Dear Valued Clients and Friends,

And just like that, it is 2020 … I do trust you and yours had a wonderful holiday season, a very Merry Christmas, and the happiest of new years. The most important thing I can do to welcome you to 2020 is direct you to our annual white paper here Year Ahead/Year Behind, providing our comprehensive review of 2019 and our forecast/perspective for 2020. We think it is readable, actionable, and digestible, and encourage you to pour into it today!

But we also have a full Dividend Cafe to bring you today. The news cycle did not slow down for the new year, and indeed, we have already opened the year with a slew of geopolitical events that add drama to capital markets. In this first edition of 2020, we obviously have to unpack all that is going on in Iran and the Middle East, but there is plenty more to look at as well – from China, to inflation, to investor sentiment, to politics, to the major risks of 2020.

So welcome to 2020, and welcome to the new and improved Dividend Cafe. Our resolution is to make it interesting for you. To that end we work.

Dividend Cafe – Podcast

Dividend Cafe – Video

One and done or something more?

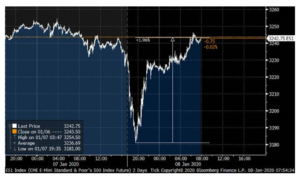

Here is what we know thus far – the market opened the year up a couple of hundred points, then dropped a couple of hundred points upon hearing of the United States take out of Iranian Quds Force Commander, Qassem Soleimani. Markets then went up a few points, then down a few points. And then on Tuesday night, Iran launched a dozen missiles at U.S. spots, none of them appeared to do any damage, and the stock market futures went from down 400 points to up 50 points overnight. We ended up 200 points on Wednesday, and as of press time Thursday we are up another 225 points. So while this has been the media story of the week, it has actually barely registered as a stock market story (so far). And in fact, the market has proven resilient and even excited through it all.

The futures said what?

Some advice: Overnight futures, and especially media coverage of overnight futures, are often not very useful predictive or informative tools.

Not so fast …

But bond yields did drop a bit (from 1.9% to 1.8% in the 10-year treasury), and oil prices were up a bit (+4% or so – nothing too dramatic). Gold moved higher. There were movements in asset prices, but they just weren’t very dramatic and certainly not unexpected. The question, of course, is what happens next. Does some escalating retaliation take place, or does this fizzle out a but from here. Markets are afraid of overreacting, and yet there is also the possibility that things worsen …

The reality is that there is no particular course of action investors ought to take in the midst of geopolitical uncertainty. This is why investors asset-allocate! And it bears repeating: Geopolitical risk is a permanent reality, not a shocking transitory thing that entered the fray last week.

We are permanently aware of the risk of geopolitics jolting markets, and we are permanently prepared via well-constructed asset allocations that honor an investor’s comfort level with various fluctuation possibilities. Period.

Half-full glass

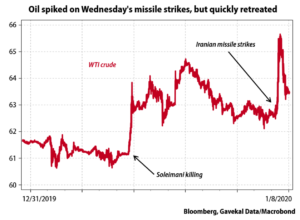

First, the potentially positive outcome … The Iranian missile attack appears to be more for the headline and local propaganda, and less intended to escalate actual tensions. Oil prices certainly seemed to think so, actually declining the day after the missile launch. Iran’s line that they would “meet further U.S. aggressions with more painful and crushing responses” seemed to almost be a way of saying, “okay, if you stop, we’ll stop,” knowing full well that a casualty-free attack was not likely to provoke any “aggression” from the U.S. at all. In this scenario, Iran backs down from the takeout of the evil Soleimani, and both countries have an off-ramp for de-escalation.

Half-empty glass

Of course, the most optimistic scenario does not always play out, and it makes perfect sense to assess what potential outcomes are out there. It is entirely possible that this whiff of a response from Iran is just act one, and that future actions escalate into a severe level of hostility. Iran knows of their disadvantage militarily, and the U.S. knows of the unpopularity of escalation politically, so the half-empty glass scenario of a prolonged military disruption leading to market anxiety is not the most likely scenario in our estimation, but the geopolitical risk is called risk for a reason.

China and Iran are connected how?

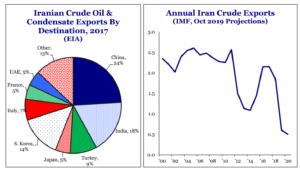

Energy purchases are a huge part of the trade discussions between the U.S. and China (that is, China agreeing to buy natural gas and potentially crude oil from American producers). China is presently Iran’s biggest customer of oil exports. Iran’s capacity for production is getting decimated. I will leave it there.

* Strategas Research, Policy Outlook, Jan. 3, 2020, p. 2

Some Economics to Start the New Year?

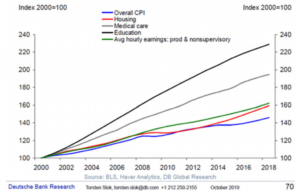

Money managers and economists all feel a compelling need to guess when the Fed may tighten monetary policy. The Fed has used as their reason for a decade now the persistence of low inflation as a justification for running hyper-accommodative monetary policy. Indeed, deflationary pressures in the economy that I have written about ad nauseum have contained the price level, other than in government-subsidized areas (i.e. college tuition, health care, and housing).

Subsidies serve as a turbo boost to prices, and this is a fact of life. Energy prices and Technology prices held inflation down over the last ten years, so the decade is a confused tale in terms of evaluating inflation.

But there is another area that low-interest rates have been effective in boosting prices higher – and that is asset prices (i.e. financial assets that are priced against a “discount rate” or a “risk-free rate”). By definition, assets get more expensive when what they are priced against gets cheaper.

The Fed believes inflation is low, and by their evaluation measures, it is. They do not worry about asset price inflation (their views on the “wealth effect” would suggest the like it). And here is why I would say with high conviction that the Fed is positioned for an extended period of “no activity” and “loose positioning” – they are re-defining how they measure inflation to give them more leeway, not less. The idea that they are “targeting 2% inflation” is extraordinary to me. But the idea that they now believe “targeting a long-term average of 2%” (so it can run above 2% in some years to make up for the years it allegedly ran below 2%) is really audacious.

And that is the world we are now in. So, no. I don’t expect rate tightening any time soon.

Our Investment Committee Discusses

the Year Behind and the Year Ahead

Midstream check-in

The troubled oil and gas pipeline space went up ~15% in the first half of the year, then gave all that back and then some in the next five months. But the space closed December with four straight positive weeks, making back ~12%, ending the year with a 6-7% total return. The announcements from key companies in Q1 about their expansion project planning, their financing, their financial metrics, and their corporate governance, will all be potential catalysts for the space in the early part of the year.

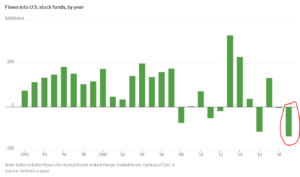

Contrarian sign of the week

It what can only be called a screaming contrarian signal, in addition to a rationalization for my entire industry, $135.5 billion was pulled out of equity mutual funds and ETF’s last year … This represented the fastest pace of withdrawal ever, and yet those investors missed out on the best market year in six years and one of the best in thirty years. Investors are not only “not chasing” hot returns; they remain in disbelief at this bull market, and tragically, many have missed out entirely. There was plenty of vulnerability in the market last year (mostly trade-related, but also around the “inverted yield curve” talk of late summer). Investors who hit the panic button are the contrarian indicator of the week around the sustainability of this bull market (they die on euphoria) …

Top Five Risks for 2020

These are not predictions, but rather risk-possibilities that I measure as having higher odds than other risks. I do not predict that any of these will play out, yet I believe all of them need to be watched, monitored, and respected.

(1) Trade war flip-flopping (also covered in our white paper)

(2) U.S. election outcomes (some are worse than others)

(3) European contagion (keep this on your list for future years, too)

(4) Escalated Middle East tensions (this is cheating, because it’s always true)

(5) Cyclical inflation spurts

A stat that floored me this week

The Philadelphia Gold and Silver Miners Index index (XAU) is currently at the same level it was in 1984 – yes, 1984, when Mary Lou Retton was winning Olympic gold medals! 36 years of no gains in the gold/silver mining index. It’s stunning.

Politics & Money: Beltway Bulls and Bears

- Obviously the largest “political” story of the week was foreign policy related to the Iranian scuffle, and I have covered that up top more extensively. But I will say that one of the most important themes we hold for 2020 is the role politics will play in markets. The uncertainty around things is likely to become a factor in boosting volatility later in the year. And the tension between the unpredictability of this political season and the seemingly impenetrable correlation between economic good fortunes and incumbent re-electability is going to be fascinating. Should economic data hold up as it is now, by the end of the year a lot of people are either going to be saying, “it was so obvious he would be re-elected,” or “he lost because temperament and fatigue trumped the economy.” I will not predict which way that breaks (yet).

- We don’t believe the impeachment saga is even a story in the grand scheme of markets (hasn’t been, isn’t, and won’t be). What we do believe is a political story the market cares about is the trade war, economic drivers towards capex, and the 2020 election and issues driven by executive orders. We have four Senate races we are watching closely, a Democratic Primary to watch (which may go on for a while), and then, of course, a general election. Buckle up …

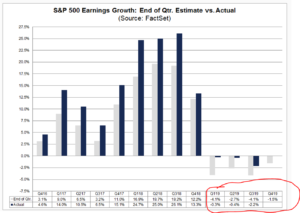

Chart of the Week

An under-rated story in 2019 was how the quarterly earnings growth results, while never stellar, consistently outperformed the pessimistic projections analysts had for them. Note the red circle at the bottom to see why we are optimistic that even fourth-quarter earnings results will come in better than expected …

Quote of the Week

“The only easy day was yesterday”

~ Navy Seals

* * *

I cannot tell you how excited I am for the new year, and just how happy I am to be in 2020. We are making a concerted effort to create as much high quality, informative, actionable content as possible this year. There will be no shortage of inspiration.

We welcome all clients reaching out with questions about our portfolio positioning as we dive into the new year. We are anticipating a book-wide re-balance across all client accounts next week, yet most top-down allocations are not being altered more than just marginally. It is a good environment for investors. It is a good time to be cautious. Both things are often true at once. Both things are always true at once.

Financial Planning, Tax Preparation, Estate Planning, Cyber-security, Property & Casualty Insurance, our Client Portal – these seven key themes: Talk to your Private Wealth Advisor about each subject.

And yes, we’ll keep talking to you about dividend growth. To that end, we work …

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Café features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet