Dear Valued Clients and Friends,

It is the topic of the moment – artificial intelligence. No topic has more captivated investors in almost 25 minutes 3-4 years than “AI” – artificial intelligence. It has resulted in one company becoming over 7% of the S&P 500, and created the most top-heavy S&P 500 in history. And it is more than an investment rage – it is cultural, political, ethical, and some may say, theological. And today, it is the subject of the Dividend Cafe! Let’s jump in …

|

Subscribe on |

We will never break the internet

The Dividend Cafe is not a place I want clients and readers to come for “trendy commentary.” As is the case in pop culture and the wider news cycle, financial and economic narratives are subject to groupthink, and many times, stories, narratives, and themes become over-exposed, un-nuanced, and just plain over-done. We are not surprised when this happens in colleges, entertainment, or social media. It can happen with William Shakespeare (see page 19). It can happen with the Kardashians (some might say one story was too much). And it can happen with financial or investment themes and topics.

Much of this phenomenon is commercially driven. In financial media, for example, only two things are actually monetizable – extreme fear, and extreme greed. The place where real life happens is too boring to generate the clicks and ratings that make much money. Dividend Cafe happens to not be a revenue center for us (if you don’t believe me, multiply the number of subscribers you think we have by the amount you paid for your subscription). Extreme fear is best monetized by a cottage industry of newsletter charlatans who have done one thing extremely well – know their customer! You may not ever meet someone who has done better in knowing their own audience than the doomsday newsletter cult of the last fifty years. Find people who want to hear the world is ending, and tell them they are right, over, and over, and over again – in different ways. It’s a work of art to observe the grift, but it is monetizable.

Extreme greed (i.e. hype) seems to be easier to monetize at more conventional or mainstream outlets (TV networks, newspapers, and widely-read websites). People buy dreams, and what could be a bigger dream than believing that one can be rich easily? And dare I say, what could draw more people in than the idea that one’s neighbor is getting rich [easily], and they are not! Envy is a more powerful vice than greed. Many people monetize this dynamic quite effectively. What happens when a big theme takes off is that the success feeds on itself in news coverage. A genuine story becomes a genuine overkill with genuine hype because human nature is at work, period.

You can read the history of Dividend Cafe on the right side of the home page in the yellow box but suffice it to say, playing into some extreme human emotion was never a strategy in the formation of this digital offering. If anything, I have developed a sort of aversion to the most popular or trendy stories of the day, not merely because of the contrarian nature of our investing philosophy but also because I find overkill of coverage obnoxious. If I wanted to talk about something over and over again, week by week, it would be dividend growth investing, Chinese food, USC football, or documentary streaming. Read that list again, and guess why I didn’t try to create a “trendy” website …

So, writing this week about “AI” investing is not me bringing the hype to the Dividend Cafe. It just is at a point where some serious “first principles” are needed when it comes to this topic. Artificial Intelligence is very much on our radar at TBG, and our refusal to discuss it 79 times per day doesn’t mean we don’t have strong opinions on it. Those opinions are the subject of today’s Dividend Cafe.

Not burying the lede

Let’s get the easiest part of this out of the way. “AI is big.” It is just as easy to add, “AI is going to be big.” The approach we take to AI is not skeptical of artificial intelligence, as if we were “AI deniers” (I am sure that term will find its way into the pejorative lexicon soon enough). I would like to start this Dividend Cafe with the conclusions up front, allowing those of you who want to skip out on the rest to do so (note: bad idea) …

- Tons of what we are talking about with AI is NOT new, but has been around for some time.

- Nearly all of the investment benefits of AI, thus far, have been limited to the “backbone” of AI, and not the use of it.

- Many of the backbone winners will prove to be losers.

- Many of the backbone winners that will stay winners are already priced for such, and then some.

- Predictions about how AI will change things, who will benefit from change, and how this will all play out, will be riddled with error.

- Greater Fool Theory applied to AI investing will make fools of those who employ it.

- Principles are what you apply in times of decision-making, not the things you end up with out of decisions.

- “This time is different” is what people always say before it ends up not being different

- The only thing that will prove more wrong than predictions about AI investing are predictions about AI’s impact on society

- AI CAN BE invested in within a dividend growth framework. In fact, it OUGHT to be invested in within such!

Now, the unpacking begins!

#1 – Tons of what we are talking about with AI is NOT new, but has been around for some time

With no intent to dilute the power of the technology or the future efficacy (see below), not all of what people are calling “artificial intelligence” is brand new. Most Generative AI is pretty new (and still in flux), whereas much of Predictive AI has been in development for quite some time. Nevertheless, the speed has all intensified, the objectives (especially with so-called “multimodality”) have expanded, and the promise of the technology has grown immensely.

#2 – Nearly all of the investment benefits of AI, thus far, have been limited to the “backbone” of AI, and not the use of it

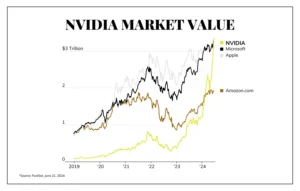

For all of the talk about language-learning and all of the public’s fascination with where AI may alter the investment landscape, almost all of the investment success for AI, so far, has been in so-called “backbone companies” – that is, not companies “using” or “doing” AI, but rather companies who create the infrastructure by which other companies will “do” AI. The obvious examples are chip companies thus far, with Nvidia being the extreme example. But adjacent to the chip companies whose “backbone” contribution to the AI story has been well-monetized are cloud companies who are key players in AI infrastructure. If AI were food, it is so far not restaurants making money for shareholders as much as it is oven manufacturers.

#3 – Many of the backbone winners will prove to be losers

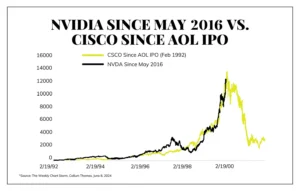

We saw a similar dynamic in the 1990’s with the internet. While some of the actual dot-com companies infamously went public to much hype and fanfare, the telecom and cable companies who were needed to “feed” the internet exploded in value. New phone and cable lines were needed, and hardware companies that would connect the internet to real life people and businesses went crazy, too. And yes, switches, networks, and routers were needed, as were fiberoptics, cable lines, and all sorts of “backbone.” The lessons of Lucent, Global Crossing, and Worldcom would suggest that sometimes “backbone beneficiaries” are not so easy to identify. And the lessons of Sun Microsystems and Juniper Networks would suggest that understanding what adjacent backbone is actually going to play out is not so easy, either.

Go back to 1999 and suggest to people, though, that it was too early to know if Global Crossing or Juniper would be the needed ingredients of the future. You were cast out as some sort of Luddite, a terrible investor like, you know, Warren Buffett. Ay yi yi. It feels like yesterday that everyone lost their mind.

#4 – Many of the backbone winners that will stay winners are already priced for such, and then some

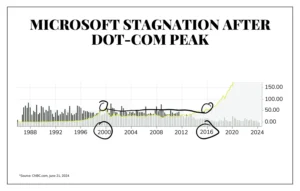

I can provide chart after chart after chart of the 1990’s winners who are still industry-leading technology success stories today. The Microsofts and Ciscos and Amazons of the world did not become the Sun Microsystems or Lucents. Their promise delivered. Their results came to fruition. They were just reflected in the price, and then some, many, many times over.

But for fifteen years plus change, it didn’t feel like these companies had lived up to the expectations. In the case of Cisco, for the person who bought in peak 1999 valuation, it still doesn’t. And despite Microsoft’s unbelievable performance over the last eight years, it went sixteen years before it re-found its price of 1999. What did it do as a business for those sixteen years? It led the world in business software, enterprise, operating systems, and pretty much all aspects of computer usage and application.

#5 – Predictions about how AI will change things, who will benefit from change, and how this will all play out, will be riddled with error

Some chip companies are going to beat other chip companies. Some chip companies are going to fail altogether. There may be a time when total chip sales simply underwhelm expectations. The “adjacent backbone” companies may be totally different than expected. In the 1990’s phone and cable-related companies were genuinely at the center of the Internet revolution. Wireless networks and fiber optics changed what we thought about cable and telephone, and the companies involved in those changing dynamics all changed, too. But an even better example is phone manufacturers … The promise of wireless coming to Nokia and Motorola created a little bubble of their own, and the competition from Blackberry created a little 99% deflation of that bubble. And then Blackberry met Apple. Should I mention Palm somewhere in there, too?

Now, was anyone wrong that phones would become a key part of the promise of wireless? Hardly. But that is small consolation to the shareholders of Ericsson. Did PC use change? Sure. Gateway saw billions of dollars of market cap evaporate before going away in 2007. But Hewlett-Packard is a $40 billion company, near an all-time high.

The predictions of sector winners and losers will be volatile, fallible, and humbling. The winners and losers within those fallible sub-bets will also shock many.

#6 – Greater Fool Theory applied to AI investing will make fools of those who employ it

Increasingly I am hearing more say that they are holding their [fill in the blank, but assume it is Nvidia] stock for now, letting it “ride a little further,” with plans to dump it on someone else at just the right time. In other words, more and more people are convinced valuations are unsustainable, but they have high confidence in their ability to find a sucker to replace them.

The year 2000 called and wants its investment strategy back.

#7 – Principles are what you apply in times of decision-making, not the things you end up with out of decisions

In other words, decisions follow principles; principles do not follow decisions. Circumstances do not form principles unless that is your principle (“My core principle is to change what I believe I do to what seems expedient, right, convenient, easy, or beneficial in a given circumstance”). Maybe that is the right principle? But if chasing fads, momentum, and catnip were a good principle it seems to me history would have been kinder to those who would have practiced it.

#8 – “This time is different” is what people always say before it ends up not being different

This barely needs elaboration. But it does because its permanent usefulness only works to specific illustrations of it in hindsight. At the moment, [fill in the blank] doesn’t apply to the “this time it’s different” lesson because, well, “this time may be different.” Until it gets revealed as not being different.

Let me be clear. Some companies end up being amazing. They grow into valuations. They dominate, execute, and transform. They succeed and reward. I am NOT talking about an inevitable failure of businesses; I am talking about the investment results of companies who price in decades of best-case outcomes in months. That lesson has no exception I am aware of.

#9 – The only thing that will prove more wrong than predictions about AI investing are predictions about AI’s impact on society

Through all of the talk about AI’s investment relevance, there is significant hand-wringing over what it will mean for the culture. Some are sure it will be dystopian and disastrous. Some worry it will concentrate power wrongly. Some worry bad ethical things will happen (that one seems safe as a prediction!). Some worry it will leave tens of million of people unemployable (that one is inane). As a Schumpterian to my core, I disagree with the doom and gloom economic forecasts around AI. As a student of history, I can’t believe this argument is being made again. But it is wrong.

AI will alter the landscape of many sectors and professions. All technology is always doing that. And it will create a lot of new jobs. It will change a lot of things. And some will be bad, then get fixed. And some will be good. And some will be unexpected. But what we hear now is mostly a list of future wrong predictions.

#10 – Artificial Intelligence CAN BE invested in within a dividend growth framework. In fact, it OUGHT to be invested in within such!

As fiduciaries, we can’t take a shot at a company priced at 60x earnings in the hope that it will become 120x earnings or that earnings will go from up 2,000% to up 5,000%. That can happen, but we can’t invest that way. It is outside of our principles.

What we can do is find companies with defensible business models, strong cash flows, and various aspects of AI backbone that may add value but won’t destroy 80% of the market cap if they do not. In fact, we own 3-4 such companies now. And management’s stewardship of their resources, promise, and present-day reality are all evidenced in a current dividend, a growth of dividend, and a fundamental defensibility that we can wrap our arms around.

We also can invest in companies that will use AI to drive efficiency and productivity in their own business. They don’t make ovens and refrigerators, they make food. Trust me, all you users of the internet and social media who no longer own AOL, Yahoo, Lucent, Compuserve, or Juniper … There will be companies who simply use AI to the betterment of their own profits, and you will get paid.

The payment will be called, a “dividend.”

Chart of the Week

No additional commentary to offer here.

Quote of the Week

“Men, it has been well said, think in herds. It will be seen that they go mad in herds, while they recover their senses slowly and one by one.”

—Charles Mackay

* * *

I am looking forward to the questions I get on this one. I am ready. And I wish you all a great weekend filled with human interaction and activity—the essence of a life well-lived.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet