Dear Valued Clients and Friends –

The first quarter of 2025 ended with a huge drop Friday followed by an intra-day reversal today. We’ll have all the quarterly recap action tomorrow (and clients will have it with detail to markets and TBG particulars in WPHR on Wednesday), but for now, let’s just say “operation chaos” at the White House is reigning supreme.

Speaking of which … Dividend Cafe on Friday looked deeper into the ambiguity of current tariff policy, and the ambiguity of what is to come (this week). The written version is here (my favorite), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

- The market opened down nearly -300 points today and almost immediately began a recovery that lasted throughout the day, with the market going into positive territory around 11am ET, and going up another notch around 2:00pm.

- The Dow closed up +418 points (+1%) with the S&P 500 up +0.55% and the Nasdaq down -0.14%

*CNBC, DJIA, March 31, 2025

- Today’s close means the Dow was only down -544 points (-1.3%) for Q1, the S&P 500 down -4.65%, and the Nasdaq down a more substantial -10.4%. The S&P is down -8.7% from its Feb. 18 high and the Nasdaq -13.9% from its Feb. high.

- The Nikkei was down over -4% today as Japanese markets join the global risk-off period largely centered in U.S. markets

- The ten-year bond yield closed today at 4.21%, down 4.4 basis points on the day and a full 36bps on the quarter, one of the best quarters for the long bond in a long time.

- Top-performing sector for the day: Consumer Staples (+1.63%)

- Bottom-performing sector for the day: Consumer Discretionary (-0.18%)

- For all the contrarian indicators one would want to see to indicate that the panic and drama and sell-off have gotten too extreme and a really cheap “buy” level is in place, the “put-call ratio” really has not surged that much. Seeing that follow other indicators would be more re-assuring. (see Glossary below)

Top News Stories

- A massive and tragic earthquake rocked Myanmar this weekend

- March Madness heads into the Final Four this weekend with all four #1 seeds winning their regions, only the second time in history this has happened (and first time in 17 years). One Managing Partner of a wealth management firm celebrating its ten-year anniversary this week apparently had all eight teams in the elite eight picked correctly in his bracket, and all four teams in the final four, and seems to have significant bragging rights throughout his bracket and with all those who doubted his college basketball knowledge. We are trying to make him available for more comment but he seems very focused on writing the rest of this Dividend Cafe right now.

Public Policy

- I thought Dr. Nordvig (former Head of Research at Bridgewater and a Ph.D economist I enjoy reading, even when is wrong captured the state of affairs well here. For those who want to skip the link, the key takeaway:

“Normally, when analyzing economic policy, you can do a mapping from economic pain into a policy response. But here we have a different causality, with economic pain generated directly from the policy itself, and it is not obvious when the pain will be so severe that there will be a policy response. This is a quite unique situation.”

- The court upheld the administration’s decisions to fire members of the National Labor Relations Board as well as the Merit Systems Protection Board. But they reversed some of the dismantling of the Consumer Financial Protection Bureau. Congress is directly taking on some of the CFPB stuff directly (imagine that!!), with the House Rules Committee set to vote later today on overturning various CFPB rules.

- The general rule of thumb with virtually no exceptions other than the post-9/11 election of 2002 is that the party in the White House gets “shellacked” in the midterms. Many have projected that the razor-thin lead the House GOP has now makes for an especially vulnerable House outcome in 2026, and I do not disagree. However, I was shocked to see that there are only three House Republicans right now in districts that Kamala Harris won in the 2024 Presidential election. In 2018 when President Trump saw the House significantly move to the Democrats, there were 23 seats filled by Republicans in districts Hillary Clinton had won. History and math still indicate that the Democrats are more likely than not to re-assert a House majority in 2026, but lots of electoral demographics make that less of a sure thing with less of an expected magnitude than past years.

- The average U.S. tariff rate on foreign goods is 2.7%. Canada’s average rate is 1.8%, Japan’s is 2%, and the EU’s is 2%. “Reciprocity” may not go the way we think.

Economic Front

- The areas in the economy that have to be monitored around tariffs are:

- Uncertainty (see Friday’s Dividend Cafe) undermining capital investment (and, to a lesser degree, consumer activity)

- Price pressures from tariffs that impact the overall price level (inflation)

- Cost pressures from tariffs that impact corporate profits

- Note what I did not say: That there is no possibility of any short-term beneficiary. Economics is the allocation of scarce resources, and in scarcity, there are trade-offs. There may be a winner, for a period, that we see. The issue is understanding what the trade-offs were, and these three above represent pretty big trade-offs

- This is your periodic reminder that exports have quadrupled over the last 35 years. The trade deficit has expanded because imports have grown at a faster clip than exports. But exports have not declined, they have substantially increased, by 400% no less.

Housing & Mortgage

- It is no secret that the Trump administration’s largest economic policy agenda items thus far have centered around trade and tariffs, and say that with a not insignificant amount of frustration. As I have suggested many times here in the Dividend Cafe, where tax reform fits beneath the tariff subject in their publicly-presented agenda is a big question, too. But one item that has not really appeared in any public forum that I have seen, but that I do believe is buried somewhere deep in their agenda, is the issue of Fannie and Freddie. In what I consider to be a rather embarrassing fact, these two mortgage behemoths remain under the conservatorship of the U.S. Treasury Department, nearly 17 years since the financial crisis and the Fannie/Freddie failure that preceded it. The companies turned into profitable enterprises again five years after the crisis, and the benefit of a government [explicit] guarantee became less relevant. Right now, the taxpayers have to inject fresh equity into Fannie/Freddie should they become troubled again, and I believe removing that taxpayer backstop and moving these companies into a full privatization solution (an extremely well-capitalized one!) is vitally important. Numerous proposals are floating around and Secretary Bessent has this matter on his agenda. I do not believe it is a subject that much animates President Trump, and with tariffs and tax reform at the top of everyone else’s list, I doubt you will hear much from anyone else about it. But the window for fixing all of this is the next three years, and I don’t intend to leave it alone.

Federal Reserve

- Odds moved this last week more towards more than less by year-end in terms of rate cuts, with a 70% chance of three or more cuts by December priced into the futures market, and a 35% chance of four or more.

Oil and Energy

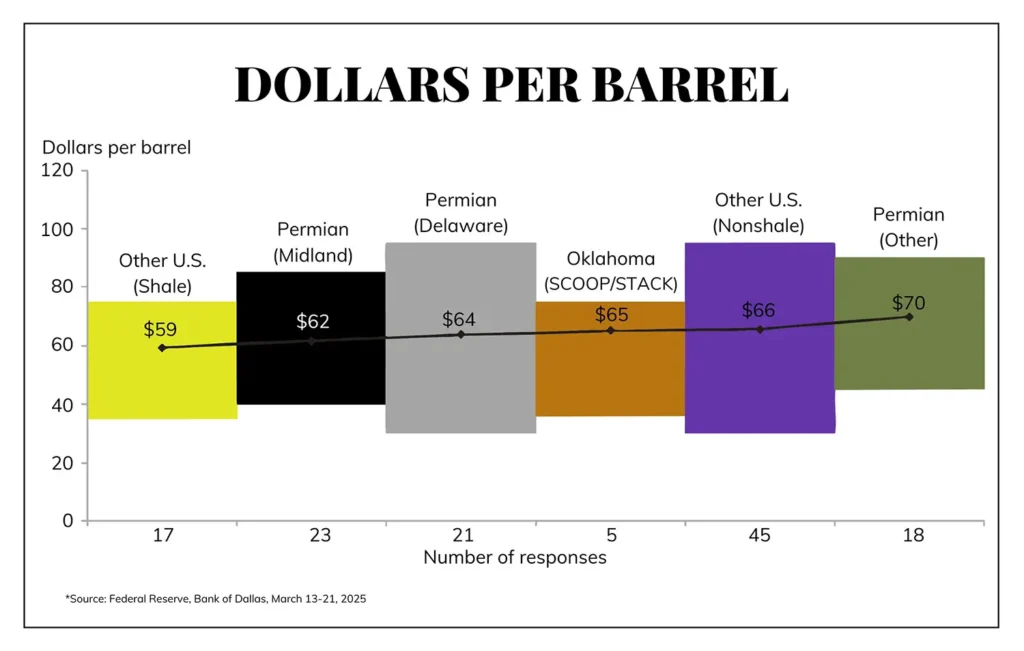

- WTI Crude closed at $71.40, pretty even on the day.

- Even as the S&P was hammered Friday and down -1.5% on the week, midstream was up a tad last week (about +20bps). MLPs, in particular, rallied over 1%.

- Peter Boockvar ran this chart today from the Dallas Fed on what the price of oil needs to be to lock in new wells for drilling (which is different than a breakeven level on current wells). All of this talk of “drill baby drill” bringing oil to $50 has apparently not been run up the flagpole at the, well, oil companies.

Glossary

- Put/Call ratio – Options or derivatives are contracts that investors can buy where certain numbers of shares can be delivered in the future at certain pre-set prices. A “put” is where an investor can SELL at a certain price (lower than it is now), and a “call” gives one the right to BUY at a certain price (higher than it is now). They can be used for hedging or for speculating, and they involve certain TIME constraints as to when these price movements must happen by. The “put-call” ratio is just a mathematical summary of total PUTS (contracts on prices going down) versus CALLS (contracts on prices going up).

Ask TBG

| “How does the Ricardian principle of comparative advantage work under a system of unequal tariffs? Wouldn’t world trade be more robust without any tariffs at all?” ~ Rod M. |

| As for the second question, the answer is “of course.” Countries would generate more trade opportunities (imports and exports) if they did not punish their own people with the imposition of tariffs. This certainly does not lead to a conclusion that the way to counter those countries who punish their own citizens with tariffs is to then punish our own citizens with tariffs, but to the heart of your question, I freely admit to being a purist here – I would love no tariffs at all.

But where we describe tariffs as “unequal” (and as is pointed out below, we have a higher total tariff rate on imported goods than Canada, Mexico, European Union, and Japan, so in this case “unequal” would mean them looking to tariff us more to make things more fair to them), I believe we next have to ask what we do when prices, barriers, and costs are “unequal” in any other aspect of a market economy. Do we believe those in a transaction should decide what to pay and not pay, or a third party actor who has power? If the latter – if a centralized, governmental force should adjudicate – doesn’t that have profound meaning for all aspects of the economy? And isn’t that concession what the 20th-century economic debate was about: governmental control of the economy versus a free and open one? |

On Deck

- A special quarterly version of the Weekly Portfolio Holdings Report summarizing Q1 will be in client inboxes on Wednesday morning.

- The Senate Parliamentarian may rule this week on the “current policy baseline” request of lawmakers (allowing what tax levels currently are to form deficit impact of new tax cuts and spending, not what they “were supposed to be if tax cuts expire.”) It is a monumentally important part of where tax reform is going.

Q1 is done. I am very pleased with how it went for our clients, given current uncertainty. Q2 is here. Markets never sleep. There is a lot of chaos right now. And to that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.