Dear Valued Clients and Friends,

There is a lot to chew on this week, starting off with one of the most important investment lessons an investor will ever learn. But then after the basic refresher in human psychology this week we also have a pretty important observation about the current geopolitical climate and the market, a little Ukraine prediction, and some other tidbits for your economic edification.

The opening ceremonies in Paris are just hours away, and nothing says Paris like the Dividend Cafe…

|

Subscribe on |

Logic-Emotion Balance

In my newest book, I fervently criticize the idea of “work-life” balance – a neo-pagan concept that I think is often well-meaning but pretty much incoherent and ultimately dangerous when it comes to how we think about our lives. Well, when it comes to investing, “logic” and “emotion” can, indeed, be in tense (“work” and “life” cannot, but you would have to read the book). The term “in tension” does not mean we can mathematically solve it – it means exactly what it says – that there is a “tension” that has to be reconciled in the reality of human nature … That is, we are all at once human beings driven by logos and pathos – and the varying dimensions humans have do not turn on and off like a light switch. This makes for an interesting consideration when it comes to investing. Our emotions and our capacity for reason often alternate in what governs decision-making, and one can strongly override the other at various times.

One such time where pathos might override logos is when it comes to maintaining a balanced and diversified portfolio. Emotionally, no one likes a “loser” in a portfolio, and logically, everyone knows that when you have a balanced portfolio, something has to be the “loser.” Even highly emotional human beings do not generally lie to themselves to the point of believing that they could (or should) own six different asset classes at once that always perform positively and always in positive tandem with one another. I mean, I think even crypto investors know that is insane (hey, just having fun, that’s all).

So here is the point I am making … A balanced portfolio means, always and forever, that something is frustrating you, AND that you are supposed to be happy about it.

Let’s walk through this. The argument I am making is that a balanced/diversified portfolio is a good thing because we believe in diversifying systematic risks with various asset classes and categories of strategy, and we believe in diversifying non-systematic risks so that a unique or unforeseeable situation in a given company or sector cannot tank the entire portfolio. It is risk mitigation for the purpose of survival, and survival is a sine qua non in investing (and in life).

Okay, so you have a good thing that is done intentionally for the purpose of survival (diversification within and across asset classes); what could happen within this? Well, everything could go down at once at the same level, and that would be pretty bad and probably not a good indication of a well-constructed portfolio. And you may think it could all go up at once and at the same level, but then why would you think everything going down at once and at the same level would be bad? All that would mean is that you did not have the diversified portfolio you thought you did! So maybe now you take the bait and say, “Okay, well, I do want the protection against systematic and non-systematic risks you previously mentioned, but I want that to come from you getting me in and out of these asset classes as opportunities and reality call for.” But hopefully, you stopped yourself before you said it … If you didn’t, stop yourself now before it costs you money!

So, back to the point I am making … You start with the accurate belief that a durable portfolio uses diversification to protect, and that is a good thing. You accept the reality that no scenario is coming where you are diversified with timing – getting in and out of all the right and wrong things at all the right times. So then, what happens?

Well, you are going to have a statement come where one stock you own is up +14% in a month, and another is down -3% in a month, and your pathos may say, “Why didn’t I just own the one up 14%?” And you will have a year where one asset class is up 20%, and another is up 1%, and, again, you might find yourself hating one and loving another.

And this is a prime example where one has to allow their logos to trump their pathos. If we forget the imminently undeniable things – that rearview mirror investing is impossible, that the balance of the portfolio is strategically brilliant, and that the MATH of something always being down more than something else is inevitable, we can save ourselves a lot of regret, a lot of grief, and maybe even more.

Non-partisan market volatility

As of press time the Nasdaq was down -8% from its all-high achieved a whopping ten days ago. The S&P 500 was down -4.3% from its’s all-time high just over one week ago. Surely, this is a market response to the geopolitical tensions of the moment?

Biden might run – he might not – wait, he definitely won’t. Trump will win – or he might not – or he won’t – or who knows. Oh, also, a bullet came within a half-inch of killing former President Trump less than two weeks ago. The Democrats will need to nominate a new candidate at their convention. Oh wait, they have a candidate. Tel Aviv has been hit by drones. Russia/Ukraine is as uncertain as ever. Bibi spoke at the U.S. capitol, and Hamas protestors put a Palestinian flag up in place of a U.S. flag. It’s just touchy out there – politically, militarily, domestically, internationally – it is touchy.

And so, do the two paragraphs above intersect with one another? Well, if they do, one would have a hard time explaining why the bond market hasn’t moved a whisker. 10-year yields have stayed within 4.20% and 4.30% the entire time. The dollar has barely moved. Oil prices are actually lower, not higher (geopolitical tensions are supposed to push commodity prices higher, especially oil). Plenty of things in markets are up, not down – financials, consumer staples, banks, energy, small-cap – in some cases, quite significantly so.

It isn’t anywhere near a “risk-off” rally, and it obviously is not a “risk-on” rally. No, it is as selective as can be. That is not a geopolitically driven sell-off, my friends.

So what gives? Why are the Nasdaq and the S&P 500 down when so many other aspects of risk markets are not? If not geopolitics, what?

Valuation, period. Valuation. Over-priced assets revert to the mean. Now, they also can keep going higher long after the period of over-valuation begins. There is no law in the universe about when mean reversion begins. But no plausible explanation exists or is needed for market action later beyond this – some things were very over-valued, and some things were not.

And that will be true next week, no matter what happens in the Presidential race (and something will, I assure you).

Forward thinking

I do not have a crystal ball about anything other than UCLA’s ongoing troubles in fielding a men’s football program (hey, Dividend Cafe is mine!). The list of things in which I lack the ability to predict the future includes the outcome of the Russia/Ukraine war. I do not say the following as a prediction or as wishful thinking but purely to game out something that I imagine most rational people have to think is at least possible. If we were talking about something prescriptive (what ought to be), first of all, I do not think most people care what I think on such matters of foreign policy. Secondly, I find the issue, much like so many other things in our contemporary political debates, to be filled with nuance in an era where nuance is really hard to do. I do not equivocate in my vehement opposition to Putin (some seem to struggle here), and I certainly do support U.S. support of Ukraine, even as I favor a clear understanding of the use of funds and accountability around strategic priorities (I don’t think any of these things contradict each other). I would like to see a sovereign and independent Ukraine repel attackers and invaders and live happily ever after.

That said, by way of prediction, I do expect an eventual agreement is going to come (“if something cannot continue, it won’t” – Herb Stein, again), and I think that agreement will involve concessions from Ukraine. How does Trump (or anyone else, including other European NATO countries looking for an off-ramp) get Zelensky to agree to any concessions with Putin/Russia, who invaded them unlawfully? Well, if I were a betting man, it would involve money. Call it a hunch. The cost to rebuild Ukraine is going to be hundreds of billions of dollars. I don’t think a telethon or aid concert is going to pay for it.

So, what am I getting at here? And what will it mean for Russia? I expect a significant industrial, materials, commodities, and capex investment to come. Louie Gave has pointed out that the huge commodity discount embedded in current trade with Russia, China, and India would likely go away. There is ample reason to believe global prices could re-price higher and even more reason to believe demand will surge for a huge rebuild. This general theme is not easy to invest in, but it essentially adds a global (and specifically Ukrainian) accent to a broader theme we already have in America: Capex, Commodities, Materials, Industrials – it seems a moment may come that further reinforces the theme. Food for thought …

Chickens come home to roost?

I read a report this week that “in recent years, governments have begun to print significant amounts of money” and that “because of this, government debt has stopped being a reserve of value and is now underperforming gold.”

Well, what exactly is new about these governments printing money, I am unsure of. That excessive government spending and excessive monetary facilitation to such government spending is the status quo is most certainly not new.

I have said this for many years but feel it bears repeating. Gold may be up or down in the years ahead – I have absolutely no outlook on such whatsoever. Gold may be up or down relative to other asset classes like government bonds – I also have absolutely no outlook on such whatsoever. But I do know this – the notion that in history, gold has proven to be an antidote to bad government behavior (fiscal or monetary) is categorically false. Sometimes, yes. Sometimes, no. Which means no.

Groundhog Day

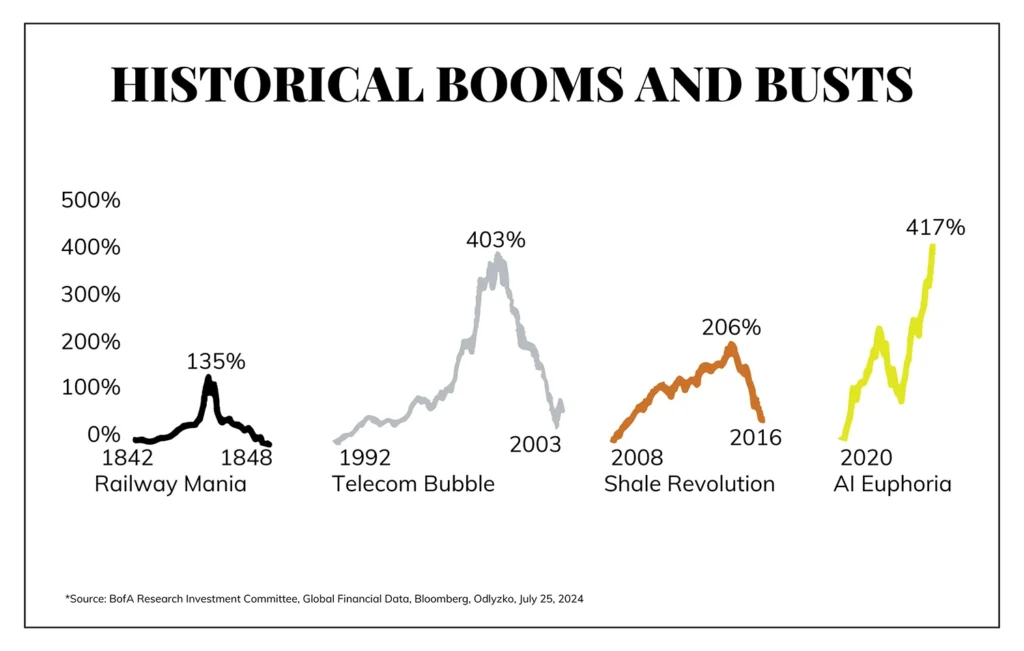

Some things really do change the world. They really do become economic juggernauts. Railroads. Broadband. Shale. And I suppose artificial intelligence may soon be on that list (I wouldn’t rule it out). I am also sure that the paradigmatic significance of a given thing has never excluded investors from way, way, way overdoing it along the way. Pathos over logos.

Broken streak

The S&P 500 being down over-2% on Thursday represented the first time such had happened in a single day of trading in 356 days of trading. This was the longest stretch without a single day down -2% in 17 years!

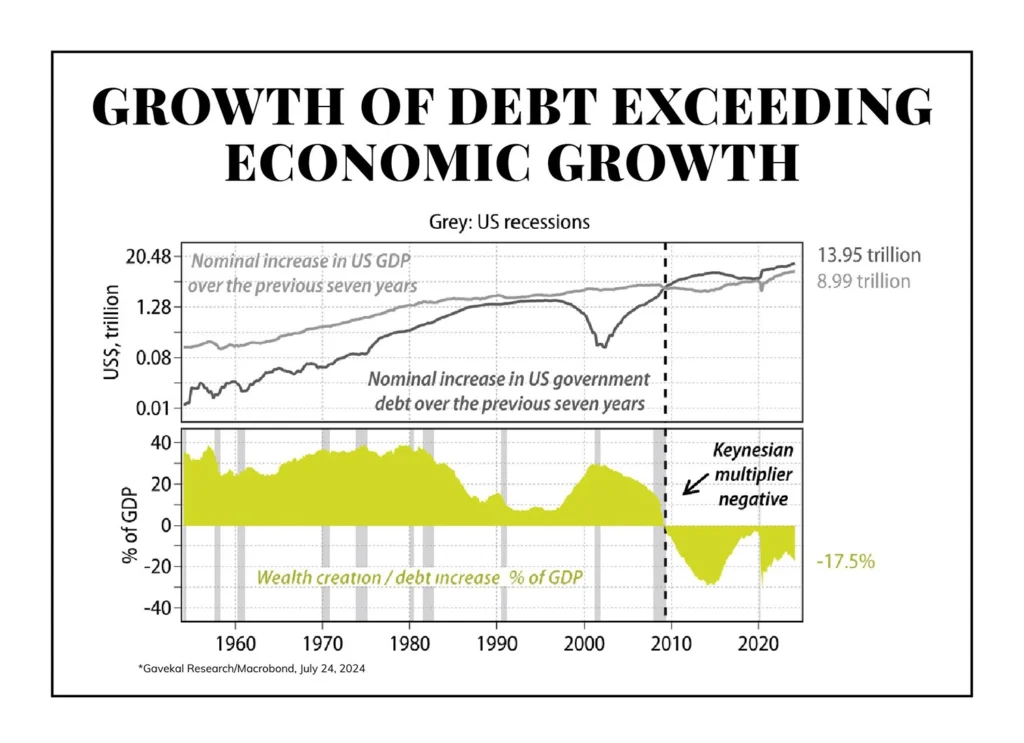

Chart of the Week

I can’t think of a more powerful expression of the economic story of our time. The issue is not the growth of debt, as fascinating of a story as that is. It is the growth of debt exceeding the growth of the economy itself. This is the unsustainable path of which I speak.

Quote of the Week

“There are no new eras—excesses are never permanent.”

—Bob Farrell

* * *

It is a bit extraordinary how significant the news cycle has been in the last couple of weeks. I would love to say that I am looking forward to calmer waters (talking about news, not markets), but I am not holding my breath. In so many ways, this election cycle is turning out very much the way I expected, which is to say, filled with the unexpected! And if that seems illogical to you, just let your emotions do the thinking for you. That way, it will make a lot of sense.

Logic and emotion, always and forever, held in tension. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet