Dear Valued Clients and Friends,

It is not accidental that I write so much about the Energy sector. First and most applicable, we are big energy investors at The Bahnsen Group, carrying an allocation in our Core Dividend portfolio that is triple the weight that the S&P 500 has. What is happening in energy markets has profound relevance for the economy at large, for all people in their everyday lives, and across all national borders. Few things are more globally relevant than access to energy.

But if I am being totally honest, even apart from the large financial exposure we have to the energy space, I love this subject because energy fascinates me. It should fascinate anyone who spends just sixty seconds thinking about the fact that natural resources around for thousands of years with almost no known utility have created a more significant increase in the quality of life for more people than anything under the sun. “Transformed energy” sits at the heart of all economic activity, as my friend Louis Gave is fond of saying.

You cannot destroy energy, which is both a law of the universe most of us learned in elementary school and, these days, apparently a vital message for investors. In the physical universe, it merely means energy is constantly changing – usually for the purpose of doing work – but in the investing world, I believe it means something different but perhaps not entirely disconnected.

So let’s do a little autumn analysis of the energy sector, where we are, where we may be going, and see what may edify us in the discussion. Let’s jump into the Dividend Cafe …

|

Subscribe on |

A quick market point

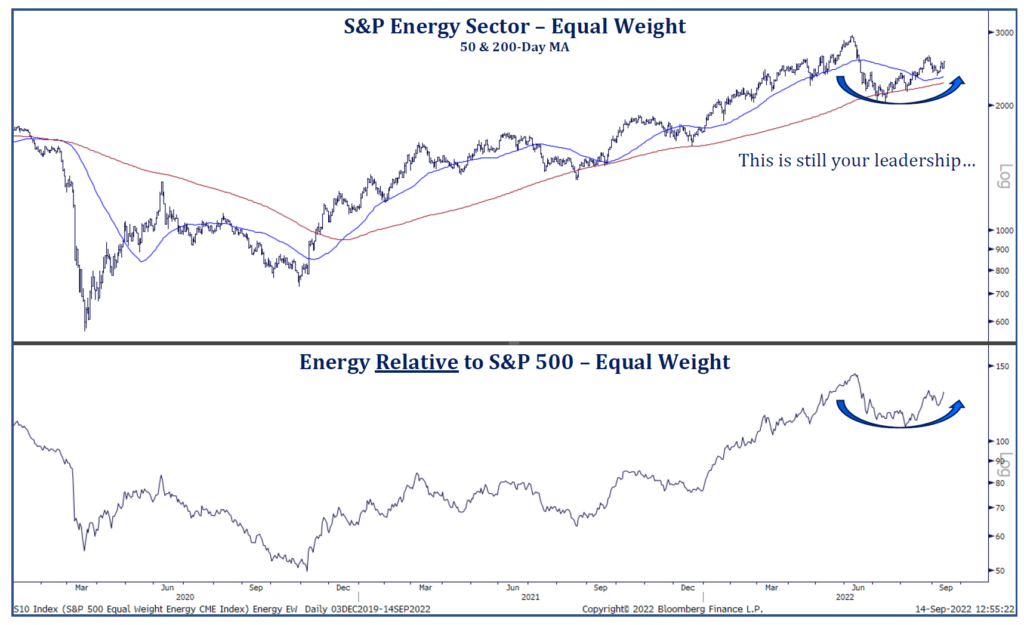

I think most readers know that Energy has been the biggest bright spot in what has been a difficult year in the market. Not only on an absolute basis have returns been stellar across the broad energy sector (top), but relative to the market, it has had nearly uninterrupted superiority to the rest of the market since November 2020 (bottom).

*Strategas Research, Technical Strategy Report, Sept. 15, 2022, p. 3

But these strong absolute and relative returns are mysteriously (and for this contrarian, gloriously) accompanied by outflows, not inflows. The normal market behavior of investors pouring into a sector just as it is ready to hit its peak and begin a reversal is not in play. Regardless of whether they prove to be right or wrong, investors have had a hard time leaving the investment success stories of a couple of years ago and are having a hard time entering the investment success story of the last 18+ months.

Under the hood

Oil prices hit a high of $124 in March and re-hit $122 in June. Yet it now sits around $85. Oil came down ~20% after that March level, and many energy stocks came down with it. It has steadily come down in the last three months, yet the energy sector has performed quite well. Why, you ask, may that be?

What goes down must go up, when the government guarantees it

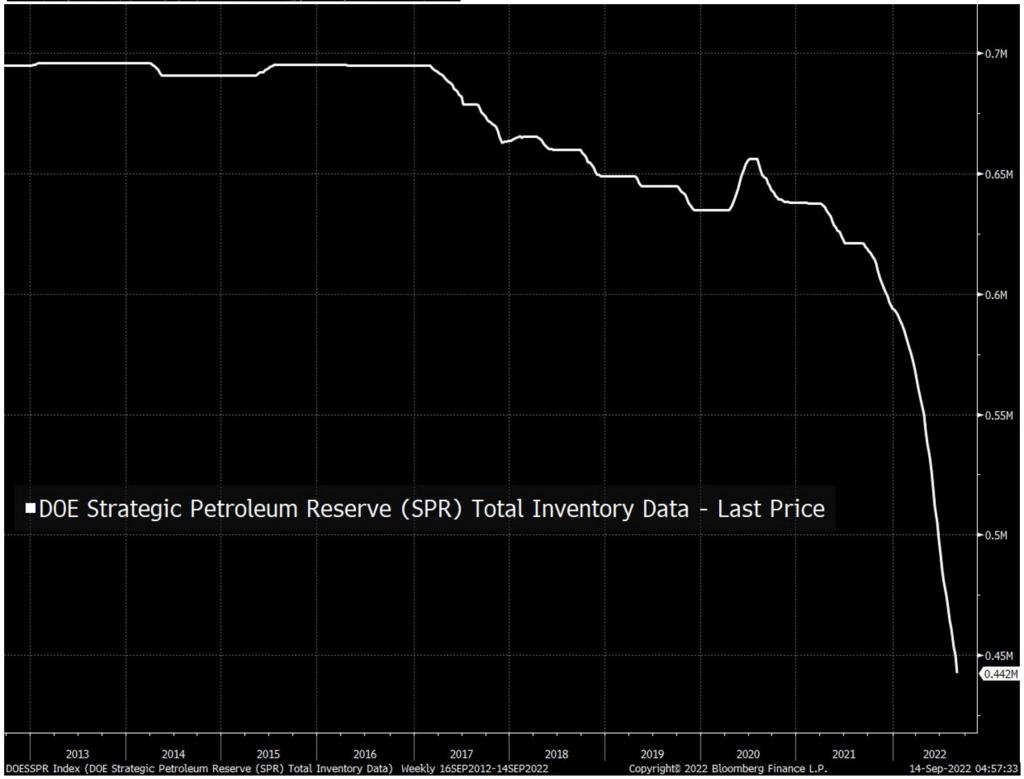

Note the drawdown of Strategic Petroleum Reserves over the last six months. Production has been wholly inadequate to meet demand, forcing upward pressure on prices, so this drawdown of emergency reserves has been used to meet that delta as much as possible, creating a floor in crude oil prices as of late.

*Bloomberg, Sept. 14, 2022

But, the government has not merely drawn down Strategic Petroleum Reserves – it has also promised to refill these reserves, making commitments to domestic producers for future purchases. The market knows this. The details are not all known (volumes, timeline, etc.), but the basic commitment is, and that causes two things to be true at once:

(1) Supply is higher now than it otherwise would be, lowering prices on the margins

(2) Demand will be maintained into the future from government commitments, keeping energy producers well-bid despite the SPR drawdowns

Reserve levels are essentially at early-1980’s levels, down 40% in just a short period of time, and while no one knows when most market actors know that inventories will have to be re-filled.

Profits and Price

I am about to start making the case for an energy exposure not super-tethered to the price of oil in its investment appeal. But before I do, I will say that there are reasons to believe crude oil could be right back up near recent highs. I hope that does not happen. Our investment thesis does not need it to happen. Oil producers are making substantial money at much lower prices. If it does happen, it represents many other negative things for the U.S. economy. It surely erodes demand at some level. But there are ample global circumstances that could cause it to happen.

First of all, Goldman Sachs is predicting it as a baseline expectation ($130/oil, to be exact). Now, I have commented before that their predictions have not always been stellar when it comes to oil prices (very few can say differently), but there are fundamental factors driving this forecast. Russia. Europe. U.S.-ESG. SPR refill. It is not out of the question.

Door #1, 2, or 3

And this is where I think there is some asymmetry that needs to be understood. Stay in the $80-90 range, and oil producers are making great money with ample demand. See, geopolitical factors push oil back to $120, and while demand slows, margins expand even more. Those are fine options for the producers.

What hurts the producers in the near to medium term? Something that destroys demand (a deep recession), with supply picking up unexpectedly. Could the former happen? Yes, even if it is not the baseline case. But could the latter happen as well, in concert with the former? I think it is highly unlikely.

The risk-reward tradeoff is favorable.

But wait, there’s more

The supply-demand dynamics of oil are not the only relevant factor for energy sector investors, and they are not even the main factor for our exposure.

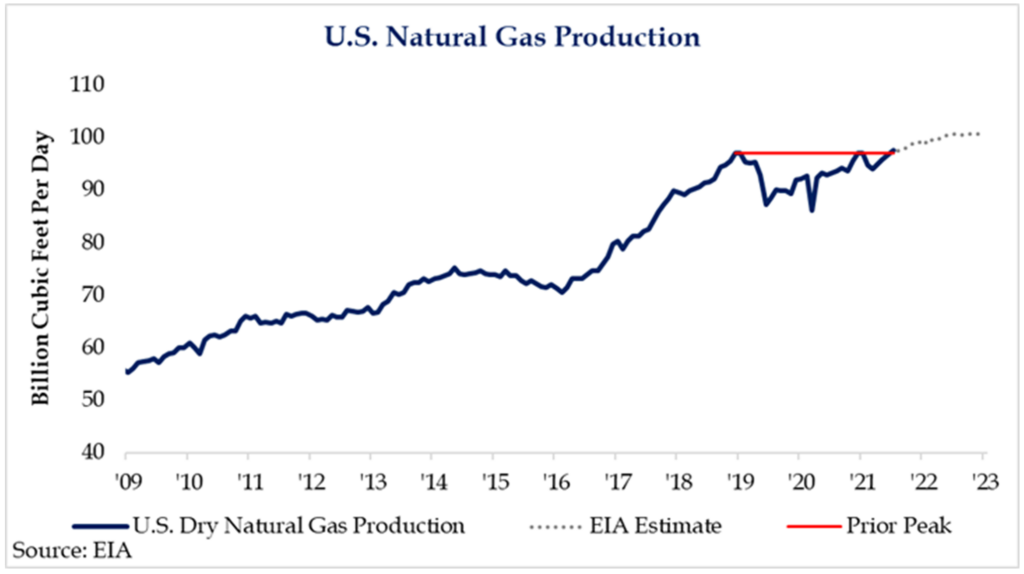

Crude oil remains one million barrels per day below its pre-pandemic production level in the United States. Natural gas, on the other hand, is now at an all-time high.

*Strategas Research, Daily Macro Brief, Sept. 15, 2022

And that explosive production to meet explosive demand in natty gas has not come at the sacrifice of margins. Prices have stayed high, and margins are significant. The dotted line above represents the EIA’s forecast for domestic production growth into next year.

I have a solution to your trade deficit worries

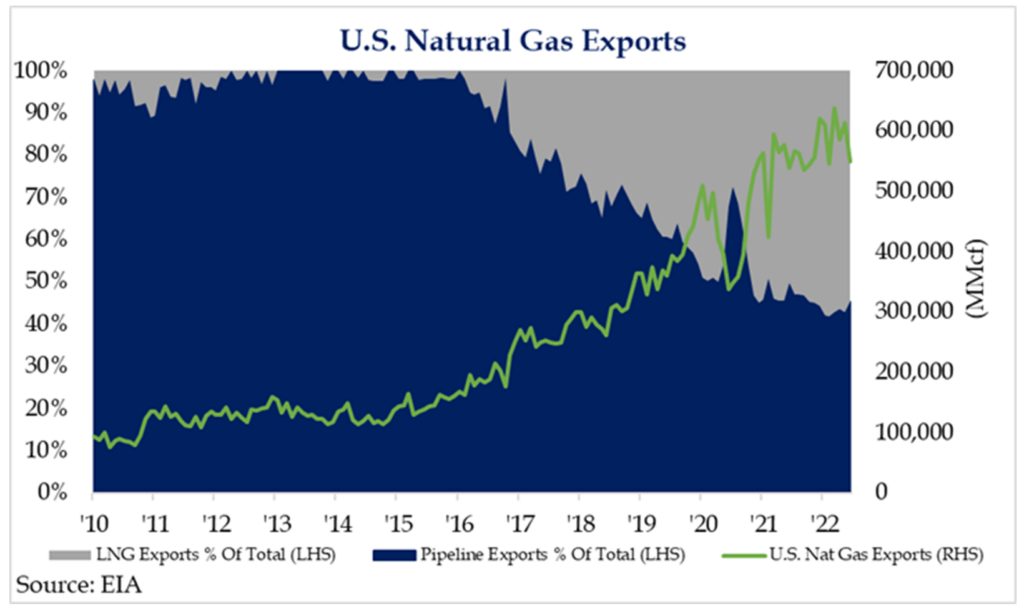

Exports of U.S. natural gas are up 600% in the last seven years. They didn’t move from 2010 to 2016 and then exploded higher. I will let you attach your own political explanation to such. Now, they continue to go higher as Europe desperately seeks a solution to its gas deficiency as Russia cuts off supply in the aftermath of its Ukraine invasion.

*Strategas Research, Daily Macro Brief, Sept. 15, 2022

So you have rising exports that in no possible way are anywhere near the level they need to be, with a greater portion of such natty gas exports coming in the form of liquefied natural gas. LNG can be exported to Europe or Asia, with terminal capacity for imports in short supply on their end and terminal capacity for exports in short supply on our end. Insatiable demand on the customer side and huge margins on the producer side, and you get … higher prices, margins, and profits.

Natural Gas Understood

View natty gas as a coal replacement if you want. Lump it in with fossil fuel considerations if you want (it certainly is a fossil fuel). But understand this, coal has gone from 50% to 20% of electricity generation in just 15 years, while natural gas has gone from 15% to 40% (the first place position by a wide margin relative to all other sources of electrical power). Fertilizers, cosmetics, plastics – and yes, electricity – we are talking about a wide array of the most basic elements of human living – all tied to natural gas.

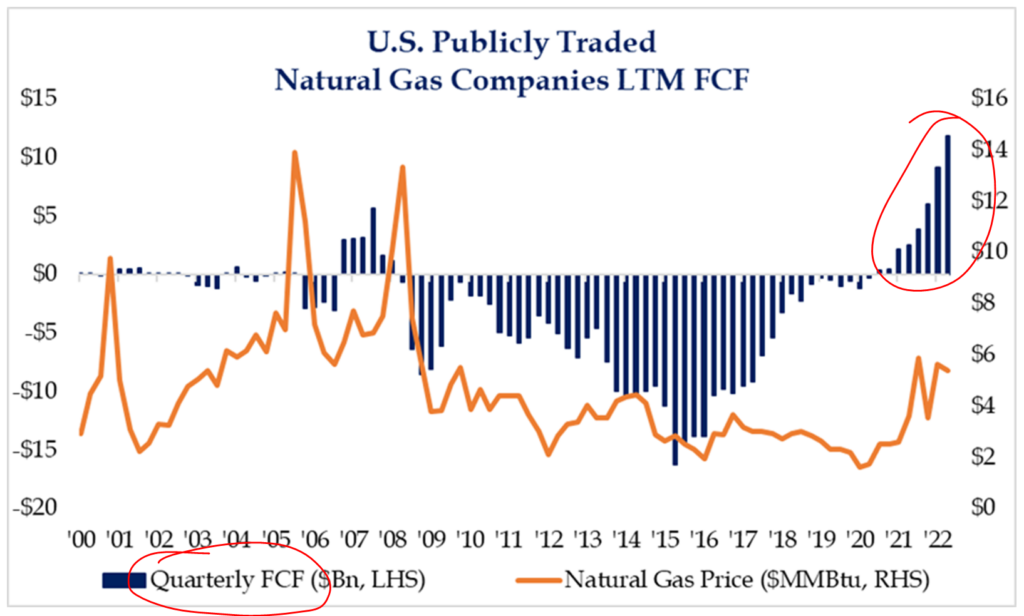

Million dollar picture

We don’t merely have an environment now where natural gas companies have growing production of a product in growing demand with growing utility and global need. We also have that now in a fiscal environment where capex is constrained, capital allocation is “disciplined,” and free cash flow is massively positive. This is a song from our hymnal.

Middle of the road

When supply is high, and demand is high, the volumes running through pipelines are high. This bodes well for midstream companies receiving tolls to transport gas from the wells to the storage or distribution facilities. It is a fee business, capex-intensive, but also in an era of strong free cash flow and greater fiscal discipline.

The midstream sector builds and operates the infrastructure necessary to transport oil and gas, to store it, to refine it, to gather and process it, and, yes, to export it. A diversified midstream exposure will have some commodity price exposure, but not much, and not as its primary source of revenue.

Is ESG the end of the fossil industry?

Fifteen years into the evolution of a movement to limit the fossil fuel role in society, the percentage of energy coming from fossil is not really down at all. The composition of which fossil fuels have changed, and the level of carbon emissions has [thankfully] come down, but the societal and human need is not changed much. The capacity for wind and solar to impact oil and gas demand is limited for a variety of reasons. The greatest threat has been external – social and political pressures to cut off funding.

Reports of an ESG-induced starvation of capital to the oil and gas industry have been greatly exaggerated. Do many in Congress yell at our big banks to stop funding our energy industry? You bet. And has stopped $1.1 trillion from coming into the energy sector from private equity over the last ten years? No. It. Has. Not. $1.1 trillion from private investors, disconnected from the direct pressure of social activists, proxy fights, and other ideological distractions.

American capital markets proved to be the great hedge against the ESG mistake. Perhaps the composition of capital sources has changed, but the need for capital fuel growth, new investment, capex, and innovation has been met.

The pursuit of rational capital allocation in a free enterprise system is tough to hold down. I say that with gratitude.

The European Emergency

If my thesis were based on a code red in Europe playing out, I would not be so sanguine. This is not because I believe Europe’s challenges are easily solvable. I think they face an electricity shortage. I think Russia is playing hardball. And I have no idea how it will play out. But investing to make money in a really bad situation often does not work out because, well, really bad situations often get fixed in a way that confounds the perma-pessimists of our day. I am arguing from a non-extreme basis – one that does not believe this all thing comes out roses but also assumes it does not reach the worst-case scenarios for our European brethren.

What I think sits right in the middle of the field is a scenario where more gas is needed in Europe from America, and we are ready to fill that role for years to come.

If it gets worse for Europe, it possibly gets better for the U.S. But no, I am not banking on that outcome.

Conclusion

I have no doubt there are things that could disrupt the various theses that form my energy sector worldview for years to come. What I must repeat as an investment professional is that our worldview is not centered around the next three weeks or three months. We have a multi-year view that is bullish on American energy at a time that the policy environment is unfriendly (maybe it gets better?), investor sentiment is not remotely frothy (maybe it gets better?), momentum and fundamentals are aligned, not at odds, and geopolitics offers asymmetrical pockets of opportunity.

Energy is always transforming. Right now, the market needs it.

Quote of the Week

“We take the materials around us and make them more valuable; that’s how we went from starving in a cave to producing a cornucopia of food that we can enjoy in comfortable homes. The thought leaders did not sufficiently consider these virtues of human beings.”

~ Alex Epstein

* * *

Enjoy your weekends thoroughly. Be grateful for energy. And be bullish on the forces of ingenuity that have transformed so much energy into so much opportunity. It is true in these aspects of our portfolios these last couple of years but even more true in our day-to-day lives.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet