Dear Valued Clients and Friends –

Brian and I did split duty today as I did most of the writing before my departure, and he will handle the podcast and video as I embark upon my Christmas week with my family. I do want to wish you and yours a very Merry Christmas, and I will be back with you next Monday, the 30th, for the final Dividend Cafe of 2024.

Dividend Cafe on Friday did a deeper dive into the recent “market sell-off” and the paradigm shift last week’s Capitol Hill chaos means (and doesn’t mean). The written version is here (my favorite), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

- The market opened modestly lower this morning on light volume, although it regained ground through the trading session, closing into positive territory.

- The Dow closed up 67 points (+0.16%) with the S&P 500 up +0.73% and the Nasdaq up +0.98%.

*CNBC, DJIA, Dec. 23, 2024

- $150 billion flowed into U.S. equity ETFs – in the month of November alone. What could go wrong?

- Speaking of which, credit spreads have also become extreme. An interesting historical metric is the high yield corporate bond yield minus Fed funds. Just prior to the GFC, when Fed funds were at a similar level, and credit spreads were also tight, this relationship was at 1.99%. Today, we are just off all-time lows of only 1.27%. Regardless of the strong economy we have, this is credit risk complacency and something we keep a close eye on.

- The ten-year bond yield closed today at 4.59%, up 7 basis points on the day.

- Top-performing sector for the day: Communication Services (+1.35%)

- Bottom-performing sector for the day: Consumer Staples (-0.57%)

- An interesting statistic I was not expecting to see: a record level number of American CEOs departed in 2024, an amount that was +19% higher than last year, to be precise. Do 1,824 CEOs feel a call to non-profit activity or altruistic endeavor, or for some, have stock prices gotten irresistible? And should some receive a very targeted Christmas present this year?

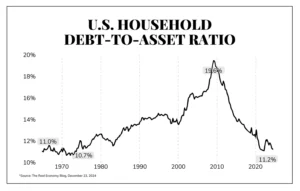

- We hear so much about debt increasing, and I am the first to sound that alarm on governmental debt. Household debt, though, has to be evaluated relative to income and relative to assets (and this should be intuitively obvious to anyone who believes Elon Musk is wealthier than a homeless person). Now, perhaps some of this is begging the question since the “asset” denominator in the equation features home prices and stock values that some may say are over-valued. But regardless, it is the numerator that gets so much attention, and the fact of the matter is that debt relative to assets has dropped precipitously in the last fifteen years. Those who sound the alarm of debt levels and do not share this additive nugget are guilty of lying by omission, in my humble opinion.

Top News Stories

- Congress reached a deal Friday to extend government funding through March, and President Biden signed it over the weekend. The deal included $100 billion of additional disaster relief spending and an extension for one year of the farm bill. The restrictions proposed against pharmacy benefit managers were taken out of the bill, as were many of the provisions in the initial deal rejected earlier last week.

- It does appear that Speaker of the House, Michael Johnson, enters 2025 in a very vulnerable position. If there were another clear candidate to replace him, it would almost be a done deal that House Republicans with only lukewarm support from the President-elect would replace him, but the one element offsetting his chance of removal is that no one else wants the job. I wonder why.

Public Policy

- President-elect Trump named Stephen Miran to chair his Council of Economic Advisors. Stephen is a friend of TBG, has been an informal advisor to me, and is an excellent choice in this extremely important role.

- The debt ceiling itself survived the latest government funding deal despite President Trump’s demands that it be eliminated, but that topic is setting up to be one of the interesting hot spots entering the new year. Some House Republicans are not likely to get rid of the longstanding, albeit ineffective, legislative device; the President-elect wants it gone, and in this tension, you may very well see challenges to implementing some of the Trump 2.0 agenda.

Economic Front

- The Fed’s preferred measure of inflation, the Personal Consumption Expenditures (PCE), rose just +0.1% on the month and moved up less than expected. Goods prices on the year have deflated by -0.4%. Energy has fallen -4% on the year and Food is up just +1.4% on the year.

- Private sector wages are up +5.7% on the year. Something tells me you’ll hear a lot more about this next year from some people and a lot less from others.

- Durable goods orders missed and were down -1.1% in November, much of it related to transportation. The silver lining was core capital goods shipments (which is what flows into GDP) were up 0.5% and ahead of expectations.

Housing & Mortgage

- Existing home sales did increase +4.8% in November, slightly above expectations and resulting in 6% year-over-year growth in volume. We remain a couple of million home sales per year below recent levels.

- As price appreciation has slowed, the current residential median price per square foot at $236 is now only marginally above where implied longer-term median trends would have it at $228.

Federal Reserve

- Futures are now pricing with almost no chance of a rate cut in January and a 50% chance of a rate cut in March. What is shocking in the Fed funds rate futures is that the odds of a Fed funds rate one year from now that is equal to or just a quarter point less than we have right now is over 50%!!

- In August, five-year inflation expectations were above 2.5%. Today, they sit at 2.2% – thirty basis points lower. The idea that inflation data is to the upside since the Fed began raising rates is, well, actually a lie.

Oil and Energy

- WTI Crude closed at $69.49 a barrel, slightly up +0.04%.

- Like the whole market, midstream got beat up last week, and like the whole market, midstream rebounded a bit on Friday. But the more detectable theme was in natural gas and natural gas adjacent investments. LNG export exposure appears to be a beneficiary with Trump 2.0, and pipeline projects that are natural gas-focused are drawing more market attention than crude oil pipes.

Against Doomsdayism

- Drug overdose deaths have declined 3% year-over-year (largest decline in 25 years). Traffic fatalities have declined eight quarters in a row. Even the adult obesity rate has declined over the last year (likely due to successful “big pharma” GLP endeavors). In every category, the mere existence of these things screams for more improvement and progress, but for a society obsessed with highlighting the negative data when it surfaces, it sure seems some honesty in reporting some improved data would be appropriate.

Ask TBG

| “I’ve long thought that the effects of QE since the great financial crisis must be having an inflationary effect on asset prices (not what CPI tracks). If that is the case, is there not a bullish case for stock and other asset prices now, despite the historically high valuations we are seeing? The way the Fed reacted to the COVID sell-off makes me suppose they will continue to inject liquidity in times of crisis.” ~ David N. |

| From 2009 to 2014, the Fed was doing quantitative easing (that is, adding to their balance sheet with the purchase of bonds), and markets were up a lot in that period. Of course, the Fed also had rates at 0% that whole period, as well, and of course, corporate profits were flying higher after the 2008-09 trough of earnings that came about in the financial crisis. So, all at once, you had corporate profits reflating, valuations lifting from trough levels, zero interest rates, and, yes, quantitative easing. It is hard to give QE all the credit for the increase in asset prices, but it can have some. But the Fed has been doing quantitative tightening, not easing, for the last two years, and markets are up ginormously (not a word). There are periods of QE in the last ten years where markets are down and periods of QT where markets are up. I certainly agree that if there were a crisis, the Fed would “inject liquidity,” but I do not believe adding to a balance sheet of $6.9 trillion has the same effect of adding to a balance sheet of $1 trillion. The law of diminishing returns is alive and well. The impact of QE was over-estimated in its first iterations post-GFC, which is not to say there was no impact, and the impact of non-QE has been over-estimated in the three times QE has been reversed since. |

On Deck

- With the Christmas holiday this week, there will be no client WPHR on Wednesday and no Dividend Cafe on Friday. There will be a Monday-edition Dividend Cafe next Monday, the 30th, and a Friday Dividend Cafe on January 3

- Next week I will be locked away working on my annual Year Behind, Year Ahead white paper, which will be published in the Friday, January 10, Dividend Cafe.

Merry Christmas, all. Peace and joy to you and yours.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.