Dear Valued Clients and Friends –

Market turmoil continued today with the Nasdaq down -4% today and now down -13% from its Feb. 19 level of just over two weeks ago. There is so much in market commentary today and public policy discussion that I will just get into it without the need for much setup. The New York Times and CNN.com quoted me in their opening bell coverage of today’s market sell-off. But they just get a cliff note or two – you’ve come to the right place for the whole book, and we all know how much people like whole books more than cliff notes.

Dividend Cafe on Friday was devoted to the latest in the tariff saga, with a whole play-by-play of what has transpired, and a financial markets unpacking of what financial markets are indicating it means for economic growth. The written version is here (my favorite), the video is here, and the podcast is here.

I was on Varney/Fox Business this morning for the opening hour with a little recap reel here.

Off we go …

|

Subscribe on |

Market Action

- The market opened down -400 points and steadily dropped throughout the day, though it did bounce 300 points in the final 45 minutes from the day’s low of -1,200 points.

- The Dow closed down -890 points (-2.1%) with the S&P 500 down -2.7% and the Nasdaq down -4%

*CNBC, DJIA, March 10, 2025

- The heavy level of protection buying in the market (VIX calls and S&P puts) may be the most bullish indicator one can find (as a contrarian). Though a $28 price on the VIX is not screaming panic, it is ~50% higher than it was just three weeks ago and the volume has run through the roof, as it has for S&P 500 put buying.

- The S&P broke well below its 200-day moving average today. I share this despite the fact that I don’t think it means anything. Actually, I share it because others will share it like it means something, and so by me sharing it I then get the chance to say that “it doesn’t mean anything,” hence killing two birds with one stone.

- Bond yields fell across the board this morning, as every spot on the yield curve from two to thirty years was down 10-12 basis points.

- Besides dividend growth stocks in defensive sectors, perhaps the only thing that has done quite well in this market sell-off is “boring bonds” …

- The ten-year bond yield closed today at 4.21%, down ten basis points on the day.

- Top-performing sector for the day: Utilities (+1.04%) and Energy (+0.95%)

- Bottom-performing sector for the day: Technology (-4.34%)

- Credit spreads are the widest they have been in over six months, are still not that wide, but are pointing to more “economic” concerns in the present moment as opposed to mere “risk asset valuation” concerns

- Concerns that RFK would tank health care stocks and consumer staples seem to have been misguided. The two best performing sectors since he was confirmed at Health & Human Services are the two sectors he has said he is going after.

- One of the most embarrassing things I have heard in a long time: Bitcoin enthusiasts who believe it is an anti-government hedge, mad that bitcoin didn’t go up more, in the hope that the government would buy more bitcoin. Embarrassing, but also pretty funny, right? I got to talk about this disastrous idea of a governmental bitcoin strategic reserve on Fox Business today.

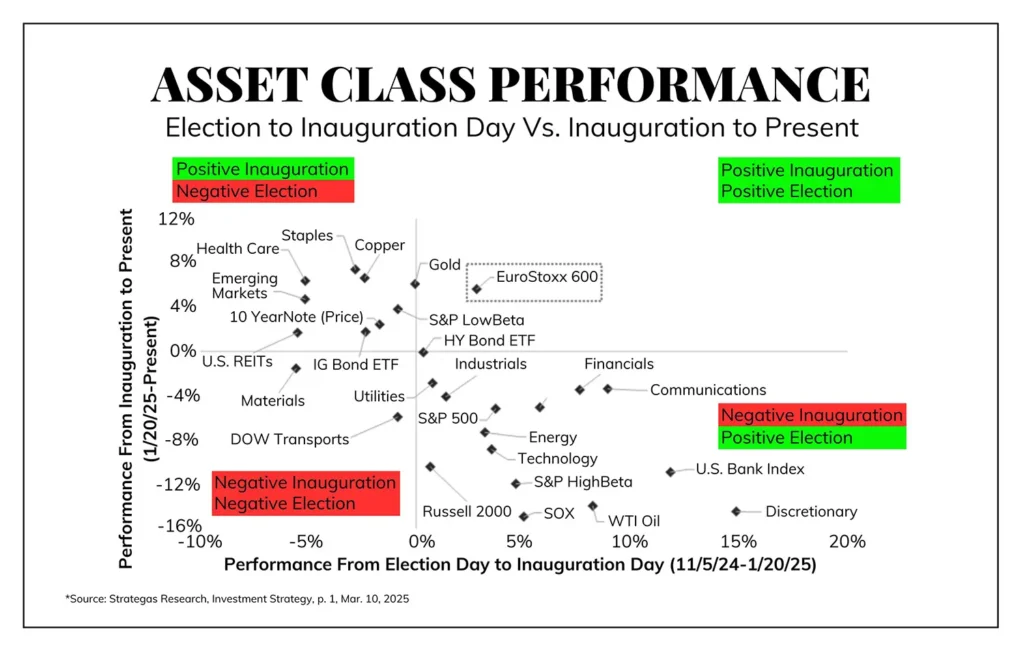

- This is one of the most interesting charts I have seen in quite a while. Healthcare and food/snack companies are leading the way since the new administration came in. Almost everything else is negative since the inauguration, and more and more sectors and asset classes have gone negative since the election itself. Note that this chart reflects action BEFORE today’s market day.

- An underrated element in recent market strain … Full-year 2025 earnings estimates have come down a tad (mostly from moderated Q1 and Q2 expectations) over this last quarter, and markets entered the year expecting higher than the +10.2% earnings growth now being projected. These downward revisions have been subtle, and may improve later in the year (or worsen), but when entering the year with such lofty valuations it should not be a surprise that markets have endured this added concern as they have.

- A little reminder for all stock investors, even those whose dividend growth portfolios have held up very well as of late: A drop in the market of 5-10% (which so far is what this is for S&P 500 investors) happens virtually every single year; A drop of 10-20% happens less but still is not at all uncommon; A drop of 20-30% is more or less a once-a-decade type affair.

Top News Stories

- I have argued for weeks that the big market and news story about tariffs and the big market and news story about the tax/budget plans are not totally separate stories – that the concerns around tariff impact become exacerbated in proportion to the concerns that a tax and budget reconciliation bill do not come together as previously envisioned. This week is a big week in the latter story, and dovetails with the already big developments in the former.

- The media will talk a lot about “shutdowns” (the headline in Politico this morning was “Shutdown week is here” – and then the key sentence in the article under that headline was “The expectation in D.C. is that a short-term funding bill will ultimately be passed.” So much journalism-ing. More on the funding and such in Public Policy below.

- Former Canadian central bank head, Mark Carney, was elected the new Prime Minister of Canada last night.

- Though not a lot is being released to the press, indications are that the U.S. and Ukraine through back channels since the famous meltdown in the Oval Office ten days ago have largely put the rare earth minerals deal back on track and are close to restoring the deal that fell apart over a week ago.

Public Policy

- Speaker Mike Johnson with the full support and prodding of the President has published a bill to fund government through September, avert “shutdown,” and try to keep critics of clean continuing resolutions in line. The bill cuts some spending, increases some, and gives more money for ICE deportations. It doesn’t touch Medicaid or Medicare. It will be politically hard for Republicans (and battleground state Democrats to not vote for it), and President Trump’s pleadings will make it very difficult for House Republicans to stand in the way.

- But remember, beyond the approval of a stopgap funding bill and some budget legislation, there is the tax bill itself that will eventually have to be reconciled to the budget. The House Ways and Means Committee met today to begin drafting the tax portion and ironically one of the first areas of contention: House REPUBLICANS (you read that right) demanding that clean energy tax credits from the Biden administration be preserved. You can’t make this stuff up.

- Commerce Secretary, Howard Lutnick, said on Meet the Press yesterday that:

“Yes, some products that are made foreign might be more expensive, but American products will get cheaper, and that’s the point.. … So will there be distortions? Of course, foreign goods may get a little more expensive, but American goods are going to get cheaper, and you’re going to be helping Americans by buying American.”

The comment is important because of what it does admit, and then what it does not address. On one hand, there is one of the first explicit admissions from the administration that “tariffs make things more expensive.” That would historically have been something every person who ever existed could have testified to, but it has been made fuzzy in recent years. That the administration’s Commerce Secretary said so is noteworthy. But of course, his claim is that American goods will get cheaper because the higher foreign tariffs will make them more competitive. This part confuses me, because I am not clear why American manufacturers will cut their prices when their foreign competitors are seeing their costs increase – though it would be awfully charitable of them! However, there is a more important point here implied but ignored in Secretary Lutnick’s comment: Apparently OTHER products that are made by Americans not competing with foreign manufacturers will get more expensive, for the exact same reason. In other words, American-made products exported to other countries which will be subject to retaliatory tariffs are going to get more expensive, and less competitive, for the exact same reason Secretary Lutnick himself said foreign goods will get more expensive. This point is being made by yours truly because the media, even in criticizing the administration’s tariff policy, seems unable to make it, and because it is not being addressed by the administration for obvious reasons. Tariffs have visible, and invisible effects. The impacted parties no one talks about are the American manufacturers who export goods already, and see their prices go up as innocent bystanders in the trade war that first starts trying to protect American importers.

- President Trump said yesterday that “tariffs will make you so rich, you’re not going to know where to spend all the money.” Okay, so first of all, I don’t know the shock and awe thing at his constant use of hyperbole. I take it as a given whether it is a time where I like it or a time I can’t stand it. But as for “Americans not knowing where to spend their money,” I just want to say that, yes, they will figure it out.

Economic Front

- The jobs report reflected 151,000 jobs in February, below expectations and marginally more support for a slightly weakening labor market. There were barely any revisions for the last two months. The unemployment rate ticked up to 4.1%.

- Hours worked at 34.1 (lowest level since 2010) and the labor participation rate down to 62.4% bother me, as well.

- Take it for what it is worth, but tax refunds are so far tracking +23% higher than they were a year ago. It is very early, but it seems noteworthy for those concerned the consumer is getting tight.

Housing & Mortgage

- I have now received no less than three reports from various homebuilders and even commercial developers that capital markets have re-opened in their space coming into 2025. Banks that would not lend on certain projects (multi-family construction most notably) have re-entered the space and are offering aggressive programs to finance new construction. Whether or not it is the modestly lower reference rates, or just tighter spreads, or simply enough time having run off the clock since many lenders went pencils down in the space, the volume of reports I have gotten about markets re-opening here indicates to me it is not merely anecdotal.

Federal Reserve

- The futures market is back to pricing in THREE rate cuts this year. It is not doing that because the Fed has said anything different. It is looking at data and saying, “yeah, they are not staying as hawkish as we thought.”

- The weaker economic data of the last week or so has futures market expectations for three additional rate cuts this year to over 75%, and now four rate cuts are priced to 39% probability (from near 0% a few weeks ago).

Oil and Energy

- WTI Crude closed at $65.96, down -1.6%

- Midstream Energy was down about -5% last week despite no real exposure to tariffs. “Risk off” sometimes includes energy, even midstream energy, and we find those opportunities to set up the most buyable possibilities.

Ask TBG

| “What do you mean when you refer to bitcoin as a ‘sociological’ investment?” ~ G.R. |

| My sociological claim is specific to the discussion of bitcoin as a medium of exchange. Speculating on the price of bitcoin is not relevant if one were only discussing bitcoin as a medium of exchange (no one has ever in the history of the world bought a dollar, or any other currency, and said, ‘I believe this unit of currency will be worth 2x what it is now.’ The bitcoin conversation suffers from a lack of focus and consistency, but it is explained by the sociological driver – intellectually incoherent as it may be. The desire to believe some medium of exchange and store of value that aggressively appreciates – all the while escaping the fiat money system that many inherently distrust – leads people to believe something (or actually three things) that can’t all be true at once, but which some very much want to be true – hence the term, sociological. |

On Deck

- I am in the TBG Palm Beach office Wed, Thurs, and Fri this week

- The Consumer Price Index for February comes out on Wednesday.

I don’t want to pile in on all the hysteria regarding where people love President Trump or where they can’t stand him. I call balls and strikes to the best of my ability here in the Dividend Cafe, where it comes to Presidential and policy ramifications on markets and the economy. As it pertains to my approach to this administration, I generally take bullets in equal measure from both sides, which in 2025 I wear as a badge of honor. But I will put down my criticism of tariffs for a moment, and put down my praise of energy policy and deregulation, just to say that … why, why, why, do we still have this absurd daylight savings change ?????

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.