Dear Valued Clients and Friends,

Rebalancing is one of the least glamorous disciplines in investing – and one of the most essential. In this week’s Dividend Cafe, I make the case that portfolio rebalancing is not a mechanical afterthought or a concession to caution, but a deliberate act of risk management, humility, and behavioral discipline.

Because no asset, sector, or security stays in favor forever, the simple decision to rebalance becomes a powerful way to control risk, preserve investor discipline, and improve long-term outcomes – precisely because it refuses to chase what has merely been working.

Let’s jump in to the Dividend Cafe …

|

Subscribe on |

Pretty Soon, You’re Talking About Real Money

Our Investment Solutions department completed a “bookwide rebalance” this week, in which every account we manage across every client was rebalanced to the target asset allocation we created for each client. This means in many cases that the weighting of one portfolio category (for example, Core Dividend) is adjusted relative to another (for example, Boring Bonds). But it also means that within a portfolio category like Core Dividend, one security is re-sized relative to another (for example, a stock that had gone from 2.5% of the portfolio to 2.2% is bought back up to 2.5% while a security that had gone from 2.5% of the portfolio to 2.8% is trimmed back down to 2.5%). In all, our ~$9 billion business executed $1.2 billion of trades over a six-trading-day period, roughly $530 million in buy transactions and $630 million in sell transactions.

Besides my desire to brag about how efficient and successful a process my trading team pulled off, I bring this up in the Dividend Cafe this week to tee up what I believe is one of the most important topics in portfolio management: The art of the rebalance. It is stunning to me that 26 years into my career professionally managing money, I still encounter advisors who do not affect rebalances or investors who do not believe in them.

I will not bury the lede here: We do portfolio rebalancing at The Bahnsen Group because we do not know how a given asset class or a particular security will be in favor or out of favor next, so we consider rebalancing:

- A powerful risk mitigation tool

- A potential return enhancer

- An exercise in humility

We consider NOT rebalancing to be:

- A contempt for basic risk management

- An implicit belief that the momentum of what goes up is never interrupted by reality, or math

- An exercise in sanctimony (and if not intentionally so, implicitly so)

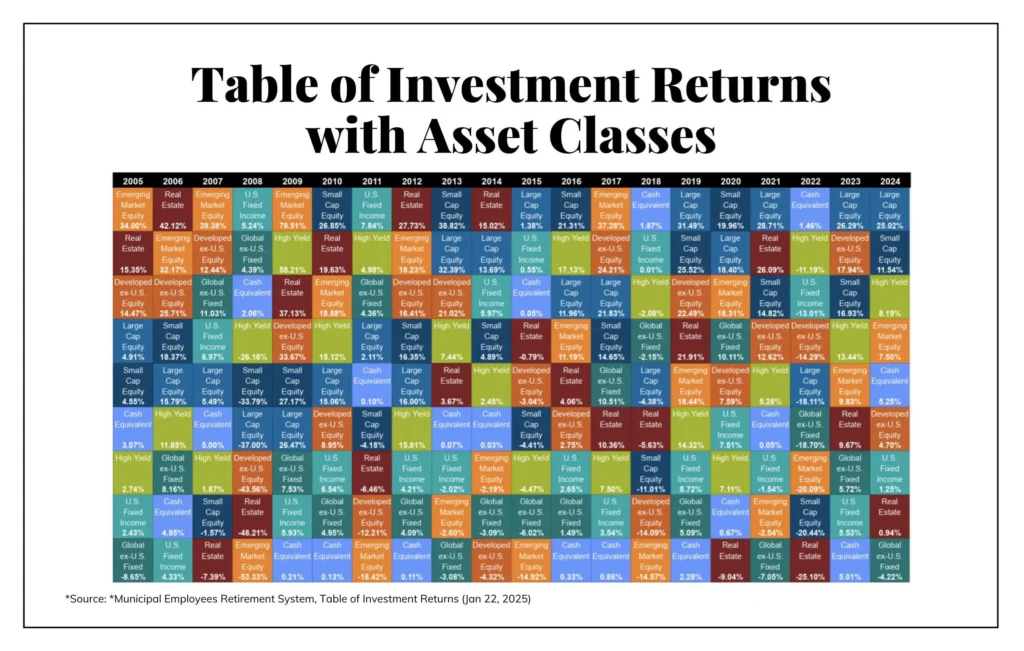

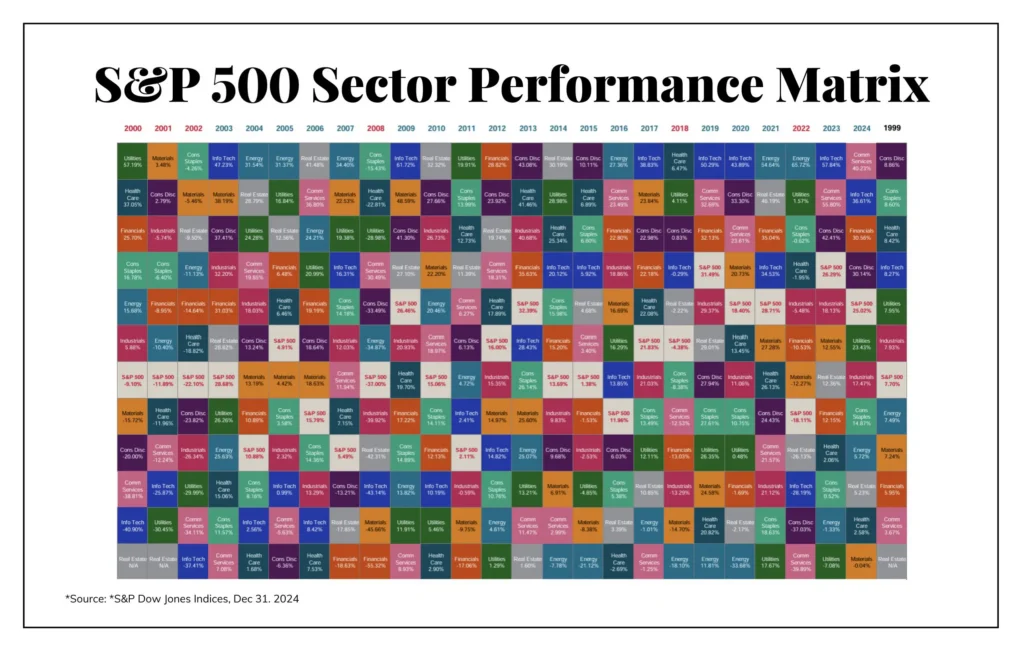

Colors of the Rainbow

I have been looking at periodic tables like this across asset classes, portfolio categories, and stock market sectors for my entire career. I have often felt that if one did not have the numbers (percentage returns) or the label of the sector or asset affixed, and just saw blank squares of different colors, it would still illustrate the underlying point quite powerfully. Indeed, one does not need to know the specifics of emerging markets or real estate to see that some asset classes are at or near the bottom (plenty), and at or near the top (plenty). That a high-performing asset is up over 18% in five of the last six years, for example, might mean that it now owns real estate at the top of this table forever and ever (most large cap growth investors seem to implicitly believe that), or the history of things might suggest, “no, that isn’t how it really works.”

Likewise, within market sectors, the sheer patchwork of color variety paints the story well enough: Leadership changes within the market. Timing what sector will do what and when is a fool’s errand. Rebalancing simply acknowledges the inevitability of these color shifts in a non-emotional and systematic way.

When you look at how Technology and Communication Services did from 2000-2006 can you imagine how much better investors who rebalanced from 1995-1999 did versus those who didn’t? Can you see how tempting it is not to rebalance when something looks permanently affixed to the top, yet how wise it would have been to do so before the inevitable happens? When you see how many are top (or near top) for a couple of years, then bottom (or near bottom) for a couple of years after that, can you see how rebalancing builds in tools to limit downside and also capture upside?

Math for People Who Hate Math

The argument that rebalancing interrupts great performers from delivering great returns is incoherent. Pretend you have an asset class or sector that will be +20% for five years in a row, and you want it weighted to be 20% of your portfolio. If you do not rebalance, that compounded return (on that part of your portfolio) will be higher. If you do rebalance, then 20% of your portfolio still went up 20% each year for five years. You did not sacrifice exposure. You did not give up big gains. You just traded away SOME of the excess gain, and what you got in exchange was risk mitigation from a very high probability event – that some correction or reversal would come about along the way.

You Didn’t Change, I Changed

The 20% weighting was created to reflect a certain risk/reward trade-off that was appropriate for a particular investor. Big gains (a good thing) could result in an asset that was weighted at 20% now representing 30% of the portfolio. But if the risk/reward propriety was 20% a few years ago, why is 30% appropriate now? What changed? Did your goals change? Did the comfort level change? Did the volatility expectations change? What happened to dramatically skew the desired risk/reward characteristics of the portfolio?

The investor did not change. The portfolio changed. And all a portfolio rebalance does is marginally resize things in the portfolio to maintain the portfolio construction deemed appropriate for an investor.

If a portfolio rebalance is not needed after substantial variance from the initial weightings, it can only mean that the initial portfolio was not well constructed. It either lacked thoughtfulness, accuracy, or intentionality – but either way, it is a terminable offense.

And if the portfolio was constructed well, has subsequently varied in a significant way, and yet a rebalance is a bad idea, it must mean either that the investor has had some substantive change in their own life and goals (maybe they got younger?), or, and here is where people just have to be honest with themselves, someone has decided that what just got done going up is most likely to continue going up.

And that determination is one of the dumbest things investors can ever, ever believe (let alone act upon).

Behavioral Management 101

The entire art of asset allocation comes down to optimally finding a blend of portfolio categories (asset classes) that meets the needs of a particular investor across financial goals and individual temperament. Our practice does not care for “style box” investing (for a lot of reasons), so we created various custom categories that serve as building blocks for all of our client portfolios. This portfolio construction process involves reaching an income goal, and a tax efficiency, and a liquidity preservation, and so forth and so on, for each individual client (hence the reason it can only be done on a custom basis, and throwing each client into one of three buckets is malpractice). But asset allocation transcends cash flow achievement, and it clearly is not about maximizing the return. If it were merely about maximizing the return, one should put 100% of their portfolio into the asset class with the highest expected rate of return, period. If Asset A is expected to return 10% and Asset B is expected to return 5%, whatever goes into Asset B is taking away from the total return of the portfolio relative to what Asset A would deliver. (Let me know if you need me to do the math a second time.) The reasons people include Asset B (or C, D, and E) is not to optimize the return – it is because of human behavior. Asset B is there to smooth the return of Assets A and B together in such a way that it makes the investor more likely to achieve the bulk of the return from Asset A by not scaring the investor out of the portfolio when inevitable volatility comes.

Now, in our building blocks of a portfolio, there are diversification benefits, liquidity vs. illiquidity considerations, and timeline considerations, so I do not want to oversimplify things. But the basic reality is that I would be perfectly content to let every client’s portfolio be 100% Dividend Growth, to the extent there was no such thing as human psychology, emotional response considerations, comfort levels, and yes, timelines. I believe Dividend Growth to be the optimal asset class (portfolio category) for growth, for income, and for growth of income. I do not fear a mathematical implosion that becomes irreversible. It represents a size, scale, liquidity, tax efficiency, and big picture solution set that I consider optimal. Yet we do not allocate 100% to Dividend Growth because there are other considerations beyond the portfolio’s abstract characteristics over a very long time horizon.

- No one can benefit from equities they do not own.

- Most people will not own equities if their downside volatility causes them to jump off the boat.

- We capture more upside of such volatile risk assets by minimizing those who jump off the boat.

- We minimize boat-jumping through thoughtful asset allocation.

- We maintain thoughtful asset allocation with annual rebalancing.

But Even If …

But the above paragraph is in the context of categories of portfolio (asset classes) and not particulars of a category (individual securities). Even if one were 100% allocated to Dividend Growth, the best-performing stock in a given year might be up a lot, and the worst-performing down, and rebalancing allows the non-emotional and systematic process of trimming the winners and buying more of the losers to play out. The same logic for rebalancing an entire asset allocation applies: Not rebalancing builds higher concentrations, increases exposure to risk and volatility, and allows drift to take place. Rebalancing the stocks within a thoughtful portfolio to their desired weighting gives us intentional management over the risk.

Risk Not Return, But Return Also

I believe that rebalancing does enhance return for a client portfolio over time, but not in the way many think. I do not believe it necessarily alters the total return of a blended portfolio. Sure, selling stocks that went from 60% to 80% in 1999 back down to 60% of the portfolio would have added to the return relative to going into the year 2000 with an 80% weighting instead of a 60% portfolio. But of course, if the reason to rebalance was a constant fear of a dramatic bear market, one could always just be uninvested. That doesn’t make a lot of sense. The reason I believe the return is enhanced is that the portfolio maintains a semblance of comfort level for the investor suitable to their “sleep” needs, and therefore decreases the likelihood of behavioral decisions in tough times that undermine returns.

And I believe that when good companies are added to after an out-of-favor period, it adds to the return of that investment. This. Is. Because. Of. Math.

The counter-argument is, “But what if that investment is not a good investment?”

But then one is not arguing with rebalancing; they are arguing with security selection. That is a different topic. Oh, and I should add, it is an argument about security selection rooted in the rearview mirror argument, which is not a good argument.

The Tax Argument

Many who oppose rebalancing say they oppose it on the basis of the realized gains such “trimming” represents along the way. There are, of course, some people who intend to die with their assets and never pay any tax. So first of all, this argument would not work for irrevocable trusts, IRA’s, 401’s, or any non-taxable account (or non-step-up account) in which assets are held. But for taxable accounts, it is my belief that the minimal, slight, marginal realized tax consequence of rebalancing is a feature, not a bug. Modest trimming along the way of a highly appreciated position limits the tax hit and consequence whereas the complete, uninhibited tax realization of an untrimmed position is (a) Much more severe, (b) Much more consequential (bracket creep and the like), and the real whammy (c) Much more distortive to behavior, because it keeps people from doing what they otherwise would do. Breaking up that consequence marginally over time limits the distortion effect of future decisions.

That said, it is all a red herring to the fundamental reason for rebalancing: realigning the portfolio with the risk/reward characteristics optimal for a given investor and their particular goals.

Conclusion

- It is very emotionally satisfying for investors to want to overweight “what has been working.”

- It is very emotionally troublesome for investors to “add exposure to what has not been” (or to what has been working “less so”)

- It can also be very expensive to add to what has been working, and very opportunistic to add to what has not been.

Investors’ humanity is why rebalancing is so fantastic. It eliminates emotion and establishes rules and guidelines that facilitate better outcomes for investors and a smoother path to achieving their goals. And across the board, these are all ends to which we work.

Quote of the Week

“Supremely rational investors take the further step of acting against consensus, rebalancing to long-term portfolio targets by buying the out-of-favor and selling the in-vogue.”

~ David Swensen

* * *

It brings me great joy to keep a Dividend Cafe within my targeted word count. I believe I pull that off somewhere around 3x per year. But I do hope the message got through this week, and of course, we welcome your questions any time.

Portfolio construction is a serious task for us. Maintaining the right portfolio and affecting the right adjustments as needed is our fiduciary duty. Of all the decisions we have to make throughout the year, managing what is currently $9 billion, no decision is easier than the one to rebalance. We are just not arrogant enough for it not to be.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet