Dear Valued Clients and Friends –

One of my favorite books about the 2008 financial crisis (I read over 75 of them, and wrote one myself) was David Wessel’s In Fed We Trust. The title may have been too sacrilegious, but his point on the role(s) the Fed played post-crisis (for good and for bad) was astute and well-written. Books will begin appearing in a few months about the 2020 COVID crisis (I will not be writing one), and one of those books will inevitably be to COVID what Wessel’s book was to the financial crisis – a look at how the Fed became the star of the COVID era (for good or for bad).

I don’t do predictions for a living, but you can write that one down.

I have covered the Fed on a daily basis throughout the crisis, developed relationships with Fed economists and staffers, and generally sought as much understanding as I can about what the short term and long term implications of Fed COVID actions will be. Prior to COVID, the Fed’s post-crisis role changed much of my long-term views about the U.S. economy, and certainly what the relationship between our country’s economy and her central bank will be.

I am understanding of much of what the Fed has done and will do, and I am critical of much of it. But what I will never be, is one of those investment advisors who takes what he or she doesn’t like about the Fed, and then invests client capital around what he or she wishes were the case, versus what is. In other words, investing must be based on what is, not what ought to be, or what one believes ought to be. This is never more true than when the activities of the Federal Reserve get applied to our portfolio management.

So yes, this week featured a NBA protest (for one whole day), a Republican National Convention, and another week of COVID progress. But it also featured a further settlement of the role the Federal Reserve will play in your portfolio for the decade ahead (and frankly, much longer). If one had to pick between guessing how big tech will perform in the next 15 days, or understanding what Fed policy will mean to your portfolio for the next 15 years, I strongly recommend the latter.

In this week’s Dividend Cafe we will:

- Review the week that was in markets

- Really spend the time we need looking at what the Fed has done, will do, and will never, ever do

- Provide five key investment implications to the monetary regime we now live in

- Do a “Euro”pean history lesson for you, and look at what that means for investors now

- Provide an explanation of how business investment works, what the hold-up has been, and why it matters

- Politics and Money – a look at this week’s Republican convention

- Chart of the Week

Let’s jump in, to the Dividend Cafe!

Market Redux

Into Friday morning trading the market is up ~650 points on the week. Day by day volatility has not been high, but disconnection between the Dow and the S&P and Nasdaq is growing. The yield curve reached its steepest level in two months (still just ~50 basis points between the 2-year and 10-year). Oil stayed about flat on the week. We are vacillating between days where the same big tech names lead the way and days where a new leadership group wants to take over. That story will get settled in due time.

Fed’s New New Normal Same as the Old New Normal

I wrote in the COVID & Markets missive the day the Fed “policy change” came out that re-structuring how inflation is calculated (a 2% target vs. a target a “2% average”) would not help them with their real underlying problem – that they simply can’t get inflation by pushing on a string! I do not agree with those who have stated that “this is a new formal milestone” – though I appreciate any attempt to add melodrama to central banking. What the Fed did was say that they are going to “really, really try” to do something they have been “really trying” to do for 12 years. And that is – counteract the disinflationary forces set off by excessive debt.

Tell us what you really think

First, let me tell you what I actually think about this, which has nothing to do with what I expect, how I need to position client portfolios, and what the impact will be. I am switching gears for one second from the “descriptive” (what is, and what matters) to the “prescriptive” (what ought to be, at least from my personal perspective). I do not believe an institution chartered with ensuring sound money should be “targeting” any kind of inflation, let alone explicitly stating that past inflation levels are remotely pertinent to future inflation levels. And once you decide past inflation can be a factor in our aspiration for future inflation, what time period for the “past” are you going to use? The “average” of inflation depends on the starting point, and will always, on average, be above or below your “average target” based on where you arbitrarily start your measurement. This is just so obvious, and so silly.

Who’s fault is it, anyway?

But besides the fact that I do not want fluctuating inflation levels and prefer a sound and stable price signal as a cornerstone to economic growth, I also do not blame the Federal Reserve for the conditions that lead them to this policy decision. Inflation is the desired tool of governments to negate the impact of excessive debt. If they can borrow $100 and pay it back with $100 that is only worth $50, that is a pretty good deal for them. The Fed is trying to manage the impact to economic growth, employment, cost of servicing the debt, the crowding-out effect, and so many other dynamics that build up when self-reinforcing dis-inflationary forces take over the world. Inflation or the desire for it is always and forever politically driven, and most of what is politically driven is desired by the people (higher home prices have been the great desire of American society for decades – a specific inflationary policy aspiration if there ever was one).

Well what does it mean?

It means the Fed will favor very low interest rates and very high availability of credit and liquidity for a long, long time. So back to the old new normal – does this sound any different than it has since March? Does it sound any different than it has since 2008 (besides one brief period of tightening in 2018)? No, because it isn’t. Here are five portfolio implications I would present:

(1) If you believe there will eventually be higher consumer prices as the Fed carries out its desire to explicitly create higher consumer prices, you would be wise to be invested in companies that have pricing power – the ability to pass on the impact of that inflation to their customers (so as to not hurt profit margins). Strong consumer staple companies are a great example.

(2) If you intend to have money in the bond market, you have to understand that rates are going to be low for a very long time. That means to get a return, you will need to take credit risk, which is a very different thing from interest rate and duration risk. In fact, they are so different, The Bahnsen Group is re-organizing our entire portfolio construction process around “Credit” and “Bonds that Act Like Bonds” as two entirely different asset classes. Cash, money markets, CD’s, treasuries – safe, “parking lot” vehicles – will offer a negative real return for many years to come.

(3) Asset price inflation and consumer price inflation have been two categorically different things for over a decade and will stay two categorically different things for over a decade (see below).

(4) High dollar-denominated debt and a strong U.S. dollar with a U.S. central bank running slightly tighter than most EM central banks (or other DM central banks) has been a headwind for emerging markets investors for roughly seven years. The reversal of all those conditions will likely mean the formation of a tailwind for emerging markets.

(5) No equity-centric portfolio can go without hedges, diversifiers, and volatility-mitigators. But in this period of easy money and zero interest rates, the traditional role of bonds that act like bonds is changing. The use of truly non-correlated alternatives to diversify portfolios will become a major “new monetary regime” reality – not because we now face equity turmoil, per se, but because bonds aren’t going to cut it.

Trying my best to make it understandable

I know some of these things are heavy, but I just don’t know how else to articulate them than the way I am. The Fed’s higher inflation is in asset prices, because all it can do (with QE and such) is create more and more reserves that find their way into risk assets, securities markets, credit, etc. And yes, all of that does serve as a misallocation of capital eventually, and a distortion of real risk. For the real economy to get the inflation the Fed wants, banks have to create deposits through lending – money gets lent out by the bank, then deposited for use, then circulated in the economy, and with those higher deposits, more lending is done, rinse and repeat. That is velocity of money, and that would create inflation. The missing domino? Demand for more loans. The Fed can put as many widgets in the corner as they want; they can’t make people want them.

Cash Call

A lot of attention was properly put on the fact that money market balances reached an astronomical $4.8 trillion in mid-May at the peak of the COVID lockdown era, an increase of over $1.15 trillion from where money market balances started the year. I made the point then, though, that while that was a huge level of sideline cash, and it did match 2008/9 financial crisis levels of sideline cash in absolute dollar numbers, as a percentage of market capitalization, it was actually much smaller than the financial crisis levels (i.e. $4 trillion of dry powder alongside a $35 trillion stock market is much different than $4 trillion of dry powder alongside an $11 trillion stock market, for reasons I hope do not require much explanation).

$234 billion has come off money market balances since mid-May, bringing money market levels “down” to $4.55 trillion, still high, but still not as high as it may seem as a % of total capital stock in the universe.

“Euro”pean History 101

As my son awaits the beginning of his sophomore year of high school, and the European History course he will soon take, I thought it might be useful for you all to take a trip down memory lane regarding the Euro currency, and where it has gone before getting to the place at which it currently is.

There had been a constituency in the European Union for decades that had wanted to see a shared currency across European countries, but the idea did not have broader support until the late 1980’s, and even then until German reunification became a real possibility. After the liberalizing events of the late 80’s and early 90’s, European authorities moved forward with the idea and discussion, though it was clear from the outset that the United Kingdom would not be on board. In all of the preparatory years before the 1999 launch of the Euro currency, there was an almost obsessive focus on fiscal discipline from member countries (strict caps on budget deficits, limits on debt/GDP ratios, limits on inflation, etc.).

The currency launched at the beginning of 1999, and essentially launched with an exchange rate to the dollar of $1.18. Some of you may find it fascinating to note that the exchange rate right now is, well, $1.18. But that is hardly a mark of exchange stability, as we shall soon see.

By the end of its launch year, the Euro had dropped all the way to parity with the U.S. dollar, and by late 2001 the Euro had dropped to roughly $0.81 cents to the dollar (the all-time low). The next few years would see a violent bounce in the Euro, and a violent drop in the U.S. dollar, and the Euro would reach $1.59 to the U.S. dollar by the middle of 2008 (it basically doubled in its value to the dollar from the beginning to the end of the George W. Bush presidency).

That mid-2008 high (and really much of the 2000’s action) had as much to do with a weak dollar as anything, particularly at the onset of the U.S. mortgage crisis in 2008. But when the financial crisis became a truly global affair, it was the dollar people jumped into, and the Euro they largely abandoned.

While the U.S. worked its way out of the crisis in 2009 and 2010, Europe began to reveal hers. Greece was insolvent (and then some), and a debt fiasco in Ireland, Portugal, Spain, and Italy piled on to the problems, and led to questions about the Euro’s existential fate. Various bailouts and liquidity operations kept things afloat for a year or two, but it was the historical “whatever it takes” moment of 2012 where Mario Draghi committed to unlimited actions to support European country operations.

2012 marked the moment where we knew the ECB would do whatever they felt needed to be done to support the Euro, but things did not get better for the fiscal health of member countries (most notably Italy and Spain) in the years ahead. Quantitative easing became the new normal, with a couple trillion of Euro added to the ECB balance sheet in 2015 and beyond. Negative interest rates came next. Expectedly, the Euro declined and has stayed between $1.05 and $1.15 to the dollar ever since (and in this run, with the dollar strengthening vs. the Euro just as much as the Euro was weakening against the dollar; now, it may seem obvious that those two things are a part of one another – a tautology, if you will – but I mean it more in terms of causation; I am of the opinion that there was fundamental strength in the dollar and weakness in the Euro the last few years, not merely one being coincident to the other).

We now arrive to the COVID moment of 2020, and from a $1.10 level at the beginning of the year we have now reached a multi-year high of $1.18 (for the Euro), which as stated earlier is coincidentally the starting level for the exchange rate in early 1999.

Summer vacation from history – now some economics

We’ll take a break from the history lesson of above and break it down for you as to what the state of the Euro and the dollar mean to investors now. The last 22 years have been anything but beacons of financial strength or wisdom across the two sovereign economic units that are the U.S.A. and the E.U., and yet the weakness of one is seemingly always counter-acted by weakness from the other, to a point where through all the debt, all the crises, all the headlines, and all the mess, they are currently in tandem with one another (relative to where they started 22 years ago). Yet they both offer essentially no interest to their holders in cash instruments, sovereign bonds, or bank notes. The values have declined in all practical senses to holders, but their exchange rate to one another is still the same 22 years later.

This is what you simply must understand. Saying “the dollar will decline” may very well be totally and completely wrong, if what you mean is “in exchange for another currency.” There is no more “relative” reality in all of finance than foreign exchange of currency. But when the prevailing interest rate of your country has gone from 4% to 0%, in what country is that not a decline?

It is imperative that we understand these things in the right vocabulary and context.

Are V-shaped recoveries part of the new normal?

The bear market that began in 2000 last for almost three years (31 months to be precise), though in fairness, it had multiple catalysts throughout (from the tech sector bubble burst to 9/11 to accounting scandals). The financial crisis not only featured a more profound magnitude in its sell-off, but from the October 2007 high it took until March 2009 to bottom, and then many more years to re-find the high. Even before my professional investing time, 1974 and other such painful periods featured the common thread of usually long periods of time to work through a bear market, let alone recovery.

Much hay is being made, understandably, at the rapidity with which this market has recovered in 2020. 23 trading days to crash and 97 trading days back up. Surreal.

But let’s not forget the ancient history of late 2018, early 2019. The market began to drop in October 2018 around Fed tightening concerns, and accelerated that sell-off in December 2018 around trade war concerns. Just days into 2019 the recovery began, and well before the quarter ended the whole [almost] 20% decline had been recovered.

*A Wealth of Common Sense, Ben Carlson, August 16, 2020

In summer of 2011 we experienced a similar thing – a one quarter drop of nearly 20% followed by a one quarter recovery of the same.

I am not interested in assuming two quick recoveries in a row means that the days of long, drawn-out bear markets are over. They are not. But I will say that central bank actions are different now than they used to be, as is investor psychology and sentiment. Ultimately catalytic fundamentals still end up prevailing, but we are wise to understand this interesting principle: The quicker they fall, the quicker they rise.

Be careful what you wish for

One of the most consistently encouraging data categories post-COVID has been the health and resilience of the residential real estate sector, with home-buying volumes far exceeding expectations, and price levels maintaining surprising strength and stability. I am not raining on that parade, and believe the low mortgage rates driving much of it are a real factor in new purchase activity.

That said, the home ownership rate has hit 67.9% over the robust July report, the highest level since early 2008, and pretty close to the all-time high of 69.9% in 2004. The home ownership rate has vacillated between 63% and 67% for sixty years in our country. At just two points has it gotten this high – now, and pre-crisis.

Low rates are a powerful thing.

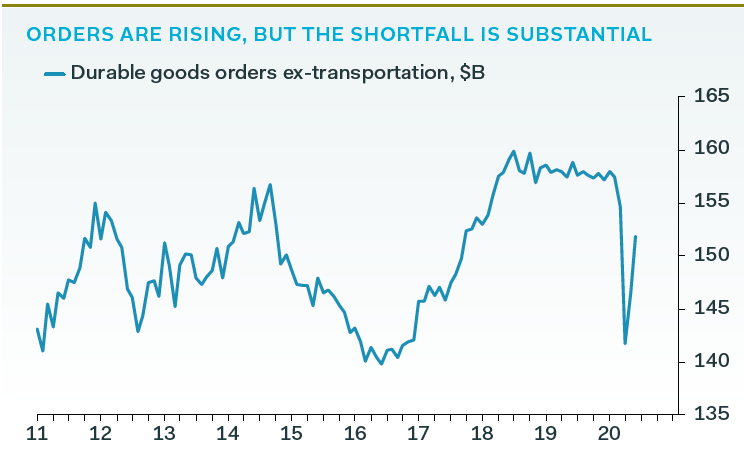

Putting Capex into COVID perspective

I do hope to keep the focus on the business investment aspect of economic recovery in the weeks and months ahead, because I believe it will provide a much deeper understanding of economic confidence and prospects than various consumer readings that financial media is often more focused. Business investment and capital expenditures have both the COVID issues to sort through, and the long-term growth questions that accumulated debt (sovereign and corporate) have brought into the picture. If you believe (as I do) that high debt today means less growth tomorrow, it becomes harder for companies to rationalize investment into long term projects, at least without some optics to a real growth plan.

The good news in the short term is that durable goods orders are now only 3.9% below their pre-COVID peak. At one point they were down over 10%.

*Pantheon Macroeconomics, U.S. Economic Monitor, August 26, 2020, p. 1

But you have to remember, always and forever, that the biggest way to drive future capex is to have a high amount of retained profits. Corporate profits give companies the capital to invest into more growth. Companies without profits have to borrow to invest in their future. Companies that see profits shrinking are afraid to invest in their future. And companies who don’t retain any profits don’t have the capital to invest in their future. So the self-fulfilling prophecy of it all is that companies not making profits lack the ability to invest in future profit-making activities. Replacing equipment, investing in R&D, building new plants and factories – these things represent investments into the profits of tomorrow, yet they require profits today to pay for them. This is why the capex outlook right now is so uncertain – we know profits took a a hit from the COVID lockdowns, but we do not yet know what that impact will mean.

A huge part of why capex was so low from 2009-2016 was that the profit accumulation from the financial crisis was so severely negative. That, and the debt build-up and low rate cycle left a negative view of the future. Capex had begun to pick back up in 2017-2019, so the COVID moment came at an awful time. We will be watching every metric we can because it will tell us a lot, not just about Q1 2021, but about quarters and years into the future

Politics & Money: Beltway Bulls and Bears

- Yes, the Republicans did hold their convention this week, and all things being equal, it probably will be considered a successful convention for them. We will wait until next week’s polling to see where the race stands with both conventions now complete, but the strategy and messaging both candidates and parties intend to take across the finish line are now on full display. I expect a tighter race in the Presidential campaign from here forward than we saw in the polls over the summer, but how much tighter remains to be seen. 2-5 points is tight. 6-9 points, while tighter than 10+, is still not very tight.

- Mark September 14 on your calendar for a special live national video call we will host to discuss the election and its implications for the market and the economy.

Chart of the Week

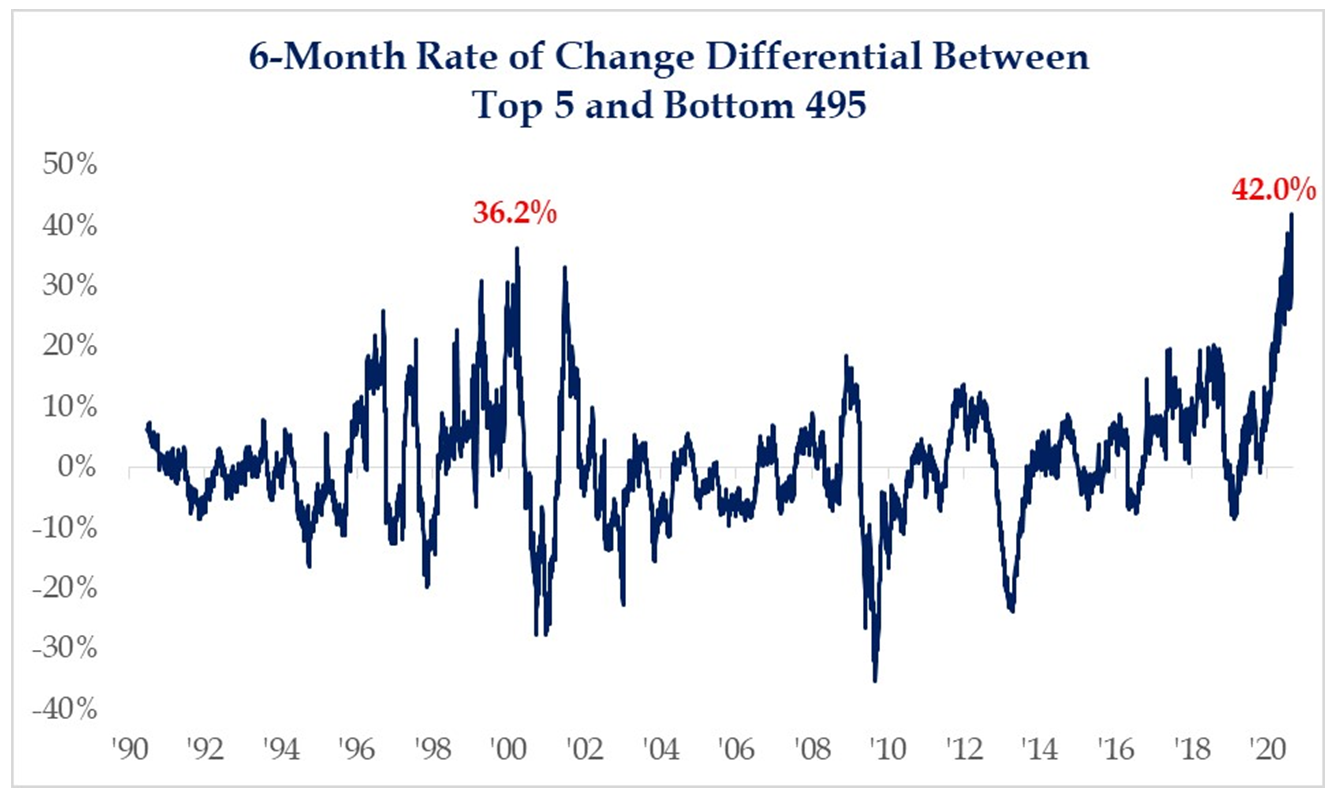

I showed this chart in my Daily COVID & Markets missive yesterday (looking at the biggest 5 companies in the S&P 500, all big tech, versus the bottom 495 companies):

*Strategas Research, Daily Macro Brief, August 27, 2020

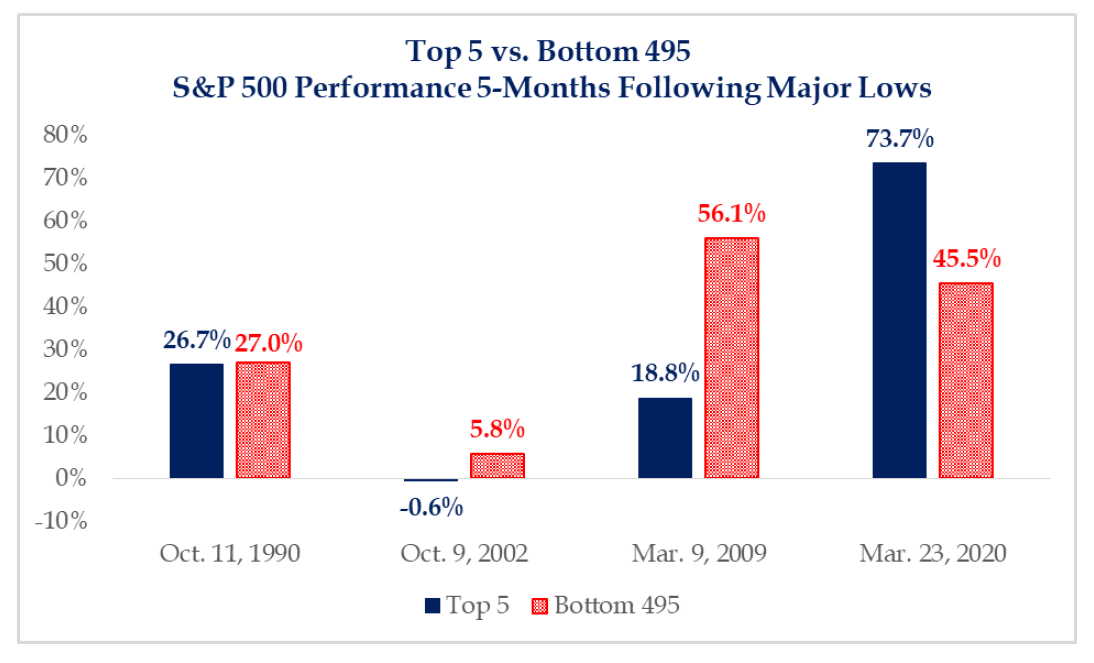

But for our Chart of the Week, let’s put this into a bear market historical perspective, looking at past major lows. This is not just a striking thing happening this year, screaming for a mean reversion, it has no basis in history either.

*Strategas Research, Investment Strategy Report, August 24, 2020, p. 3

Quote of the Week

“The farther back you can look, the farther forward you are likely to see.”

~ Winston Churchill

* * *

I don’t get to bid adieu to August with this Dividend Cafe because Monday is the 31st, so it will be next week, going into Labor Day weekend, that we will officially be into September and the final month of Q3. A wild ride may very well await investors through the end of the year, though the more people talk about that, the less likely it actually is (the paradoxical truth for investors that never goes away).

I wish you and yours a wonderful weekend, and welcome any questions you have about this week’s Dividend Cafe (or any other questions you may have for that matter).

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet

The Bahnsen Group is a team of investment professionals registered with HighTower Securities, LLC, member FINRA, SIPC & HighTower Advisors, LLC a registered investment advisor with the SEC. All securities are offered through HighTower Securities, LLC and advisory services are offered through HighTower Advisors, LLC.

This is not an offer to buy or sell securities. No investment process is free of risk and there is no guarantee that the investment process described herein will be profitable. Investors may lose all of their investments. Past performance is not indicative of current or future performance and is not a guarantee.

This document was created for informational purposes only; the opinions expressed are solely those of the author, and do not represent those of HighTower Advisors, LLC or any of its affiliates.