Dear Valued Clients and Friends,

If one looks at the rapidity with which this market has sold off, the levels to which it has sold off, and the stressors that currently exist in our financial system and society at large, there is surely a lot of anxiety and uncertainty that permeates. This special Dividend Cafe will get into a handful of things that just simply must be said, offers a podcast from our Investment Committee, and addresses a lot of what is going on in the world that may help explain this crazy mess. Please, if you have time, join us in the Dividend Cafe …

************

I want to present a more comprehensive view of everything going on in our national conference call tomorrow. There is no need to RSVP unless you have a question you want to send ahead of time, and the phone number for participants is below.

Market update

Down over 2,000 points last Thursday. Up about 2,000 points Friday. Down 3,000 points today, Monday. The market opened down 2,500 or so, went as low as down 2,800, rallied back 1,400 points, and then spent most of the day down right near 2,000. In the final half-hour of trading, the market dropped another 1,000 points, leading to a 3,000 point drop that is the worst point day in market history and the second-worst percentage drop in market history.

Since last week the carnage has spread across other markets besides the stock market. Credit is largely clogged. High yield spreads have blown out to over 8%. Municipals are having a very hard time getting sold. There has been no place to hide.

We understand why stocks are down, but why is everything else experiencing distress?

The answer to this speaks to the very nature of our entire financial system. When one needs cash, they prefer not to sell what has gone down a lot, so they look to what has not gone down, or what is liquid and sell-able. When enough people do that, it makes what is liquid and sell-able less liquid and less sell-able. It is a vicious cycle, and last week there were extraordinary dislocations in the financial markets clogging all assets. They are the by-product of leverage in the financial system and a ton of forced selling taking place at once.

It is a brutal process to watch play out, but it has to play out for markets to achieve normalization.

Can the Fed help?

The Fed made a shocking announcement Sunday afternoon that they were cutting interest rates back to 0% (fed funds rate) and re-instituting quantitative easing to the tune of $700 billion. Of that, $500 billion will be in Treasuries and $200 billion in mortgage-backed securities. They also cut the discount rate to 0.25% (from 1.5%) – the rate banks pay when they borrow directly from the Fed. They gave forward guidance on their intent to hold things like this well past the immediate market distress, and until there is a total recovery in the economy from coronavirus, etc.

Why didn’t this help the stock market today?

It is going to take time for the Fed medicine to work its way through the financial system. Treasury notes can trade with wide bid/ask spreads as they are now, and it be considered a healthy financial market. Repo rates need to come down to the fed funds rate level to indicate healthy liquidity. And Mortgage Backed Securities should not be trading at such a widespread to treasuries. These elements will eventually benefit from Fed activity, but for now, the financial system is absorbing the pain of a lot of leveraged selling. It has piled on in equities, and it hurts.

When will it end?

More than anything else, we need positive news on the national health front. As data around the treatment of the virus shows flattening, containment, improvement, etc., it will allow markets to begin feeling the worst is behind us. Markets are so, so far out ahead of themselves here, we could and should see equities rebound well before the economy does. But the first step will have to be the health data showing real improvement.

Is a huge fiscal stimulus package coming?

We suspect one is, but the politics are still tricky. We will have more in our next communique and a lot more in tomorrow’s conference call on this.

Don’t you owe us more on oil prices?

Yes. I have a lot I am putting together to send this week.

Charts to digest

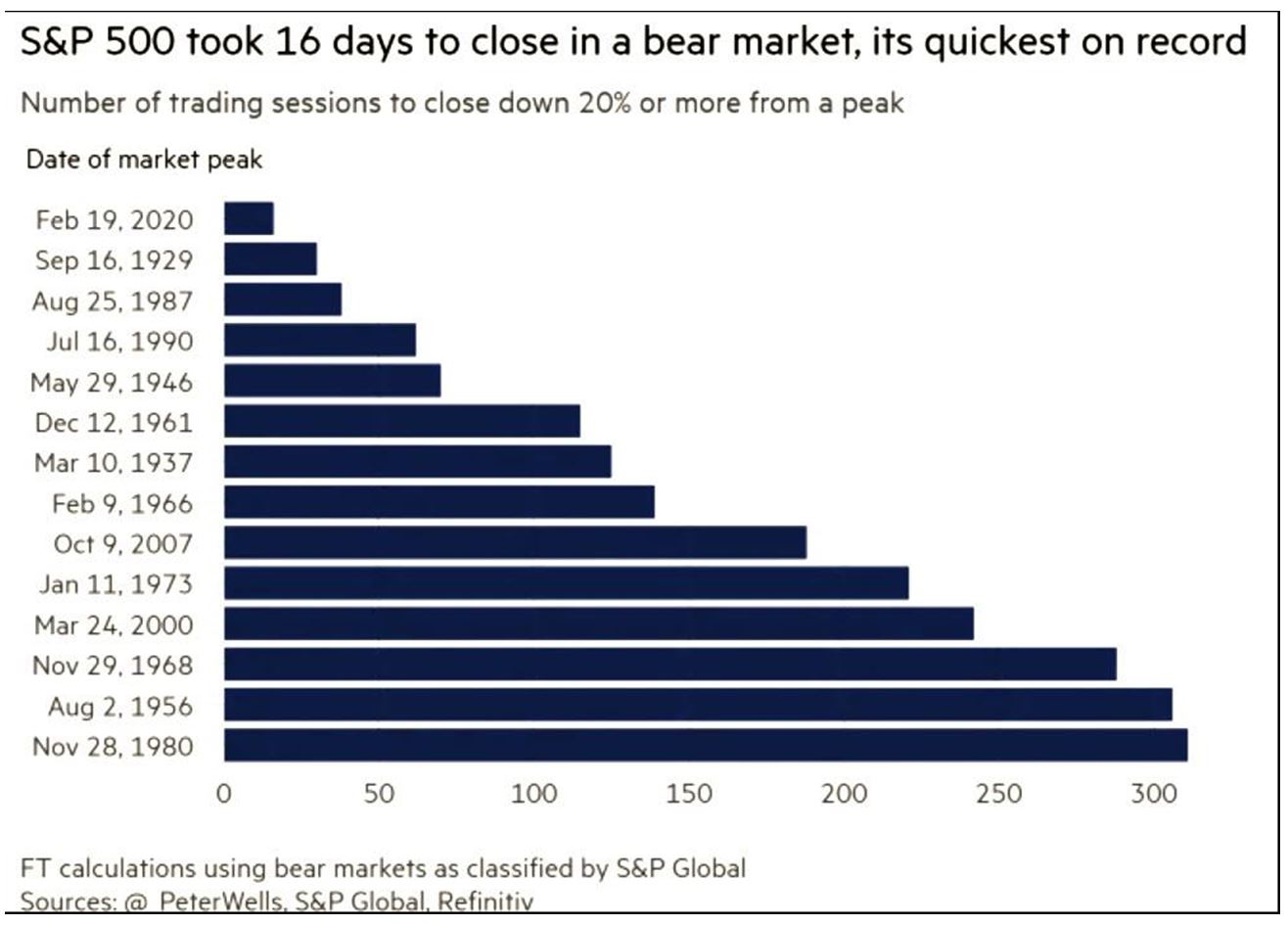

This chart just demonstrates the unbelievable violence with which this bear market has come upon us. The quickest avalanche into a bear market in history …

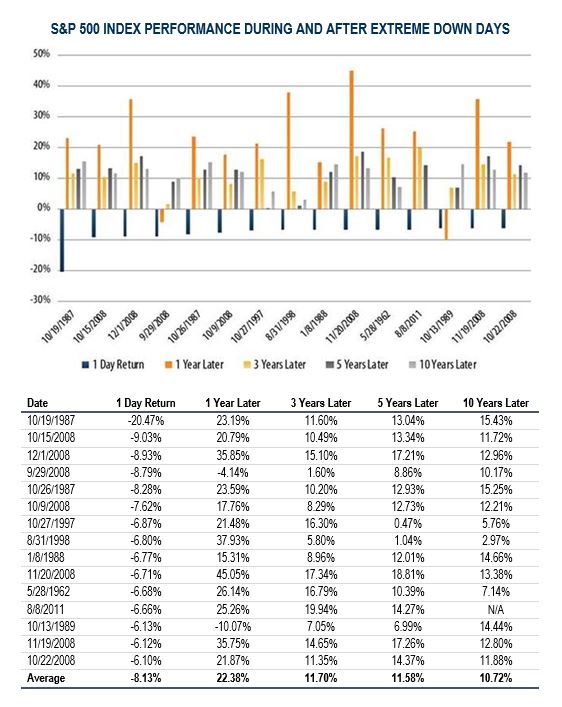

When we look to the history of how markets have performed a year after extreme down days like the ones we have had so much recently, the historical record provides much reason for optimism.

* Bloomberg, March 16, 2020, First Trust

Quote of the Week

“God, grant me the serenity to accept the things I cannot change. The courage to change the things I can. And the wisdom to know the difference.”

~ Anonymous

* * *

You’ll be hearing from me several times this week. We have a lot of work in front of us. We are all engaged in this fight. May our country be healthy and normal again, soon. In the meantime, please reach out to any of us at The Bahnsen Group. We know the distress is real. We are for you in every way, even if we can’t make it all better quickly. Being there for you is the end to which we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet