Dear Valued Clients and Friends,

It has been a whirlwind of a week here in Newport Beach, appropriately loaded with client meetings, end-of-the-year tax planning meetings, a substantial amount of company leadership and portfolio meetings, and of course, all the good times that go with being with the Newport Beach people. I will be back in New York City tomorrow and working all week out there before heading out with my family to a secret winter destination for Christmas week (not a secret from you all – just a secret from the family I don’t want to invite … just kidding!).

This week’s trip into the Dividend Cafe talks a lot about “business optimism” (small and big business). There are plenty of things to unpack there if we are to understand what it means (and doesn’t mean) for markets and investors. We also cover the size of Nvidia on the global stage (literally), the latest in Trump 2.0 appointments, the state of financial regulation, some data on profit margins, and the lay of the land in IPOs. It is a deep and wide Dividend Cafe, and I heartily recommend you jump on in …

|

Subscribe on |

Bigger than the nations

This is your periodic reminder that Nvidia has a larger market cap than all of Canada’s stock market, and all of Australia, and all of France, and all of Germany, and all of Italy/Spain/Portugal COMBINED, and all of Scandinavia COMBINED, and all of Switzerland, and all of the United Kingdom … So countries that have been around for centuries have entire public markets worth less than one U.S. semiconductor company. Call it a concern. Call it a dunk. Call it an opportunity. Call it a long play. Call it a short play. But don’t call it uninteresting.

Just when I thought I was done, they pull me back in

The last several weeks of Dividend Cafe have thoroughly covered a wide array of appointments to the economic and policy team of the incoming Trump administration. And while there are certainly a wide array of less high-profile positions to be filled, it has seemed that the major positions of note to us investors have been covered (and, for the most part, encouragingly so). But this week President-elect Trump named Andrew Ferguson to lead the Federal Trade Commission (FTC). This stands in massive contrast to the current FTC head, Lina Khan, who I previously noted was someone Vice President-elect Vance actually spoke well of. Ferguson, a former congressional aide and a former Supreme Court clerk, is a huge advocate of deregulation and a less heavy hand from Washington, D.C., when it comes to mergers and acquisitions. He has indicated a desire to hold big tech to the fire still, but he is widely known to be a pro-market and pro-business advocate, and I would see this choice as an overwhelming positive for public equity markets.

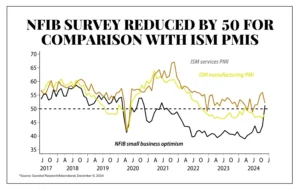

Small Business Hopes & Dreams

It doesn’t take a lot of detective work to notice one of the big trends when President Trump was elected President – both in 2016 and now again in 2024: Small Business optimism skyrockets (well, I guess this is a trend if you view two out of two times as a trend. All nine components of the index were positive, uncertainty declined by a stunning 12 points, and some form of optimism around anticipated tax and deregulatory activity is clearly palpable.

Now, that said, this is just that – optimism. It is not, yet, activity. Could disappointment overtake optimism? Could other factors overpower optimism around tax reform and deregulation? Is the Fed likely to be a factor in all this? I am not trying to rain on any parade here, but I think it is worth making two true statements at once: There is a general and meaningful optimism in the small business community right now that reflects a surge of planned investment, hiring, expenditures, and more – and at the same time, the need is still there for that optimism to translate into activity.

What optimism outside the mom and pops?

Small business optimism matters in the real economy, but maybe Wall Street optimism matters even more for public market investing. And on that front, the results are basically identical to NFIB small business readings. The New York Times ran a story this week about Wall Street enthusiasm for Trump 2.0. There have been numerous stories about Silicon Valley’s optimism and support. Some of the stories focus on what appear to be former Trump critics seeming to “kiss the ring” for pragmatic reasons, but much of the sentiment, abundantly clear in public equity markets, is simple “optimism.”

Is large-cap optimism merely the same thing as small-business optimism centered around expectations for a more favorable tax and regulatory environment? Or is there a categorical difference that is worth better understanding? I think it is important to remember that optimism is a “feeling,” and the “feeling” here is that there will be a more favorable climate in the areas that impact financial markets and economic activity. Feelings can be reversed as easily as they can surface, but yes, I do believe a non-specific optimism can be sourced to expectations for more favorable tax and regulatory treatment. However, I would add, and this speaks to the vulnerability here – that some of the optimism is a matter of unwinding what has been a loaded-up pessimism – namely that cabinet picks and agency heads would be problematic. The business community feels, and I more or less agree with this assessment, that the more controversial or potentially problematic picks are largely outside of their lanes. People may have strong feelings about the candidates selected for Secretary of Defense or FBI Director or the Director of National Intelligence, but they see the Treasury Department, NEC, EPA, Energy Department, Commerce Department, FTC, SBA, SEC, and so forth and so on as reasonably allied with the cause of business. Even with tariffs, as addressed last week, there remains a “hope” that the worst-case scenarios are not really serious.

I care about personnel. I care about policy. But I would never make an investment decision about optimism. People “feel good” about things all the time right before they stub their toe on their nightstand. The data is there, and whether it is small business or big public companies, there is no reason to ignore it. But no, it is not predictive or even actionable. But it also is not entirely irrational by any means.

Proof in the pudding

You know what really causes small businesses to be optimistic? The production of goods and services! (Kudos to all my economics students who were screaming the answer in advance). The correlation of ISM activity with both services and manufacturing and how small business owners “feel” about things is historically very tight. Now, optimism has jumped in advance of the ISM survey data jumping. If services and manufacturing follow – if business investment follows and greater productivity and economic results follow – the result is a positive feedback loop that drives economic growth. If production does not follow, optimism does not hold. Eventually, if Dallas Cowboys fans start to give up (not this one, but you know what I mean).

Financial Deregulation

I have already teased that a big theme in my annual white paper (coming January 10) wherein I analyze the Year Behind (2024) and offer my extensive commentary on the Year Ahead (2025) is going to have a deep focus on the nuances of planned tax legislation. I am engaged in conversations on this front with legislators, advisors, and Trump 2.0 officials on the daily, and I believe the tax piece of 2025 is substantial.

But another big theme going into 2025 is going to be financial deregulation. The alphabet soup of agencies that oversee our nation’s financial system would be a mystery to most people if they understood it all, and the low-hanging fruit for improvement in this is massive. A lot is on the line for what this means to the economy, but a lot is on the line for financial sector investors, as well. Regulation compresses Return on Equity, and Return on Equity is heavily correlated to the multiple financials receive on their book value. Consider yourself teased.

IPO nostalgia

There were over $500 billion of IPOs in 2020 and 2021, and there has not been even $70 billion of IPOs in 2022, 2023, and 2024 – put together!!! Now, the 2020 and 2021 volume was pure anomaly – the SPAC craze was, well, crazed, and it provided a shiny object boost that was blown to smithereens in 2022. So comparing the 2020/2021 levels to 2022-2024 levels is somewhat apples-to-oranges, but even looking pre-2020 we averaged about $60-70 billion per year in IPO transactions, and that average has dropped to $20-25 billion over the last three years. On the line when it comes to these things we discuss, like financial market liquidity, risk appetite, exit multiples, M&A, and so forth – is IPO volume. 2025 is going to be interesting.

CPI vs. PPI

Everyone loves to comb through the data each month to form an inflation perspective whenever these monthly figures post (which is fair enough, even if the combing often done is not, shall we say, very good). But what is missed when one is obsessively trying to say “inflation is sticky” or “inflation is gone” or, as some who get it say, “this is all silly – why is the shelter lag so long and pronounced?” is that perhaps the most important data right now is the delta between producer prices and consumer prices. These things have a relationship with one another, but the timing and the nuances within the data are not linear or perfect. So it is with a grain of salt that I say that, generally speaking, the spread between CPI and PPI speaks to profit margins in the corporate sector. In theory, what consumers will pay and what it costs producers to make something is called a profit margin and while margins have been record-setting, that declining spread between consumer prices and producer prices is potentially indicative of a moderating environment for margins ahead.

Third time’s a charm?

With the market set to close the year up over +20% two years in a row, it bears asking – does this happen a lot? Well, actually, it has happened seven times over the last hundred years, which means we’ve been in one of these periods about 20% of the time over the last century (I know, 7x two years is 14 – not 20 – BUT the > 20% thing happened five years in a row 1995-1999 so those years are included in the 20% thing. So when the market is up over 20% two years in a row, what historically happens with the next year? Well, half the time, it has been up and half the time down. So use that data point to form an opinion on 2025!

Chart of the Week

Maybe hosting the Olympics isn’t as great a thing for one’s economy as people seem to think (actually, since Peter Ueberroth and 1984 Los Angeles, that has pretty much been true everywhere). But what you see here is just nasty – incomprehensibly nasty.

Quote of the Week

“Humor is the insight that nothing is as serious as it seems… Humor combines reason and serenity. It testifies to knowledge, insight and judgment and a developed mind. Humor is a character trait, a virtue, comparable with courage, honesty or modesty. Humor allows a wider perspective. It strengthens the ability to see things the way they are.”

~ Andreas Thiel

* * *

The Monday Dividend Cafe will have a little update on some things I am hearing about the 2025 tax bill plans, including the latest with the SALT deduction cap. But it is also going to go around the horn as we always do. I’ll know more of our publication plans for the holiday weeks next week and will share immediately.

In the meantime, have a wonderful weekend, and reach out with any questions. I hope you are ahead on your Christmas shopping, or, if I am being a truth-teller, I hope your spouse is as on the ball as mine is …

Truth-telling is the ethos of TBG. To that end, we work, even if outs me on things you could have guessed anyway.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet