Dear Valued Clients and Friends,

Long-time readers know that I have strong opinions about the Fed, about monetary policy, about its relevance to economic conditions, and of course about its implications for investment decision-making.

Today we have enough misinformation out there about the Fed that it may be a chance to actually use that word appropriately. And this misinformation comes in a period of elevated interest. The stakes are high.

This week in the Dividend Cafe we are going to see if we can’t make more sense of what the risks are and are not around current Fed actions. And in so doing it will allow us (force us?) to touch on a handful of peripheral subjects that matter. It’s an easy read, digestible, and actionable.

So jump on into the Dividend Cafe …

The plot thickens, but too many aren’t watching the right movie

The obsession with what the Fed will do this year with interest rates and its balance sheet is a constant, never-ending demonstration of economic fallacy and market ignorance, sometimes innocent, and sometimes click-baity. But all of it bothers me not for where it is wrong, but for where it is wrong causes us to miss what is importantly right.

If I were a capital market investor today who believed that the Fed has spent ~25 years backstopping risk assets (and in some cases actually promoting them), and yet was about to enter a prolonged period of removing that backstop, it would be a game-changer in my view of risk premia (that is, how to think about the risk and reward in current capital allocation). And indeed, I do believe the Fed’s support (implicit and explicit) of risk assets has been undeniable since the 1990s. That is not to say the Fed is the sole or even primary reason for the performance of risk assets in this time. To believe that is to misunderstand the very concept of human action, the genius of the profit motive, the stark reality of self-interest, and the global movement towards democratic capitalism. But to deny that the Fed’s “put” has been there post-LTCM, post-dotcom, post-GFC, post-Euro, post-COVID, and so forth and so on, is to live with our heads in the sand.

And yet I do not believe the great impact to risk premium that the Fed has created is in the backward actions of what they actually reactively did in these various situations. Rather, it is in the impact those actions have on forward expectations. Investors can invest for growth, innovation, cash flow, and all the rest, with some degree of belief that “left tail risk” is hedged by the Fed. Does anyone believe that belief is not there? And for that matter, does anyone believe it is wrong-headed?

This is worse than that

The Fed staying at 0% longer is worse for markets because it counters the great advantage the Fed brings to risk assets: Mitigation in the case of super bad events. The Fed can not go lower if it is already at 0%. There will be more bad events. If you don’t believe that, I can’t help you. If you don’t know that, you need to. We have not cured for the business cycle. We have not cured for geopolitical sins. We have not cured for most of what has ailed humanity for millennia. And markets have baked into valuations (the risk-free rate and the risk premium) the confidence that the Fed will be there when those things get too hot.

Getting off the zero bound restores some capacity for the Fed’s best contribution to market returns – bandwidth for action in the case of really bad stuff.

So yes, being off the zero bound is better for risk investors than being on the zero bound, no matter how much you like levering up at record low interest rates and feeling like a real estate savant.

There is true humility in investing when interest rates are not 0%.

But aren’t markets saying otherwise?

They’re doing no such thing, and won’t be if we drop a lot more, either. The volatility thus far this year has been elevated, but market performance has been totally benign for all but the shiniest of objects.

Shiny objects get their froth removed for reasons not involving the Fed all the time (though the Fed can certainly pull forward those days of reckoning).

Markets may hem and haw and zig and zag for a while, but re-pricing around a 0.75%-1.5% discount rate is simply not meaningful in the grand scheme of things.

So QE doesn’t matter either?

Surprises to the markets matter. If the Fed’s balance sheet is reduced slowly, and with ample telegraphing, I wouldn’t alter my messaging much around this issue, either. But my underlying point is that Fed front-running, speculating about the speculators, and algo/vol plays notwithstanding, the market cares more about its belief that the Fed will be there when wanted more than what actually happens in what is actually an economically expansionary time like now.

And will the market appreciate the Fed reducing inflation?

The problem with the question is the premise underneath it. I do believe inflation’s growth will be substantially lower in 3-6 months, but I do not believe that is because the federal funds rate will be 0.5% instead of 0%. In fact, I find that idea laughable. What will bring prices down is a closer equilibrium to supply and demand, which is to say that that which is impeding the production and availability of goods and services to meet demand levels will have to directionally correct. And that will bring back disinflationary forces. And that will have nothing to do with the Fed.

Are you saying no level of tightening the Fed could do will hurt markets?

No. What I am saying is that with debt-to-GDP at 120% and climbing, we have no room for massive Fed tightening. Could the Fed tighten to the point of an implosion for the U.S. budget deficit? Sure. Will they? I’d say not. Rather, would I expect the Fed to reverse direction well before the debt service created an irreversible problem? Yes, I would. Do I expect the Fed to chicken out at the point of credit market distress? Indeed, I do.

Ideally …

A majority of talking heads bemoan that Fed tightening may cause some over-levered companies to fail. If credit spreads widen, it is possible that companies living on a thread with monetary accommodation could meet their fate. But ideally, that would be a feature, not a bug, of some Fed normalization. This is not to say that I cherish the idea of company failure or job loss. It is to simply say that on a macro level, capital is best served by chasing its most optimal destination, not by being diverted into subpar zombie companies. Resource allocation is improved when the Fed behaves more naturally, and as a defender of free enterprise for the right reasons, I favor optimal resource allocation.

Emerging perspective

Who is the last country on earth to still be trying for a “zero COVID” policy? Well, let’s just say that omicron is not cooperating with the futility of this failed approach very much.

Why is this relevant? I am not sure any macroeconomist has given any reflection to the implications for China re-opening its borders, easing restrictions, and, brace for it, even restoring a policy bias of pushing banks to lend.

Now, to be clear, they have stayed closed (stubbornly) for two years. They have no political risk to maintaining the brutally ineffective lockdown policies (many western politicians are so jealous of the handy benefit of not fearing votes whatsoever). And face-saving is a part of Xi’s ethos, it would seem.

But really, a re-opened China, and a re-liquefied China, is not priced into global growth, is certainly not priced into emerging markets equities, and would likely go a long way towards easing supply chain challenges.

Would I bet on it? Truth be told, I would.

A quick note on safety

It occurs to me in my non-stop drumbeating on the dangers of “shiny object” investing … We have seen part of FAANG get taken to the woodshed this year and the other part down, but not down a ton. I have gone to great lengths to define what a “shiny object” is – those popular, trendy, momentum, cult-like aspects of the market that are bough for their shine and not for their truth, therefore enabling price to be so disconnected from reality that risk becomes severe. Well, FAANG or parts of FAANG may have or have had valuations that I find stretched and unsustainable, but I actually would offer a different caveat about my FAANG skepticism versus the shiny object argument. I truly believe many “mega-cap tech” names have not so much been given shiny object status, as safe haven status, and that may be just as unhealthy, even if it is a different category of unwise. A safe haven like the U.S. dollar, or Treasuries, or what people think Gold is, or the Swiss Franc, etc. means something very different than “big tech.” Parking lots to store money where principal can be preserved in the midst of uncertainty are as desirable and coveted as ever – and when one starts to believe something that is anything but is a “safe haven” – a store of value – an alternative to volatile equities – it does not end well.

Big tech may prove to be a good investment or a bad investment from this point forward based on a lot of things. But it can not be a “safe haven from volatile equities,” because it is volatile equities.

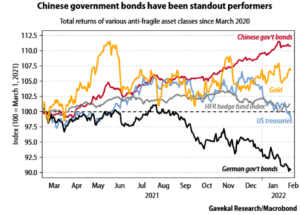

Chart of the Week

Just looking at the “safety” asset classes – not all of the “risk assets” that we know have done extremely well since the COVID moment of March 2o20 ended – it is Chinese government bonds that have done best, hands down.

Quote of the Week

“By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some.”

~ John Maynard Keynes

* * *

I will leave it there for the weekend. Markets continue to go up and down. The Fed continues to be a source of anxiety, and sometimes, for all the wrong reasons.

If one is going to fret about the Fed, we want them to do so for the right reasons. To that end, we work.

Happy Super Bowl watching!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet