Dear Valued Clients and Friends,

As the new school year has begun, I have once again found myself in a classroom a couple of mornings per week, teaching an Honors Economics course to high school seniors at Pacifica Christian High School of Orange County. I taught the course for four semesters from fall 2021 through spring 2023 and then took two years off because of my, well, schedule (you really wouldn’t believe me if I told you what that entails). Somewhere in that time period, I memorialized the course as a free online offering for people who wanted to self-direct their way through it. With my daughter now a senior, I agreed to come back for one last hurrah and teach it again, and I have to say that I am having the time of my life. I love the students, I love the subject, and most of all, I love the fact that in a better understanding of economics, we can truly drive better outcomes in business, in finance, in public policy, and in all sorts of aspects of human endeavor.

This sets the stage for today’s Dividend Cafe. A couple of major themes have dominated global financial markets since the global financial crisis (GFC). The relative superiority of U.S. investment markets versus international alternatives has been stark, long-term, sustained, and meaningful. And it has not been an accident. The “best house in a bad neighborhood” reality of global economics is an important concept to understand. I have written plenty over the years about the “bad neighborhood” part of the equation (i.e., excessive indebtedness), but not enough about the “best house.” Today, we are going to look at the intrinsic economic advantage the United States has had and why we must fight tooth and nail to maintain it.

A little economics. A little history. A little national pride. And some warnings to take seriously about the future. It’s a lesson I love teaching, and maybe one of the most important lessons an investor can learn. Let’s jump into the classroom that is today’s Dividend Cafe …

|

Subscribe on |

A Conflict of Visions

I have a rather strong affinity for free enterprise deep in my bones. I love financial markets and have enjoyed a very rewarding career working within them to create solutions for real-life people with real-life financial goals and objectives. The task of matching client needs with solutions and using financial markets to do so is one I cherish, but I never confuse the chicken and egg here. Financial markets are not the end to which I work, but rather a tool (a massive, glorious, incomprehensibly blessed tool) used for the end to which I actually work. The precondition under which financial markets drive outcomes that improve our quality of life, that deliver goods and services to people who want and need them, and enable people to pursue their hopes and dreams, and that ultimately drives the process of human flourishing, is this little thing called free enterprise. I believe in a market economy because I believe it optimizes the conditions necessary to drive human flourishing, both for individuals and entire societies.

One of the lessons the students will be learning this semester is the “constrained vision” for an economic framework (to use the language of the great Thomas Sowell). Advocates of free enterprise do not suggest the system is free from the impairments of the human condition. Rather, what we suggest is that, utopia not being possible on this side of glory, all competing systems (to free enterprise) are worse. Everything an investor might think about as a good or bad investment has to be coupled with the question, “Compared to what?” The same is true for economic frameworks. We “constrain” our expectations for a market economy to the limitations that exist because of reality, particularly the reality of human nature. But our enthusiasm for free enterprise is born from its capacity to more optimally drive conditions for flourishing than any other system known to mankind. History has been relentless in driving home this reality.

My emphatic opposition to collectivism, socialism, and central planning is philosophical (what I know about the human person, social cooperation, and incentives all reinforce the merits of free enterprise and the dangers of contrary systems). It is empirical (what we have seen time and time again is that experiments to replace freedom with command-control economic planning have ended disastrously). It is moral (my ethical belief system puts a high regard on the value of private property and human agency).

So there is no ambiguity that my philosophy of investing is explicitly centered around the merit of freedom – freedom in enterprise, in trade, in entrepreneurial risk, and in markets that allow for the creation of wealth. I would suggest that apart from this, there is almost nothing that is actually investable.

In All Thy Getting, Get Competition

Investors are all competing for returns, sort of. This may sound like investors are competing with each other to get the best possible return (“I want to be up 10%” … “No, I want to be up 11% and beat you!” … “I want to own that stock” … “You can’t own that stock; I own that stock!”). It doesn’t exactly work that way. However, capital is most certainly competing for returns, meaning that it is always and forever looking for its most rational and efficient use. Investments, therefore, compete for capital. Investors are trying to participate in this miraculous (and glorious) process. But what is really going on when we talk about investments competing for capital?

Very simply: People are competing in the production of goods and services. Period. In this process of enterprise investments are made, risk capital is sought, capital achieves a return (or doesn’t), and the process results in the creation of wealth (successful goods and services meet human needs and wants, and the capital behind such production grows). Take away the competition that embeds production of goods and services, and you get a poorer society. It is competition that drives innovation, that drives product quality, that puts downward pressure on prices, that incentivizes new ideas, and that seeks rewards in the marketplace. Some elements of public life exist outside of a market framework (for example, the U.S. military does not respond to market signals and bears the burden and responsibility of national security alone). But where we put things in a market framework (commercial society) we are promoting competition, daring competition, and receiving the benefits of competition. And where we limit competition in commercial society, we impede market success and national prosperity. We will be coming back to this point shortly.

But with That Competition, Embrace Risk

Here’s the thing: Almost all anti-competitive actions I see in global markets are done because someone is trying to soften the reality of risk. The basic premise is that competition is good, but risk is bad, so where we can have a system of some competition, but with all sorts of risk moderation to keep people from suffering the downside of risk, we can have our cake and eat it too.

And it is perhaps the fatal premise for all under-performing societies that still pay some lip service to freedom. The more fatal conceit is the full-blown denial of freedom – a totalitarian state that doesn’t care about any of what I have said so far. But between the ideal framework of freedom and aspiration and a totalitarian compression of opportunity is, well, Europe. Put differently, plenty of Democratic societies have decided to maintain a broad posture of freedom (i.e., Democratic elections, representative government in some form, personal mobility, etc.) while deciding that an aggressive hand is needed to “soften” the competition effects in the marketplace. I would suggest that this becomes an outstanding metric by which to measure marginal investability (i.e., the more “softening” of market forces, the more marginally unattractive the investment opportunity set becomes).

Risk-taking can result in bankruptcy. Not taking risks can result in a dormant, stultified, stale, restrictive, tedious economy. Risk-taking can mean that capital may receive a negative return. Not taking risks assures one of capital stagnation. Risk-taking can create stress. Not taking risks results in paralysis.

In all the good outcomes of risk-taking, we get that which builds a civilization, but in the “bad” outcomes of risk-taking, we get nothing more than temporary setbacks, price signals, entrepreneurial lessons, market messaging, lessons learned, opportunities for improvement, and something that essentially builds a better future. This is not to minimize the pain that risk can create along the way, but the relationship between risk and reward is the textbook definition of asymmetry. The rewards bring lasting benefits; the risks bring only temporary challenges – and those challenges are, themselves, blessings in disguise. They inform producers, investors, and stakeholders of key messages that create value in the future. God help us if we ever lived in a world without risk.

American Exceptionalism

Other societies have fostered risk-taking, but none have done so like ours. Not even close. The gap between first and second place is substantial. And that encouragement of risk-taking when connected to the rule of law, to a culture of individual responsibility, to a political experiment that saw natural rights as created by God and secured a government that served at the consent of the governed, has been potent. It has created plenty of failures, but compared to what (remember)? Speculators often succeed when producers do not, and this strikes people as unfair or immoral. It is a fair emotional response, but not a fair intellectual one. We cannot get the investment (risk-taking) we need in legitimate goods and services without the possibility of circus clown grifter speculators being in the mix at times. We take the good with the bad, knowing that the laws of gravity always prevail in the end.

If the good we are after is a dynamism that requires no man or woman to stay in the same station of life permanently, we accept the fact that sometimes some people appear to be changing stations without the same level of work, sacrifice, and intelligence as others. Our commitment to economic mobility requires us to accept this. And our own personal agency and psychological well-being require us to get over it. There is a word for people who obsess over how unfair it is that someone else has gotten ahead “too easily” – UNHAPPY. Don’t be unhappy.

Sameness or Growth

There is a school of thought that a tight similarity in the wealth of citizens in a country is more important than the country’s absolute wealth. Many countries have a smaller gap between rich and poor than ours does. They are also, across the board, poorer countries. I do not mean merely “in aggregate” – I mean per capita. Roger Lowenstein pointed out this week in a Wall Street Journal article that per capita income in Arkansas (one of our poorest states) is higher than all of Germany, and that across the entire United States, per capita income is 84% higher than all of Europe. There are a million things that can be said (and have been) about how the economic pie should be divided in a rich nation, but one thing I hope we can all agree on is that we don’t solve for division of the pie by making the nation poorer.

(Capital) Market Forces

One extraordinary thing the United States has done is foster robust capital markets to promote economic growth. While many have decried “financialization” as somehow impeding economic progress, the United States has long used innovations in financial markets to facilitate risk-taking and the deployment of capital to all sorts of economic endeavors, and we have reaped the rewards.

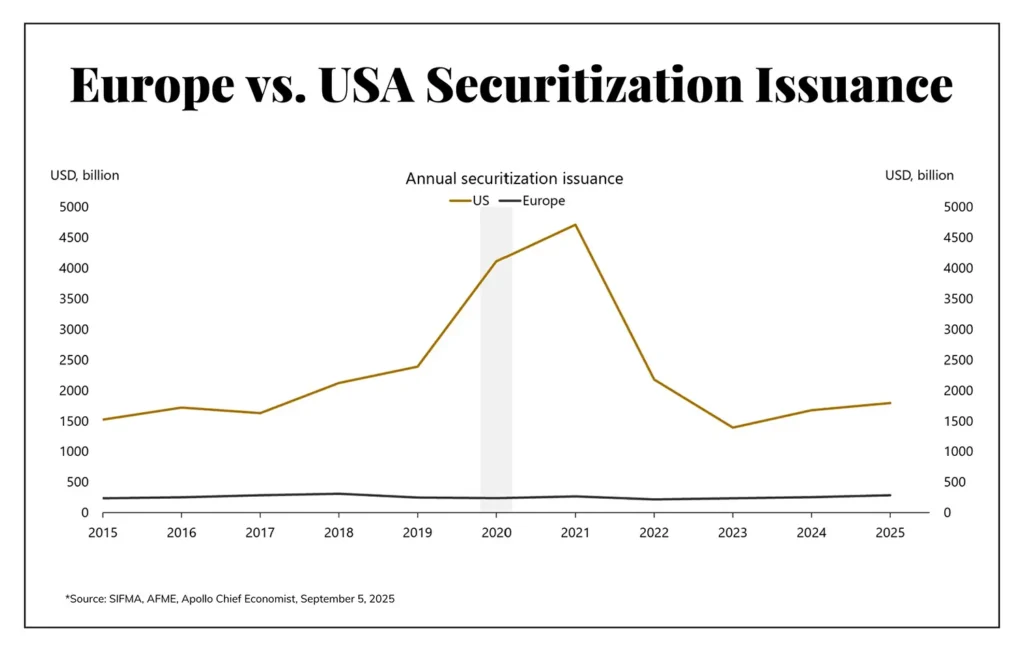

Securitization accounts for approximately 50% of U.S. GDP, compared to about 7% in Europe. We have a $30 trillion GDP and $15 trillion in securitization issuance. The financial instrumentation I refer to is often demonized as “tools for Wall Street dealmaking,” when, in reality, they are tools of lowering borrowing costs, creating investor liquidity, distributing risk efficiently, and expanding opportunities for capital to be deployed across a variety of markets far more expansively (from automobiles to consumer goods to commercial real estate to aviation to anything else creative minds can figure out a way to efficiently securitize). European resistance to securitization is not the opposite of “financialization” – it is resistance to growth and the unlocking of value creation.

Heart of the Matter

This gets me to why the United States has been so incredibly “investable” for so long, why its private and public risk assets have so substantially outperformed international competitors for so long, and why it attracts capital from all over the world … We have an economic framework that incentivizes risk-taking. We see millions of applications for new businesses every year. Yes, many of them fail. But what makes so many people take on the risk of reward if not the belief that, should they succeed, they will reap rewards?

This societal advantage cannot be maintained without a rigorous belief in the dignity of the individual (a dignity I can only defend as attached to creational reality). Changing the priority of business activity from individual hopes and dreams to some sort of constant social experiment is how good investment dies. Business endeavor matters because the human person is dignified and should be free to aspire to great things. A lower view of the individual serves as a rationalization for excessive regulation and bureaucracy that crushes investment. May it never be!

So Our Competitive Position is Secure, Right?

Every single thing I have said so far is under assault. Whether it be marginal or categorical, the basic beliefs and practices that have created economic exceptionalism face compromise and threat. Government rescue of failed enterprises harms competition and creates moral hazard. Impositions of collective social agendas on enterprises undermine the dignity of the individual and centralize economic endeavor in sub-optimal (if not fatal) ways. State control and ownership of the means of the production distorts resource allocation. The desire for “central planners” to come “protect” certain industries or economic actors is significant. In a lot of ways, we are victims of our own success: We have been so successful with the principles that have made us who we are that we think we have the luxury of abandoning those principles to try something different.

It is a lesson I do not want us to learn the hard way. And, truth be told, I am not actually as pessimistic as many are. I think we will do the right thing after we play footsies with the wrong thing a bit.

Conclusion

The United States has created over 250 brand new companies in the past fifty years that are worth over $10 billion, with the aggregate value of these “new” companies being well over $35 trillion. Europe has created just fourteen such companies worth about $400 billion in aggregate. 5% of the new company creation at that value, resulting in 1% of the value creation. Higher median incomes. Substantially higher small business creation.

These advantages and results are by-products of philosophical tenets that have stood the test of time. The question for investors as we look into the future is whether or not the superior investment region will want to become more like the weaker, or the weaker will want to become more like the stronger. At that crux lies one of the most important decisions investors will face in the decades to come.

And you know how I will be praying.

Chart of the Week

It may seem like an obscure financial metric to some, but at its core, it tells a crucial story of why one region has trounced the other in economic opportunity.

Quote of the Week

“All things being equal, you’d be a fool not to want to be poor in a rich country instead of middle class in a very poor country … The price of getting richer as a society is that some people will get rich faster—and richer in general—than others. That may be aesthetically or culturally displeasing, but a lot more wealth gets shared than the whiners appreciate.”

~ Jonah Goldberg

* * *

I really am an optimist. I can recognize the impediments of excessive government indebtedness without believing it will collapse our country. I can call out some of the marginal moves towards counterproductive central planning and managerial accommodations without believing that we will throw the baby out with the bathwater (in terms of our economic framework). I recognize that some people believe I am too negative (by even focusing on these things when they clearly have not yet devastated the American economy). And I know that some think I am too positive (for not focusing more on the marginal impairments we continue to tolerate in our own economic success story. But this is what I really believe – that we are the best house in the neighborhood, that the neighborhood is worsening, and that we owe it to our kids and grandkids to improve our own house as if civilization depended on it.

Invest as if your kids and grandkids depend on it. Because they do.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet