Dear Valued Clients and Friends –

Things are moving very fast in the world and the markets, and not always with as much clarity as some may be hoping for. We try to break things down around the horn today, and maybe you’ll feel a little more clarity when done. Or maybe not.

Somebody wanted to argue with me about Nvidia today. I am a peacemaker, though. And a fun Fox Business segment from over the weekend in Maria’s Wall Street.

Dividend Cafe looked at the conflicting realities around political inflation and monetary inflation, and assessed what inflation expectations have done in the last few weeks, and why. It covered a few other nuggets, too, so check out the written version is here (our favorite), the video here, and the podcast here.

Off we go …

|

Subscribe on |

Market Action

- The market opened up, then came straight down, then back up, and fell in the final minutes of trading. On the other hand, the Nasdaq was pretty much down throughout the day besides the open.

- The Dow closed up +33 points (+0.08%), with the S&P 500 down -0.50% and the Nasdaq down a harsher -1.21%.

*CNBC, DJIA, Feb. 24, 2025

- It is way too early to know if it is true, or how true it is, that Microsoft is cancelling leases for some data center expansion. But the idea that many hyper-scalers may be down-ticking their AI capex in 2025 is gaining traction, and represents a much bigger paradigm shift for markets than people realize (if true).

- Nvidia releases their results this week (last of the Mag-7 to report), and the total guidance for 2025 Mag-7 names has seen the low end of the earnings range come lower, but the high end go higher. This could be interesting.

- The ten-year bond yield closed today at 4.40%, down two basis points on the day.

- Top-performing sector for the day: Health Care (+0.75%)

- Bottom-performing sector for the day: Technology (-1.43%)

- Just 60% of the S&P 500 names are trading above their 200-day moving average right now. With the Russell 2000, it is not even 50% …

- I talk a lot about the concentration U.S. investors have in U.S. stocks (that has been a very, very good thing for a very, very long time now) and, of course, the concentration U.S. investors now have in a handful of mega-cap tech companies (something that I have been well on record about in terms of the elevated risk it represents). Lost in the shuffle sometimes is the elevated concentration for U.S. stocks and U.S. tech stocks that NON-U.S. INVESTORS HAVE. It is somewhat surreal how much of the U.S.-centric portfolio dynamic is driven by foreign investors and the tech concentration (foreign investors want OUR big-cap companies, not theirs). This is, all at once, a good thing and a bad thing. The good part is it rationally speaks to the U.S. ability to generate capital flows into our country because of superior economic dynamism and innovation. The bad part is that foreign investors are no less human than domestic ones, and humans like to buy into euphoria and skip the part about discipline and logic. To this end, we work, provided you have a U.S. address. =)

Top News Stories

- Germany held its election yesterday, and the center-right, Friedrich Merz, is the new chancellor. The far-right party came in second place, and the social democrats came in a stunning third place. To say that building a coalition for the new party in charge is not going to be easy is like saying that uniting the warring factions of American politics will be a challenge for the Trump administration. It. Is. A. Mess.

- Dan Bongino has been named Deputy Director of the FBI

Public Policy

- The ability to thread the delicate needle needed to see one bill happen for budget reconciliation that passes tax reform with other agenda items will largely come down to the politically sensitive feat of selling House members on cuts to Medicaid. Reductions in these entitlement program increases are sensible and needed budget items, but the politics are not simple, and the math is nearly impossible without this on the front burner. The House Rules Committee has a key meeting on all this today.

- DOGE has advertised $55 billion of savings so far from their efforts, but an $8 billion savings turned out to be $8 million (silly typos). Government waste is hard to get rid of, even in a program that is all about, well, government waste. I am watching all of this for political, economic, and market sensitivity.

Housing & Mortgage

- Housing starts came in at 1.36 million in January (annualized, of course), below estimates by a tad and well below the December figure. Single-family starts, which is the number everyone should be paying attention to ex-multi fam, were below one million.

- Existing home sales were down -4.9% in January. The median sales price was down a bit on the month but is up 4.8% versus a year ago. The annual pace of activity at around 4 million is substantially below the 5.25 million pre-COVID pace and certainly below the insane 6.5 million pace during COVID.

- A normal market inventory (months it takes to sell existing inventory) would be 5.0. The supply is now up to 3.5, well below normal, but much better than the 1-2 it has been as more sellers adjust to current market reality.

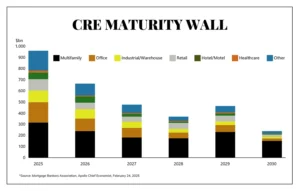

- Very few elements are more relevant to Fed rate thinking than this maturity wall in commercial real estate:

- The median age of all homebuyers is now 56 years old, a far cry from the age 31 when I was in Kindergarten. There are just way, way more people upgrading houses than there used to be, and way, way less first time homebuyers than there used to be. That latter metric means a higher average median age.

Federal Reserve

- The signaling of an end to $25 billion of tightening per month ($300 billion per year) is a big deal for monetary policy. Not only was it a key theme of ours this year, but it also gives the Treasury an assist as bank reserves look more plentiful when that can easily be reversed when the debt ceiling is soon lifted. Our friends at Strategas believe the official end of quantitative tightening is coming as soon as March (May at the latest) as the Fed seeks to assist liquidity, not drain it, in advance of a higher debt ceiling.

- Apart from the wonkiness of what I just said, which is important to financial markets, a further and more pedestrian takeaway is this: Ending QT allows the Fed to be easing monetary policy while displaying neutrality via a pause in touching the federal funds rate. We are basically at a 0% chance of a rate cut in March, just 28% in May, and up to 62% chance in June.

Oil and Energy

- WTI Crude closed at $70.91, up 0.72% on the day.

- We were very encouraged by what we saw across midstream earnings this quarter as a bottom-up assessment. The whole “space” can indicate one thing, but what really matters, ultimately, is how individual companies do and what individual companies are projecting (and for us, that means the individual companies we actually own). Macro factors can be a headwind or a tailwind for the whole industry for a prolonged period of time. Still, eventually, it will always come down to the free cash flow generation and individual outlook of actual companies – and these things are by-products of the decisions they make – acquisitions, capex commitments, balance sheet management, productivity, etc. Q1 reflected a solid quarter of results from Q4, and despite several years of huge performance, we see good things for our exposures continuing.

Ask TBG

| “What are TIF spreads? How are they measured? How do TIP spreads affect annual inflation expectations?” ~ Johnny H. |

| A TIP (Treasury Inflation-Protected Security) pays its coupon plus the annual CPI, so the spread between the yields of TIPS and Treasuries of the same maturity gives IMPLIED expectation for inflation (literally). |

On Deck

- The House’s actions on budget reconciliation are the biggest story in the days ahead.

- Pacifica Christian is playing in the CIF championship game on Saturday after a double-OT thriller win over powerhouse Corona Centennial on Friday night. Go Tritons!!!

Reach out with questions, and I will be with you this week in the daily blurb as there is plenty “on my mind.” …

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.