Dear Valued Clients and Friends,

One of the questions I get asked the most is, “what scares you right now?” Clients ask it every now and then, or some version of it, but I also get asked in various TV interviews that ever-so-compelling question, “what keeps you up at night?” There is one particular problem with the question I want to address in this week’s Dividend Cafe, and I want to provide a really thorough answer to it.

What is the problem with the question, “what is keeping you up at night?”

The problem is that the real question the person asking means to ask is, “do you think the market could go down?”

It’s a dishonest question, but probably not intentionally so. It’s a couched way of basically asking something reasonably worthless and unhelpful. Why is it worthless and unhelpful? Because the market can always go down, and anyone asking the question knows it, or anyone invested in the market ought to know it.

But, but, but you say – aren’t there times where it is extra super-duper extra likely to go down? And wouldn’t that have you worried? The answer to those two questions is, “of course not, other than in hindsight,” and “not at all.”

But, but, but, I say – if one ever just asked the question, “are there macroeconomic conditions that bother you, that you really dislike, that even though they don’t foolishly lead you into market timing or false prophesy or clickbait dis-ingenuity, you really are troubled by?”

Well, that question I can answer, and I will …

… in today’s Dividend Cafe.

Sleepless and Oblivious – no thank you

There is a general over-arching reality in the American economy that troubles me. It is not new – I have felt it and believed it since the aftermath of the financial crisis.

Now, these things do not keep me up at night (if anyone knew how tired I was by the time I go to bed at night after the days I have every single day of my life, they would know why nothing keeps me up at night). And no, these things do not “scare me” per se. Despair is a sin. I don’t do despair. I don’t like people who live in fear. I don’t like what it does to people’s emotional state, and potentially their financial state, to stay in fear.

I believe my professional and existential duty is to prepare for all comers, and I believe the various things that stand in the way of successful financial objectives are all dealt with daily at The Bahnsen Group. Not by being scared. Not by staying up at night (how does that help? Go to bed!). And not by pretending to know things we cannot possibly know (us, or anyone else)! Rather, by vigorous and intelligent planning, allocation, and portfolio design from the get-go …

That is our solution. And we do it to a coherent investment philosophy that we can defend, any time, anywhere. For the life of me, I do not understand how financial professionals can feel good about a financial approach for their clients that they have enacted which they themselves know is not rooted in a belief system, not rooted in a point of view, not rooted in any real disciplines or principles. I would feel more vulnerable about what we do for clients to counter-act the uncertainties of the day if I did not feel conviction in the basis for what we are doing.

But beyond conviction and discipline and principles and beliefs, an analytical approach to the conditions of the day is paramount.

Japanification: more a disease than a remedy

Long-time readers of the Dividend Cafe know that I am of the belief that excessively indebted societies are at great risk of putting themselves into a debt-deflation trap that can be horrific to break out of, if not impossible. In modern times, we have no shortage of major, developed countries that have experienced boom times, bust times, great fiscal spending to address the bust times, great monetary accommodation to address the bust times, and then more boom/bust cycle because of the fiscal and monetary medicine used to treat the aftermath of the last boom/bust cycle.

It is not controversial that this has happened. It is a mystery as to why it happens.

I believe that many financial professionals, or economists, or other such “analytical spectators” to the economic realities of a given era are essentially assigned a particular period of history that they get to live through, watch, study, and perhaps even opine on. Some extraordinary minds lived through the Great Depression (Irving Fisher, Ludwig Von Mises), the post-World War II era (Friedrich Hayek, Henry Hazlitt), the stag-flationary 1970’s (Milton Friedman), the supply-side success of the 1980s (Art Laffer, Bob Mundell), and the tech boom and globalization of the 1990s (too many to count – most still alive).

The early part of this new century began in the aftermath of the technology implosion and with a dangerous entrance into a boom cycle of our own – the U.S. housing crisis. While it took seven years to bust and then another 18 months to work its way through the financial system leaving carnage behind, that era represented an entire new period of its own in American economic life. I have studied every period of American economic history as exhaustively as I can, and I hope to study each period more exhaustively through the remaining decades I am given here on earth. Still, the era that will be forever inextricably linked to my adult life and financial career is the post-2000 boom/bust cycles of American economic life.

And out of the dot-com bust, and then the great financial crisis, and now reaffirmed and reapplied out of COVID, I am observing and responsible for managing through the conditions of some form of Japanification in the American economy.

There’s that word again

I was in high school in the late 1980s when the Japan boom was coming into its own. From 1987-1989 the rage of the American press (and future American President real estate developers) was the ascendancy of Japan and implications for American competitiveness. Japan’s boom was booming.

And Japan’s bust was violent. Real estate. Stocks. Leverage. Credit. Banking collapses. All the things. Just utterly devastating.

We can debate the causes of the boom, but Japanification did not begin with the boom. And it really did not begin with the bust. A bust can purge out the excesses of a boom and allow a normalization (after a lot of debt liquidation, which means a lot of pain and agony) to play out.

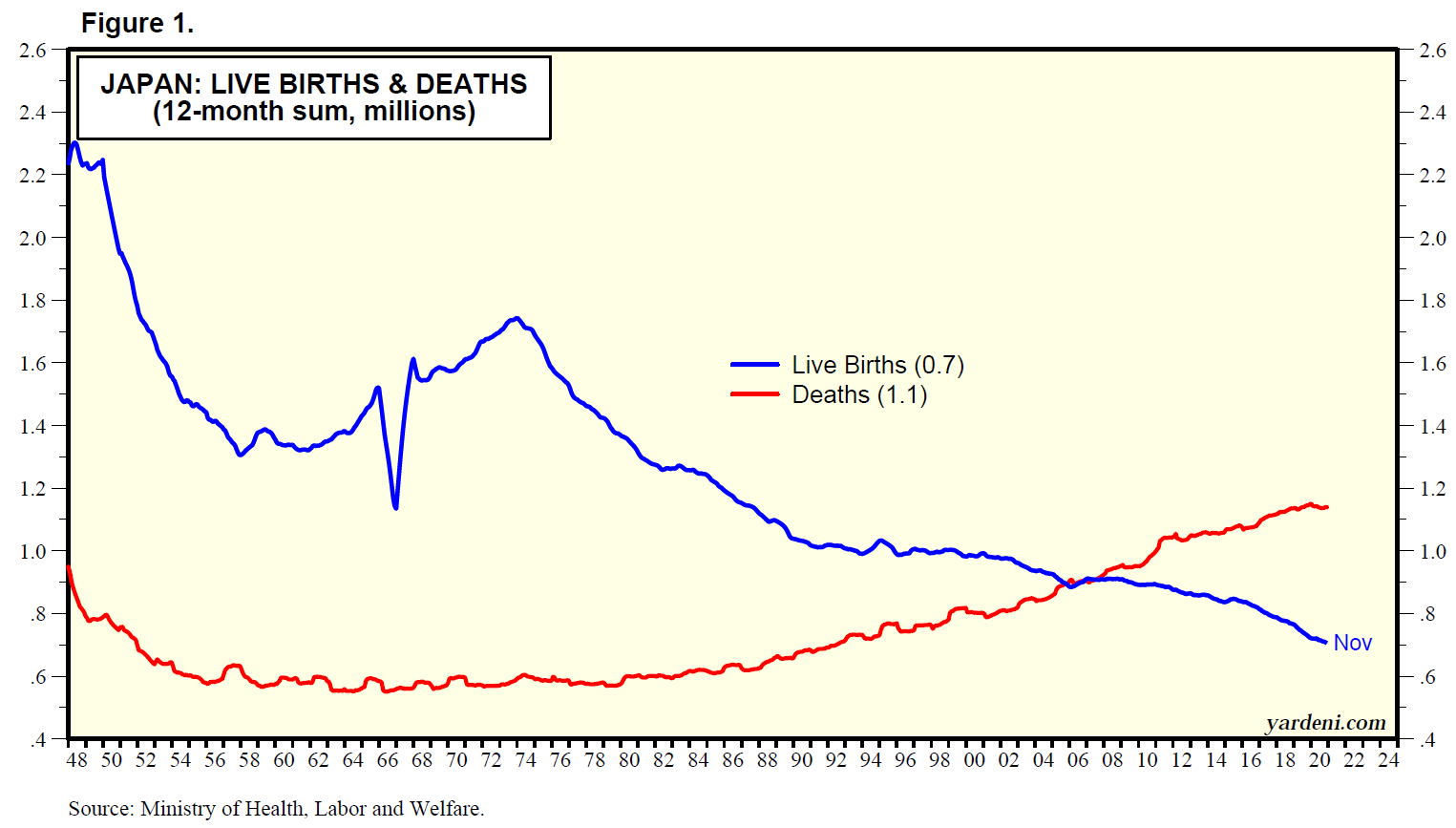

Japan needed a little more help than just merely seeing their bust cycle play out to purge the excesses of their boom cycle. Their demographics were perfectly aligned to feed into the great deflation trap of all time.

As Ed Yardeni’s charts always do, you see a lot of information here. The deaths began climbing right at the time of the bubble implosion (1989), and the live births were already in secular decline. Those two numbers went in opposite directions for the last thirty years, exacerbating and feeding the reality of a deflationary cycle.

What to do?

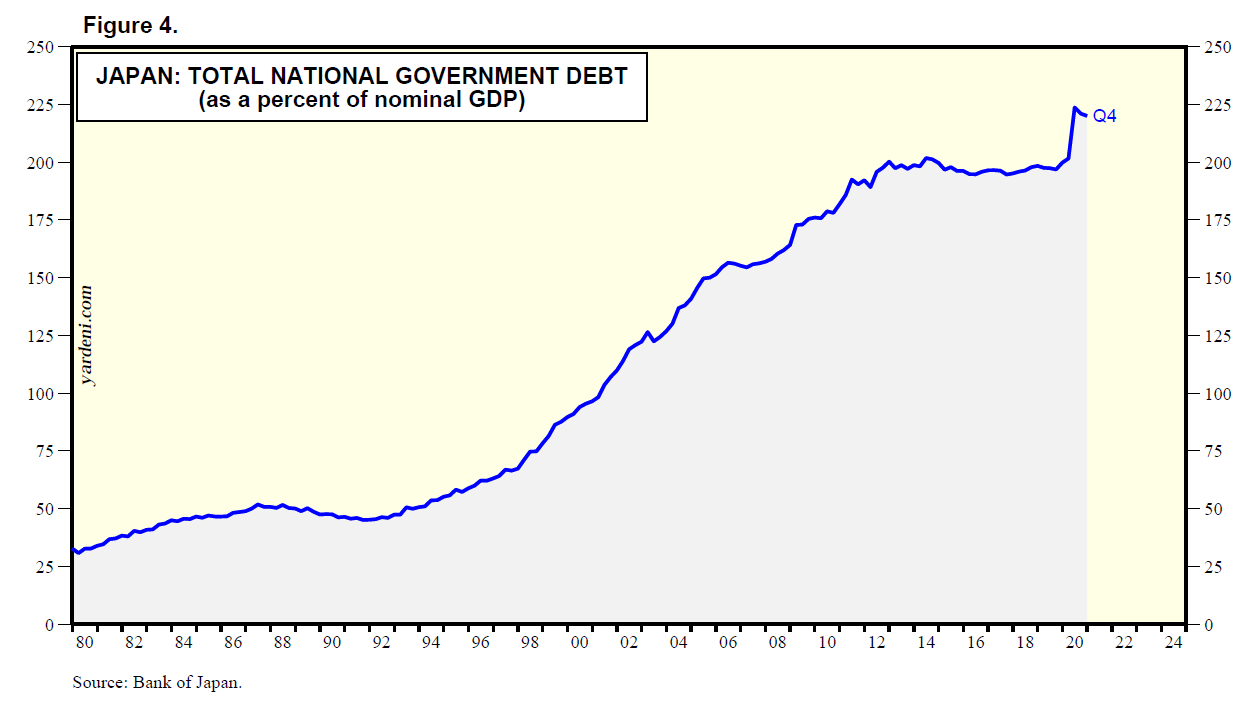

Budget deficits in Japan were 50% of GDP in 1993 – they are 220% of GDP now. It is almost a data point my keyboard does not even want to type.

This fiscal medicine (spend spend spend after borrow borrow borrow) does two things. On the one hand, in the short run, I can certainly accept the Keynesian reality that this fiscal spending, in the short run, offset the deflationary debacle that was playing out in real-time.

But it is also undeniable that it kept it from getting better, and in fact, fed on itself in the form of more debt, and the need for more debt still to deal with the impact of the fiscal condition. And this fiscal treatment required …

Monetary treatment

They work hand in hand, as we saw in Japan and now see in the EU and post-GFC America. Blowing out budget deficits requires some mechanism to fund it all. The central bank’s aiding and abetting was only magnified in Japan, where central bank independence is not even a pretense.

As you can see, they brought rates down to basically zero and have basically kept them there, well, for decades.

How has that gone for them?

I want you to here see the essence of “Japanification.”

Do not get me wrong. There would have been more contraction and more pain in Japan in the 1990s and subsequent pain of this deflationary cycle had they not intervened so aggressively in fiscal and monetary treatments. And maybe there are some there who believe it was worth it. I am not going to sit here and lie to you by claiming they had any good choice. There was no good choice – once you let a bubble excess form, you have no option but to take some pain.

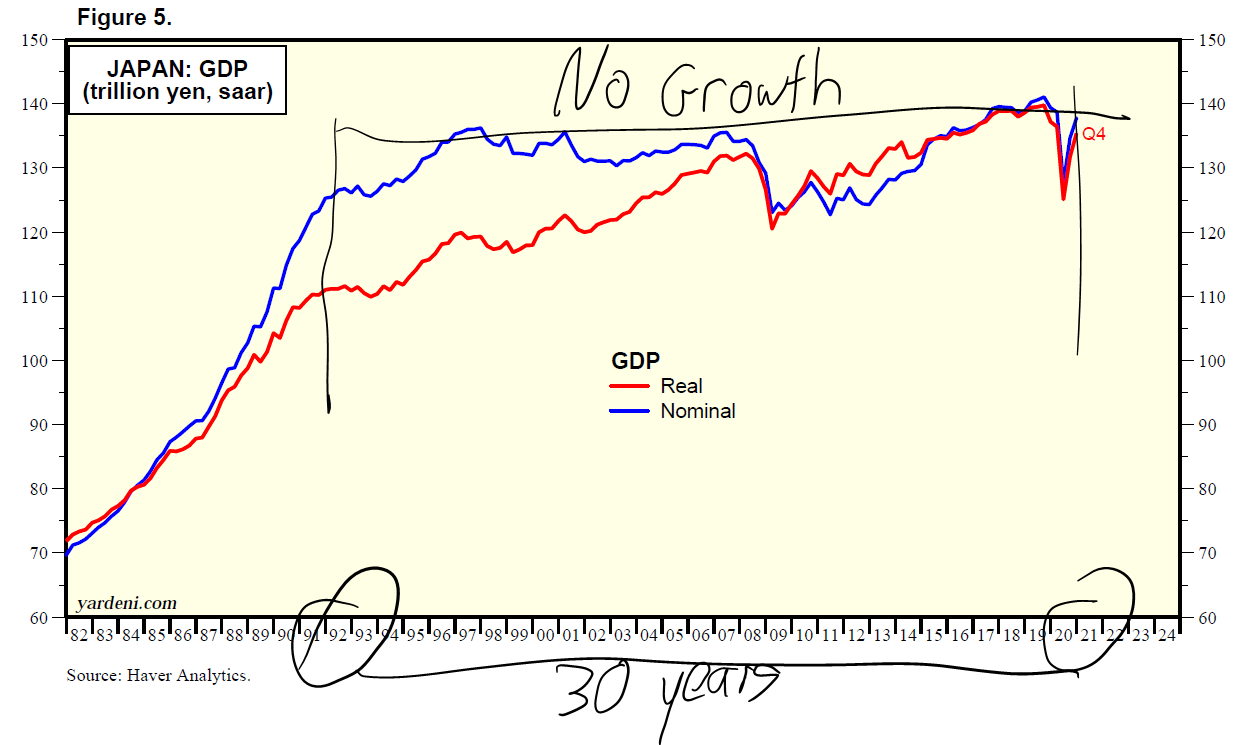

In Japan’s case, the pain has been the form of no economic growth for 30 years.

Is America next?

My view is that there are some key differences in the American economy vs. Japan’s, and yet even more similarities.

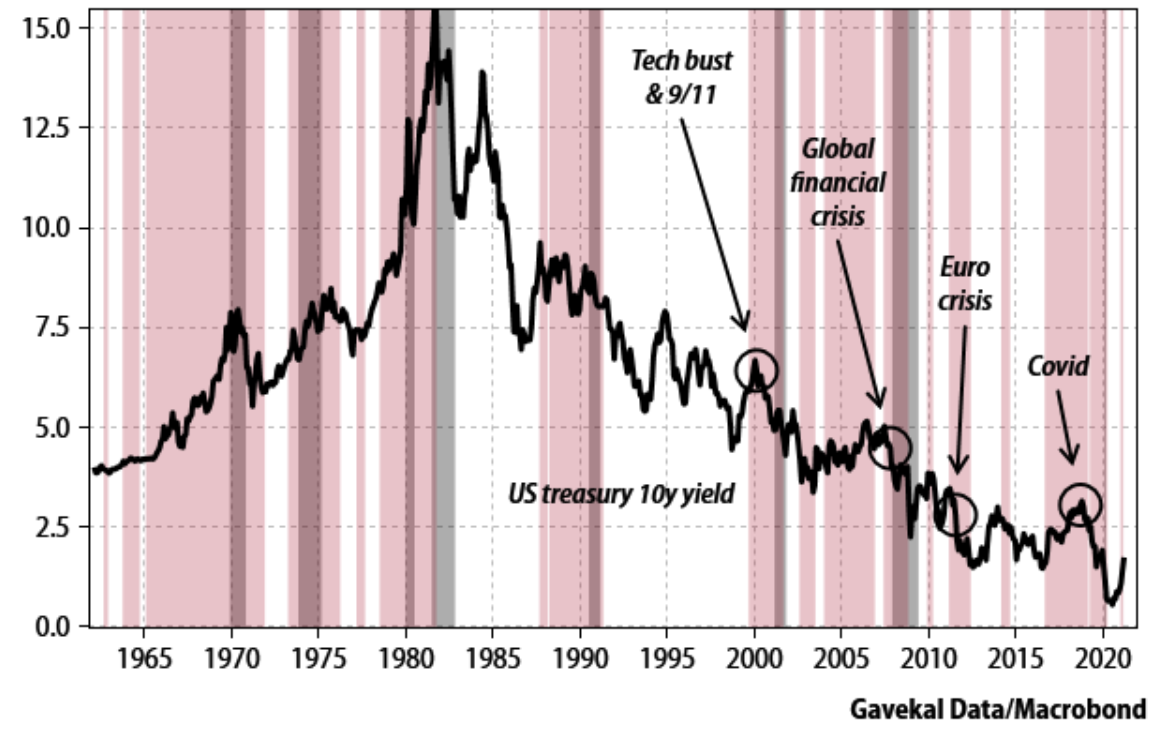

First, the similarities. Note the direction of our interest rates, exacerbated by each negative event we have faced throughout the last few decades.

I freely accept that the portion of this chart that shows the move from 15% to 6% or so was, itself, the removal of the other sort of bubble – the Volkcer-led 1980’s purging of 1970’s inflationary excesses. Upon that inevitable mean reversion, it is the subsequent race to zero (and these are nominal yields; real rates are negative) that is highly Japan-like. Shocks to the system, treated with fiscal and monetary medicine until the patient feels better, followed by a further drop in yields despite the patient feeling better.

The medicine never, ever stops during healthy years, and each time the patient gets sick again, the medicine is less efficacious. So we increase the dose.

Proof in the pudding

Fiscal aid helps aggregate demand when it happens (though even that it does so with a rapidly diminishing return, bout by bout). But then it pulls growth forward, reducing future investment, future wealth creation, future productivity.

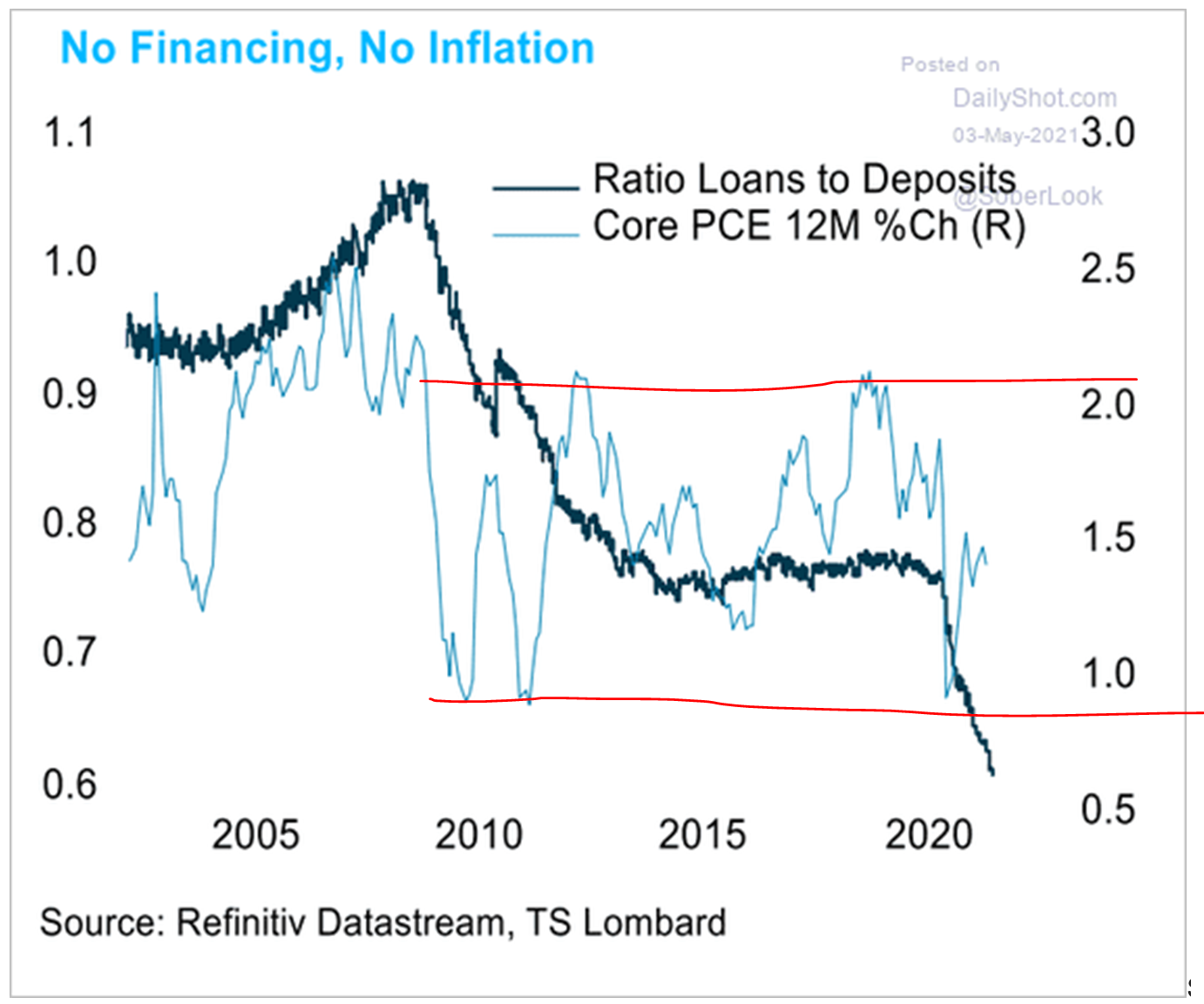

The Fed throws money at it, but it can’t get the money into circulation to inflate away our debt because there are not enough new loans to create velocity of money, which is to say, no inflation effect (despite their best efforts).p

Take your pick, but the answer is “yes”

When we hear about the disinflation of the era we are living in, we often hear that the cause is digitization/technology. Others point to the highly counter-inflationary impact of globalization. I have already pointed out the major role of demographics (declining population growth resulting from reduced fertility rates). And, of course, my hobby horse, the deflationary reality of modern fiscal and monetary policy.

People are free to debate which of these is the primary cause, but the answer is that all of these factors contribute. Any attempt to quantify or measure the relative impact is completely futile, non-falsifiable, and subjective. What we do know is demographics are a decision by the society. Globalization is a trend that has taken place. Technology is not going backward. But fiscal and monetary are, well, policy decisions.

Is there hope?

Of course, there is. Our debt is 125% headed to 170% of GDP, not 220%. Our fertility rate is 1.8, not 0.8. Our technology innovation is a 10 on a scale of 1-10. Japan’s was half of that. We have plenty of output that can absolutely change the pace of our secular growth decline.

But if we “Japanify” at a slower pace than Japan, will that mean no Japanification?

I don’t see how. Our trendline growth was broken, and we pushed debt-to-GDP through the roof to combat it, it didn’t combat it, and now the higher debt-to-GDP makes future growth harder to come by. Rinse and repeat.

We pushed monetary accommodation through the roof, now we are addicted to the medicine, it no longer has the same curative effect, and we lack treatment for the next time there is a real “emergency,” meaning I have to believe an even bigger shock and awe from the Fed awaits us in the future. Rinse and repeat.

Bottom line:

A significant amount of what I have said here is bullish for us holders of current risk assets, whether we know it or not. Excess liquidity works its way into financial markets. Declining growth in the future makes the good-growth assets of the past worth more.

But it also subjects us to bubble formation.

And it does so without the same risk mitigation tools we are used to having (a fed funds rate to cut, Treasury yields to drop and bid up Treasury prices, etc.).

It also lowers the growth opportunity for our kids and grandkids that many of us have enjoyed. It elevates social and societal tensions. It grows the cultural divide.

I would be happy to bottom line all this for you into an investment portfolio thesis, but we do that all day, every day. You know how we feel about that – we believe rising dividends from companies with pricing power mitigates the cyclical inflationary threats that we will continue to face. We believe that investing in a real, defensible business model with cash flow generation hedges the risks of investing into merely rising multiples or betting on perpetual popularity (those two being the chosen investment philosophy of most of America, even if not consciously). We believe that tail risk volatility (9/11, GFC, COVID) is too high to be 100% in equities, no matter how good the equity portfolio, so diversification around non-correlated assets is pivotal.

And we believe in being humble and nimble along the way. And having a lot of kids.

There’s no free lunch

I am submitting to my publisher the manuscript this weekend for a book that will come out this November titled, There’s No Free Lunch: 250 Economic Truths. There is no single greater encapsulation of economic cogency than the sentence, “there’s no free lunch.” We are not debating if there will be pain or no pain as we work through some of these economic challenges. We are debating about the composition of the pain, the distribution of it, and the magnitude of it. And there are highly respectable differing views on all of it. But there will be no free lunch.

Chart of the Week

Those yields on the right of this chart are NEGATIVE yields, as this is the “real yield” chart (net of inflation) of the 10-year Treasury index. I think it is absolutely imperative that people understand the incompatibility of a long-term inflation thesis with a NEGATIVE real yield (one that has dropped over 30 basis points since mid-March).

*Bloomberg, May 6, 2021

Quote of the Week

“A good summary of investing history is that stocks pay a fortune in the long run but seek punitive damages when you try to be paid sooner. Virtually all investing mistakes are rooted in people looking at long-term market returns and saying, ‘That’s nice, but can I have it all faster’?”

~ Morgan Housel

* * *

I am happy to have the book done and happy to have this Dividend Cafe done. I enjoyed writing it, largely because the view out my apartment window in NYC this morning as I wrote it was beautiful. But this message does not keep me up at night. It just keeps me deeply engaged and highly grateful for this moment of time I am called to. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet