Dear Valued Clients and Friends,

Virtually everything going on in markets right now (or so it would seem) has to do with what central banks are doing (or are projected to do). It certainly is not true in reality – the things happening today that will ultimately determine investment outcomes in years to come will have far less to do with the cost of capital and far more to do with human action – but in the day-to-day volatility of market price levels, I have no choice but to pretend. Well, “pretend” is not actually the right word – it is more an acknowledgment that the world we are living in gives a lot – and I mean a lot – of attention to the Fed in one’s outlook on financial asset pricing and economic health.

The current obsession with the Fed (as in the immediate 2022 and soon-to-be 2023 period) revolves around inflation. We have had a cult-like obsession with the Fed for over 25 years, so it is not inflation that created the Fed’s place in our hearts and our wallets. But right now, inflation is the cause du jour – the rationalization for 24/7 coverage of the Fed, and certainly the Fed’s stated rationale of heavy activity in financial markets.

Much of this is with good reason. Much of it is so misguided that I don’t really believe I am hearing what I hear some days from people I know [used to?] know better. But all the talk about the Fed right now is tied up with all the talk about inflation, and therefore a re-visit on the inflation subject is in order.

Jump on into the Dividend Cafe, and may our investigation of the state of the nation when it comes to inflation bring some revelation about the Fed’s imagination in matters of monetary administration as we pursue our goal of wealth creation.

|

Subscribe on |

Pretext is everything

The simplest explanation of why the Fed Funds rate is currently 4.25% and why it is projected to get near, at, or above 5% in 2023 is that inflation went up a lot in 2021 and 2022 and that the Fed needs to use its policy tools to bring inflation down. One of the Fed’s “dual mandate” objectives is price stability, and high inflation is counter to the objective of price stability. Simple enough.

The assumption is that tight monetary policy is anti-inflationary, which follows from another not-usually-explicitly-stated implication that easy monetary policy is inflationary. Both of these assumptions would be true if the other one were true, but the reality is somewhat more complex. A better way to say it is that excessively easy monetary policy can be inflationary and that tighter monetary policy can be anti-inflationary. But as is often the case, certain nuances and caveats matter.

Nevertheless, the current dynamic assumes the following fact premises:

(1) The Fed was really easy in monetary policy out of the COVID moment,

(2) High inflation surfaced in 2021 and 2022 because of the Fed’s easy monetary policy

Therefore, (3) The Fed will need to implement really tight monetary policy to defeat those inflationary effects.

Premise #1 is true. Conclusion (#3) is perfectly valid if both premises #1 and #2 are true (and connected). But is the pretextual assumption in #2 accurate? Is the present inflation a by-product of easy monetary policy, thereby commanding a tight monetary policy solution? Herein lies the rub.

Won’t be my last caveat

I am about to argue that a substantial misunderstanding of the 2021/22 inflation is the cause of errant prescribed solutions that have become mainstream. But that is not the same as saying that the easy monetary policy of 2020-22 was a great thing or without truly awful consequences. If I say that eating too much fast food does not cause osteoporosis, that does not mean that I believe fast food is good for one’s weight, heart, blood pressure, etc. (I just guaranteed myself two things with that last sentence – someone is going to write me to make a case that fast food does actually cause your bones to become brittle, and someone else is going to write me to make the case that fast food is good for your heart and blood pressure; this is the life I chose). So I can, and do, all at once believe that excessively easy monetary policy can be distortive, ill-advised, dangerous, an impediment to organic structural growth, and so forth and so on, without believing that in this specific case, it was the cause of the major inflation elements we have seen.

Just as I can believe smoking can be bad for your health without thinking it does anything negative for your lungs (okay, just kidding, I know it is bad for your lungs; I just figured if I poke the crazy bear a little, I might get less email, but now that I think about it that may be a bad strategy).

Setup Redux

Formulating an expectation as to what the Fed is going to do, not to mention what one believes the Fed ought to do, would help to better understand what really did cause the inflation of 2021/22. I have long argued that there is a delta between what the Fed has to say and what the Fed really believes, and I have not said that so much as a criticism as just a statement about how the world works. I also believe there may be a delta between what the Fed really believes and what the truth on the ground is, but even in that case, the point is the same – at some point, the delta between fact and fiction – between what is said and what really is – compresses, and manifests itself in changing circumstances.

Where are we now?

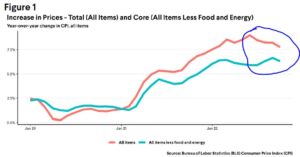

This week the Consumer Price Index was released for the month of November.

Inflation picked up in 2021 as the world began re-opening, and the growth of inflation peaked several months ago and has begun a slow decrease from peak levels, but with the overall price level still substantially above its pre-2021 levels.

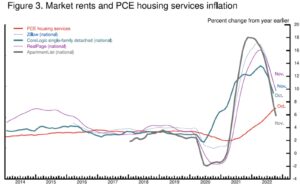

The basic argument that housing/rent prices are over-stated in the CPI is easy to make. “Shelter” shows a 7% increase even as the real-time indicators show this:

*Bloomberg, December 2022

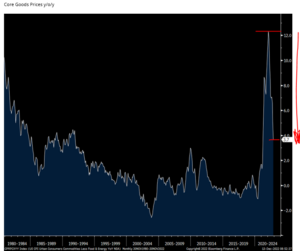

Transportation costs are now deflating. Medical Care costs have come down two months in a row, but they are a volatile and funny thing. Recreation, food and beverage, and various services are still inflating. Apparel and many household products are substantially disinflations, and total core goods are really stabilizing, if not downright deflating.

*Boock Report, Bloomberg, Dec. 13, 2022

Services, particularly Shelter, continue to reflect above-trend inflation, and select items like Food remain elevated as well. Energy prices are way down, but the highly volatile nature of Energy prices is why we look at “Headline” inflation (everything) separate from “Core” (with food and energy stripped out).

The lay of the land is much better than it was six months ago, but nowhere near desired targets.

Supply-Side Inflation if There Ever Was One

The COVID pandemic shutdowns did more than merely collapse DEMAND as people were locked inside their homes. The lockdowns collapsed the PRODUCTION of new goods and services. Then, in early 2021 “demand” normalized (people resumed living), yet “supply” didn’t.

I am very open to a discussion of the policy errors that I believe are embedded in this theory of the case. And indeed, this theory is riddled with what I believe are policy errors. My goal here is not to absolve anyone of blame; in fact, it is to avoid further policy errors.

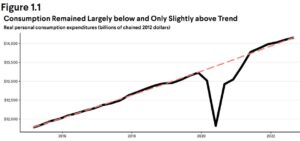

But the “aggregate demand needs to be tamed by tighter still monetary policy” misses some really inconvenient truths about post-COVID inflation. For one, consumption didn’t really move – it merely normalized:

*Joseph Stiglitz, The Roosevelt Institute, The Causes of and Responses to Today’s Inflation, December 2022

Even this return to trendline consumption was robust, as history generally does not indicate post-recession demand normalization this quickly. I imagine this to be the idiosyncratic nature of what caused the contraction – not organic economic slowdown, job loss, or diminishing consumption appetite, but a forced and really kind of unappreciated removal from economic life. I would argue without any real desire to press the issue that “pent-up” demand was very high.

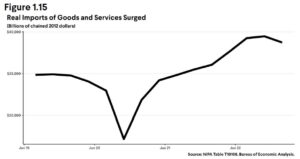

Okay, so consumption comes back to normal post-COVID (the number one rule of economics: “humans act”), and how are we set to meet those consumption demands? Consider the following:

*Joseph Stiglitz, The Roosevelt Institute, The Causes of and Responses to Today’s Inflation, December 2022

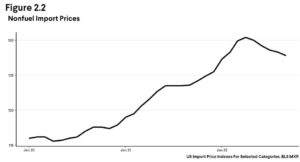

So what does one do if they are not making enough goods themselves? Well, they import them, of course.

The cost of those imports (excluding fuel) did what? Skyrocket higher. Semiconductors, Energy, and Shipping costs flew higher, and along with it, the prices people pay for things that touch semiconductors, energy, and shipping (i.e. pretty much everything). You can bet the recent downtick in inflation is related to this recent downtick in import prices.

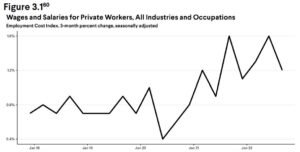

What about wages? The Employment Cost Index (ECI) is only 1.6% higher than it was pre-COVID. Certain sectors have seen wage costs go up a lot, and others have seen no change at all, but the idea of a Fed-induced aggregate demand pushing all wage costs higher has been, well, false.

*Joseph Stiglitz, The Roosevelt Institute, The Causes of and Responses to Today’s Inflation, December 2022

At the end of the day, all different nations of all different fiscal and monetary responses to COVID experienced inflation-price pressures because the ONE universal circumstance was an era of normalized demand faced with a moment of inadequate supply. There would not have been uniform global inflation (that saw the dollar RALLY, I might add) if unique U.S. monetary activities were the primary cause. Global supply challenges led to global inflation.

The Economics of it all

In a nutshell, conventional monetary policy is supposed to curb aggregate demand where inflation has come about because of demand-side excess. Monetarists like me and Milton Friedman believe that excess money supply relative to goods and services pushes prices up (because of math) where velocity is stable. I believe that if all we have is ten bananas on an island, two people, and exactly twenty dollars, you have a certain price for a banana. And then, if all you have is STILL ten bananas on an island, and still two people, and no new goods or services, but then you have forty dollars, the price of those bananas will go higher. In a complicated society with more than ten bananas and more than two people, the quantity theory of money becomes more complicated, still. And yet this much is true – a stimulation of aggregate demand without a corresponding increase in supply certainly adds to the price level. Therefore, looking to the central bank to use monetary policy tools to cool aggregate demand is sensible (in this paradigm) as far as it goes.

The problem is that we did not have inflation of surging aggregate demand brought about by accommodative monetary policy. We had a surge of inflation brought about by inadequate production of goods and services.

I promised you another caveat

My belief that Fed monetary policy was not the primary cause of container shipping costs, labor shortages, oil supply inadequacy, transportation expense, import expense, or semiconductor challenges is not to be confused with a belief that the Fed had no role in housing inflation. I doubt anyone has written more over the last twenty years about the role of easy monetary policy in promoting housing bubbles. I am here referring to two bubbles: the pre-crisis one of 2002-2006, otherwise known as the mother-of-them-all, and then the COVID bubble of 2020-2022. How could we have a housing bubble right after we had a nasty housing bubble? As my friend Rene Aninao of Corbu likes to remind me – “we are a stiff-necked people” (Exodus 32:9).

But my point is this … I have just offered multiple paragraphs and charts earnestly and [I think] persuasively arguing that the lion’s share of our inflation these past two years has non-monetary causation, and yet I find it painfully obvious that Fed policy fed the housing bubble. These are not inconsistent positions; some might say they are more thoughtful … =) Look, I can be wrong on both (maybe the Fed did cause shipping container prices to go higher and didn’t cause housing prices to elevate), but it is not an inherent contradiction. Housing is the textbook definition of a rate-sensitive purchase. One’s monthly payment is more impacted by the interest rate on their borrowed money than any other variable in a purchase. I suspect that the heavy QE component in the purchase of mortgage-backed securities did much to inflate housing (even as I am sure it did a lot to distort the liquidity and supply/demand in those assets). But I am certain that interest rates at 0% – and held there for a long, long time – did a lot to escalate the conditions that fueled housing’s meteoric rise.

I not only believe housing prices are coming down and will come down, but I believe they should come down, and I believe the Fed’s monetary policy should make them come down. And I do not believe that this is a negative for the economy (whatever will someone who bought a house for $1 million fifteen minutes ago and told their friends it was now worth $1.7 million when they see their neighbor sell for $1.3 million? Horror of horrors). Markets clear prices, eventually. There is an equilibrium of supply and demand that we call a “price” in the civilized world, and that price discovery out of the varying conditions of demographics, income, family formation, residential preferences, down payment affordability, underwriting, etc., all are capable on their own of finding a price that works for buyer and seller. It is what we call a “market,” – and it works better without a finger of twelve academics on the scale.

Conclusion

It is impossible to predict exactly when the lag effect of CPI shelter reporting catches up to reality on the ground of declining housing/rent expenses. It is impossible to know what geopolitical realities may do to energy and food prices in the months/quarters ahead (Ukraine, OPEC+, Biden/ESG, etc.). What I do know is this – the overwhelming evidence is that the cause of 2021/22 inflation was primarily supply-oriented, and those supply issues are normalizing rapidly. As the inflation data turns south, three questions will be relevant to investors:

(1) At what point does disinflation cease, and what becomes the “new normal” of inflation? Back to the 1-2% level of the last 20 years, or down to something higher than the 2% target?

(2) What damage is done to the economy in the foolish pursuit of “taming aggregate demand”? Does a severe recession come as they go about signaling their seriousness around inflation?

(3) When the current inflationistas lose focus and get distracted by subpar economic growth once again, how will this “Japanification” play out for investors, elected officials, and all economic actors in the years and decades to come? Because it’s coming.

Chart of the Week

There are plenty of ways to look at the housing market right now – builder sentiment, input prices, purchase volume, new construction, mortgage finance, sale prices, etc. – none of them reflect an upward trajectory right now.

*Strategas Research, Investment Outlook, Dec. 13, 2022, p. 8

Quote of the Week

“The good news is that all the recent indicators point to inflation moderating on its own. There is now increasing evidence that supply side problems are at last being resolved. Key prices like energy and food show strong mean reversion—they’re returning to more normal

levels—and that will be disinflationary. Hopefully, this will induce the Fed to exercise even more caution in its policy of monetary tightening.”~ Joseph E. Stiglitz

* * *

I am going to have a long-written DC Today on Monday, but no podcast or video.

I am going to do the written DC Today summaries Tuesday thru Thursday, but no podcast or video.

Next Friday’s Dividend Cafe will feature something we have never done before in written form.

There will be a Weekly Portfolio Holdings Report this Wednesday but not the week after.

And on Friday, January 6, we will be releasing the Dividend Cafe, my annual white paper summarizing the year that was and the year ahead. I expect a doozy.

In the meantime, enjoy that final holiday shopping. If I were a Keynesian, I would tell you that you owe it to the economy to spend more and save less so as to do your part to stimulate aggregate demand. But hey, everyone says “demand is too hot,” – so I guess by not shopping more, you are doing your part to bring down inflation!

It is hard to keep track these days.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet