Dear Valued Clients and Friends,

It has been a whirlwind of a week here in New York City, where the weather has turned crisp, beautiful blue sky autumn, and where the discussions among money managers right now are as heated and differentiated as I have seen in 25 years. It was an intellectually stimulating week, to say the least, and I am going to give you a very concise summary of a few themes and takeaways in this week’s Dividend Cafe.

That’s right – concise … You’re welcome.

Some of the major takeaways, provocations, questions, focuses, etc. that this week generated necessitate more time than I have had to process so far. And several really warrant their own stand-alone Dividend Cafe (and are going to get exactly that in the weeks to come) … But today I just want to provide a high-level overview of some of the major themes, takeaways, and debates that I came away with from the week. A very granular, long-form deliverable will be created summarizing my notes from the week (20+ pages) and available upon request. But for the rest of you, jump on into the Dividend Cafe for a few considerations that The Bahnsen Group’s 20th annual money manager week in NYC has generated!

|

Subscribe on |

For the Newcomers

I suppose a little context is in order for those who are not clients, or even for newer clients who may not be familiar with the backstory here. In a nutshell, in 2006, I was managing $100 million at UBS, and decided to try calling some of the portfolio managers I was then allocating money to, to see if they would meet with me in person. Some said yes, some said no, but I made the trip and combined it with several client meetings, essentially beginning what would become an annual tradition.

In 2008, the annual week of meetings became substantially important in my life, our money management process, and the direction of our business. I was literally in the city in the immediate aftermath of the week(s) that shook Wall Street to its core, and by then was in a more prominent position at a more prominent firm (Morgan Stanley). I would walk from one meeting to another, and sometimes major Wall Street banks had new owners by the time I got to the next meeting. Some of the hedge funds I was meeting with were deeply involved in significant exposures at the heart of the GFC (either exposed in a really good way, or a really bad way … one of these firms ended up being prominently featured in the hit movie, The Big Short, years later). It was as dramatic a week as I have ever experienced professionally, but it catalyzed an intense period of intellectual and ideological development for me. My intense interest in how credit markets worked was born out of that period and the systemic crisis of 2008, and I do not believe many dividend growth money managers care about credit markets as much as I do.

Well, all that to say, from 2009 through 2014, these trips were unbelievably life-changing. Our business was growing significantly, and I was developing more and more relationships with substantial traditional and alternative managers. Each year, the trip turned into an opportunity not only for due diligence on managers but also for internal scrutiny over our own decisions and positioning. I was a Managing Director at Morgan Stanley throughout these years, and I will never, ever forget some of the meetings and lessons learned during that period.

Since 2015, we have done this trip every year as our own firm. Brian Szytel began joining me before we left Morgan Stanley, and we are now meeting with managers as a multi-billion-dollar organization with deep skin in the game in high-conviction strategies. The meetings continue to be a major contribution to our portfolio management process, and they often result in various shifts or adjustments to strategy particulars. This year is no exception.

So that is the historical context in four short paragraphs …

What Does it Really Do?

I became a bi-coastal resident of New York City in 2017, so it can no longer be said that these money manager trips were an excuse to go to the greatest restaurants in America (or at least eat an edible bite of pasta, versus the available options in my other coastal residence). The trips are essentially a few things rolled into one:

- Yes, standard due diligence and monitoring across managers we already have capital with, but also …

- A chance to hear the macro perspective of managers outside their own lane and asset class. I love hearing bond managers talk about bonds or real estate managers talk about real estate, but far more interesting is often bond managers talking about labor, or real estate managers talk about interest rates, or small-cap growth managers talk about AI, etc. And because some of our major relationships are with alternative asset management firms that oversee hundreds of billions of dollars, there is intellectual capital across the multi-sleeves of their own shop that represents valuable information and perspective for us.

- The trip becomes almost a “retreat” for enhanced focus and contemplation on the markets, the economy, and our portfolio strategy. We find ourselves in a mindset of introspection that allows us to consider decisions, opportunities, and ideas with enhanced focus. Brian, Kenny, and I, sitting down together between meetings or over dinner at the end of the day to download and debrief, is almost as valuable as the meetings themselves.

- It gives us an enhanced view of how capital markets really work on the street – seeing the trading floors, meeting with executives of large firms, portfolio managers of many-sized firms, talking with a total candor that could never make a public-facing document. If the sales team of a large company hosts us with 30 other financial professionals for a “show and tell” event, we learn absolutely nothing about the organization and its people. It is too polished and too curated. But when we are getting this more intimate, one-on-one access, we can ask really hard questions, debate in a vigorous way, and just generally be edified around the processes and machinations of capital markets at work. It is among the most fun things a person can experience.

Now For the Fun Part

This year’s meetings included portfolio managers, hedge funds, and the like in the following asset classes:

- “Boring Bonds” (taxable) – our internal nomenclature for traditional investment-grade taxable fixed income

- Floating Rate Bank Loans

- High-Yield Bonds

- Mortgage Securities (agency)

- Commercial Real Estate

- Private Equity

- Private Credit

- Infrastructure

- Venture Capital

- “Boring Bond” (tax-free)

- High Yield (tax-free)

- Commercial real estate debt

- Middle Markets Lending

- Structured Credit / Asset-Backed Securities

- Small/Mid Cap Growth

- Emerging Markets Equity

- Midstream Energy

- Non-agency mortgage

Several of these asset classes involved meetings with multiple managers, and at least one meeting took place, focusing on each asset class on this list.

Some Major Takeaways

- The AI debate is intense and unresolved.

I can’t even begin to tell you how wide the chasm is between the “AI is the biggest revolution of all time and all any investor needs to do is close their eyes and buy buy buy” camp – and then the “AI is going to set more money on fire than anything we have seen MySpace, Peloton, AOL, and Pets.com rolled into one.” This was an incredible debate throughout the week, with billionaires, with geniuses, and with people of substance. And I am here to tell you – no one knows. There is a very extensive Dividend Cafe coming on the subject in the weeks ahead, but I was utterly flummoxed the last few days by the ferocity of the debate – sometimes with substance behind it, and sometimes, not. - The talk about “private markets” as monolithic is ignorant.

There is increasing public dialogue about the “dangers” of private market investments becoming more democratized. There is a consensus questioning the wisdom of such huge new inflows into private credit. There is vast curiosity about how realizations are going to happen at the pace L’s want in private equity (i.e., companies getting sold so investors can get their money back). - This may be the least conviction on the state of the economy I have ever, ever seen from various economic minds and wizards.

Yes, many believe it is weak and vulnerable, but that camp is highly open to various upside surprises. And yes, many believe it is strong and going to get stronger, but that camp is uncertain about a variety of economic issues. From my own questioning about where tariffs will undermine foreign capital flows in tension with the possibility of enhanced Foreign Direct Investment, to the optimism around AI efficiency versus fears of labor deterioration, to wonders about tariff impact to hopes for onshoring and productivity … there is absolutely no consensus in various economic tug-of-war, push-pull, bull-bear debates. - Spreads are tight everywhere, but yields are good everywhere, and when door A is closed, door B becomes the focus.

If I had a nickel for how many managers who swim in a spread asset class said this week that, “yes, spreads are really tight, but the all-in yield is still great …” I would have at least six nickels, maybe more. Look, their point is absolutely legitimate, but it 1,000% speaks to the shifting risk-reward dynamic. Spreads reflect risk and are supposed to provide an opportunity for that risk relative to something risk-free. When yields are decent, the asset class feels fine because investors like the coupons they are clipping. But, but, but … spreads always and forever reflect something. And one of the sources of return on spread product, besides current yield, is tightening spreads. When spreads widen (if??), that takes away from total return. We have no problem acknowledging attractive all-in yields despite tight spreads, but our weightings have to reflect the different risk-reward dynamics – period. - There is more interconnectedness with the data center theme than anyone realizes.

It is so easy to think of AI as an Nvidia story, and Nvidia as an AI story, and data centers as something needed to drive AI growth, rinse and repeat … But in the weeds of all this, from real estate to power demand to electricity production to natural gas to pipelines to interest rates to private asset managers to a host of adjacent (and non-adjacent) sectors also brought in to this story, the “data center” story is one that has many, many players. There are some aspects of this that are doomed to fail. There are some that will succeed but are vastly overpriced. And there are other elements that will win, and win big, and are not on the radar.

Conclusion

I have some strong opinions on all of this, and I will share a lot more in the weeks ahead – about the nature of the stock market right now, about the impact of indexing, about what AI will do (and will not do) to the jobs market, about the AI hype, about the risks in private markets – and I look forward to multiple Dividend Cafe editions on these topics individually.

For clients, we have some adjustments coming that are more specific to particular strategies and product dynamics – not necessarily any kind of shifting macro worldview. We will be unpacking that for you, as always, in the weekly portfolio holdings reports (that are for you alone).

And for everyone, enjoy your weekends. If wherever you are is as beautiful as New York City is right now, I have no doubt you will.

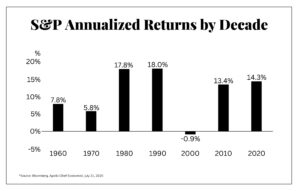

Chart of the Week

The market has averaged ~10% per year for about a century. But you know what it has NEVER done in a calendar decade? A return per year of 8%, 9%, 10%, 11%, or 12%. The average return can be well above or well below its mean, and in fact usually is, for a decade at a time.

Quote of the Week

“The loudest one in the room is the weakest one in the room.”

~ Frank Lucas

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet