual, new tax cuts.” One of these things is not like the other. But additionally, the CBO also underscores the spending impact, too. In no period that we are assessing past scoring did they properly forecast spending levels (and I assure you that was not because spending came in lighter than projected).

Those who are claiming the debt impact will be less than projected are going to be proven wrong here. Now, other things may change. All we can comment on now are the facts of this bill and current known variables; if something else changes (for better or for worse), so be it. But those saying the debt impact here will be negligible because the CBO is always wrong are, well, wrong.

Myth #3: The OBBBA takes a chainsaw to health care spending in our country

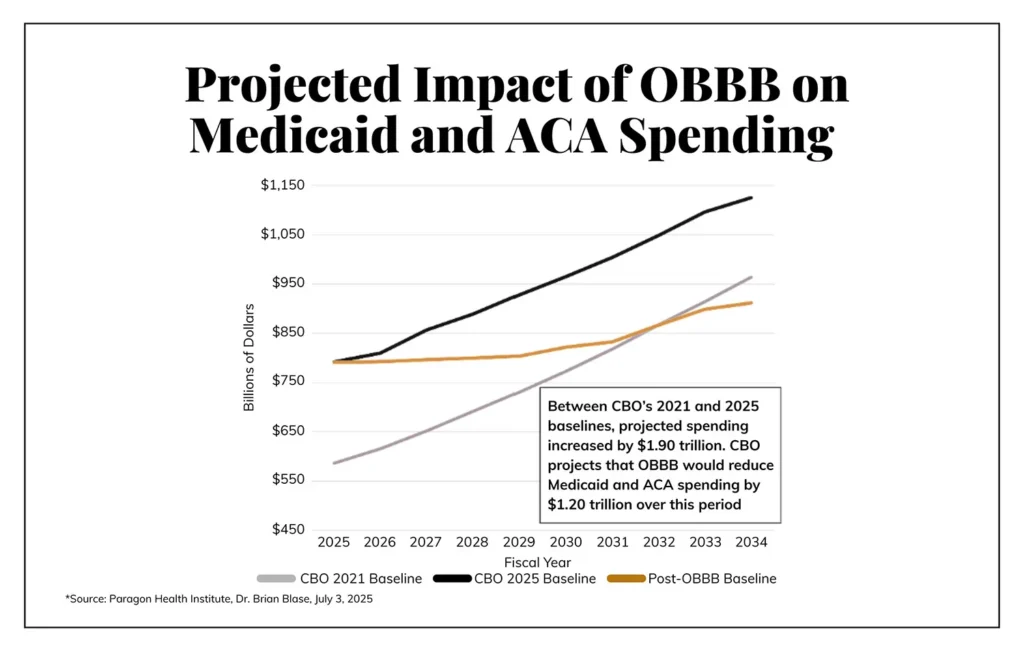

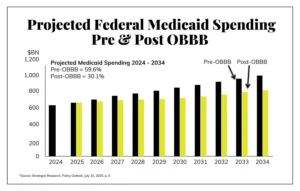

There are reductions to federal Medicaid spending in the bill that are intended to provide the numerical basis for other things done in the OBBBA. However, the more nuanced truth of what the Medicaid provisions are tell a different story than is being told in media narratives. Regardless of whether one believes this should be the policy objective or not, the primary focus is on removing ineligible enrollees from Medicaid, adding modest work requirements, and removing those whose eligibility was intended to be a temporary COVID-era subsidy. There is considerable room for disagreement about what we want our national Medicaid policy to be (i.e., federal support), but much of the current commentary is marred by poor distinctions between removing ineligible enrollees and actual cuts to coverage. Again, without expression of what policy ought to be, what the OBBBA does with Medicaid is primarily to restrain the growth of spending each year, restrict eligibility of non-citizens, move funding responsibility to states (as was originally intended), and limits the use of “provider taxes” and other workarounds.

The growth of federal spending on ACA and Medicaid is being severely curtailed, back in line with initial 2021 budget estimates, but the dollars being spent are growing, not shrinking.

To Growth or not to Growth, That is the Question

I promised objective analysis in the Dividend Cafe, but if we are being honest, the line between objective and subjective when it comes to opinions about tax policy is sometimes not super bright. So I will share what I subjectively consider to be objectively true … =)

- Objectively, “no tax on tips,” and “no tax on overtime,” and “auto loan interest deductions” are not pro-growth. They may benefit those who receive the deductions, but they are not incentive-producing or marginally broad-based benefits to the supply side of the economy. They just aren’t.

- Subjectively, all three of those policies are terrible. Yes, the President campaigned on them, and yes, as I have said repeatedly, the “no tax on tips” one had to be done from a political standpoint (Nevada is watching). But they are not the types of tax cuts that conservatives have historically supported (they do not produce supply-side benefits); they present an advantage to one worker that another worker does not receive for no good reason whatsoever.

The “no tax on tips” provision was implemented as a deduction of up to $25,000, but it only applies from 2025 to 2028. The “no tax on overtime” was implemented as a deduction of up to $12,500, also only for the years 2025-2028.

There are legitimate arguments to be made for lower taxes for many, and I am generally a low tax, limited government kind of guy. But creating special tax loopholes that benefit bartenders but not truck drivers is unfair to truck drivers. Having a lower effective tax rate for one person with the same income as another because of the way one’s pay is calculated is discriminatory. I believe the net result will be people angling to arbitrage (and game) the tax code with reclassification around tips and overtime, and I believe there will be entire sectors of workers who are totally left out, while a small segment receives all the benefits. I opposed student loan forgiveness for the same reason: it has a certain stench of buying votes, or attempting to do so. It certainly is not pro-growth.

In the auto loan case, it encourages the use of debt to buy a depreciating asset (is more consumer debt the need of the hour all of a sudden???), it discriminates against those who save to buy a car versus borrow to buy, it distorts the market as the tax benefit ends up getting priced into the cost of the car, as many on the right insisted would happen when Vice President Harris campaigned on a government subsidy for first-time homebuyers), and it puts the government inside a transaction it has no business being in (how individual consumers finance their automobile purchases).

My lack of enthusiasm for these personal tax changes (tips, overtime, auto) is simply a comment on the lack of supply-side growth benefits, which I favor in driving tax policy. These are not especially expensive tax cuts (but they are not free), so my critique is less fiscal and more growth-oriented. That said, there are pro-growth elements in the tax bill that I believe are underrated.

- The 20% small business tax break is now permanent. When the corporate rate was reduced from 35% to 21% in 2017 there was a realization that LLC’s and sub-chapter S corporations and partnerships would not receive the same benefit, so a 20% reduction of pass-through income was passed (though subject to income thresholds and not made available for every type of business). This break was going to go away even though the reduced corporate rate was staying the same. The OBBBA makes permanent this “equalization” move for small businesses.

- The Section 179 deduction for full deduction of equipment and capital investment is pro-growth and significantly supply-side.

- Likewise, so is the bonus depreciation deduction for production property (new factory construction, etc.).

- A permanent deduction for Research & Development is pro-growth and significantly supply-side.

I suppose a simple way to summarize the growth components is that the individual tax rate extensions are a “status quo” – the new selective “campaign” tax cuts are not pro-growth, whereas the new business deductions are pro-growth.

What I Hate the Most

What I hate most about the bill is not what it does, but what it does not do, which is address the trajectory of national debt. A bill that sets out to add $3 trillion to the national debt is almost certainly going to add more than that, and the need of the hour is to reduce the national debt, and at the very least, not add to it. I have written about the fantasy-land world of things I wish would be done, and I have written about where this is all headed. I certainly understand the political realities at play. I have not lost my Madisonian sensibilities. Legislating is hard in divided government. But if, if, if the intention was going to be “one big” bill, then I would have far preferred much clearer commitments to spending constraints that undid more of the excess we have seen since 2020. That effort was more or less taken off the table from the beginning. Federal spending has been running 23.7% of GDP since the pandemic; it has historically been 18-20%. This is the issue I wish the bill were addressing.

I am not a believer in the SALT deduction despite the fact that losing it cost me a fortune in taxes. I simply don’t believe that two people making the exact same income, who live in different states, should pay drastically different federal taxes. What the OBBBA managed to do was add to the inefficiency and inequity of a SALT deduction, but not let those who would most benefit from it, actually benefit from it (it phases out after $500k of income). The bill was not going to pass without some concession on SALT deduction due to holdouts in the GOP from California and New York, but this is my section of what I hate, and this part of the bill was horribly managed.

But at the end of the day, I just do not believe the bill took advantage of a needed opportunity to address spending and debt, and I consider that the greatest macroeconomic issue facing us today. Some may say, “Well, we can address that later,” but I ask you: if a Republican President, a Republican majority Senate, and a Republican majority House were not willing to address it, does anyone really believe that addressing it will get easier in the future?

What I Like the Most

The bill avoids a sure recession from a $2 trillion tax increase. This doesn’t do anything new, but it avoids what would have been a huge problem. But “status quo” is hard to get excited about.

What I like most in the bill, besides the avoidance of a recessionary tax increase, are the pro-growth elements of the business tax changes that I highlighted above.

A Few Things to Add …

Remember when “carried interest” was the most dangerous inequity in the tax code? Like President Biden’s bill in 2022 and President Trump’s bill in 2017 and President Obama’s bill in 2013, “carried interest” remains same as it ever was.

It is true (much to Elon Musk’s apparent chagrin) that many EV tax credits are being rolled back.

There are limits on the amount of federal student debt that graduate students can take (including medical and law school students). There are also efforts to change repayment options for new borrowers, to allow less forbearance and delinquency.

The estate tax exemptions are permanently set at $15 million (single) and $30 million (married), and then indexed for inflation from there.

Cut and Paste as You Wish

“Dear David – Why do you criticize President Trump so much? Don’t you see that he puts America first and therefore should not be criticized? You just seem like a Trump hater, always looking to go after him instead of supporting his agenda.”

AND

“Dear David – Why do you carry water for President Trump so much? Don’t you see that he is going to destroy America and therefore should never be supported? You just seem like a Trump MAGA guy always supporting his dangerous agenda.”

Or, you could re-read today’s Dividend Cafe??

Conclusion

I still see a budget deficit that is 5-7% of GDP for years to come. That number has to, has to, get down to 3% of GDP. The OBBBA does not do it. That does not mean there are not good things in the bill – there are. And the good things do not mean there are no bad things in the bill – there are. But “one big bill” is not going to solve the “one big debt mess” we have.

That remains a challenge for another day.

Chart of the Week

Yes, the new bill reduces the rate of growth of Medicaid spending. No, the new bill does not reduce Medicaid spending.

Quote of the Week

“Conservatism, rightly understood, is less a commitment to the past, than a commitment to certain truths, applicable to past, present, and future.”

~ Charles Kesler

* * *

There are a lot more details and nuances in the tax side of the bill that my Planning Department and Tax Department are working to summarize – details and nuances that didn’t belong in the Dividend Cafe. We expect to have that piece done in a few days.

In the meantime, all fun and games aside, regarding pre-scripted hate mail, I welcome all your comments and questions, all of the time. And I will remind investors that history is not ambiguous or unclear about this final point: connecting your market view to your political mood or interpretation of legislation has been the most predictably bipartisan foolish thing one can do, for decades.

Avoiding such folly, well, to that end we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet