Dear Valued Clients and Friends,

By Monday the Dividend Cafe will be able to cover whatever it is Jerome Powell has said in Jackson Hole (I have long believed that all economic news and financial announcements should be required to take place before my Friday Dividend Cafe deadline, but this proposal has gotten very little traction with the last several Presidential administrations I have pitched it to). But apart from whatever Powell has said in Jackson Hole (today, Friday, the 22nd), there is plenty else to talk about regarding the state of monetary policy in our country. In fact, while interest rate policy has been covered extensively (here in Dividend Cafe, by other market commentators, by the President, and by some in the media who do not know what an interest rate is), there remains a crucial part of monetary policy that remains very lightly covered – the use of the Fed’s balance sheet as a tool of monetary policy.

That will be the subject of today’s Dividend Cafe, but I have to warn you – a Dividend Cafe about quantitative easing and quantitative tightening might just prove to be more entertaining than you already anticipate it to be! That may be hard because I understand this is already a song the groupies have been begging me to sing, but I am going to do my best to outperform your sky-high expectations.

Talk about the Fed almost always stays focused on interest rates because they are easy to understand (or at least we think they are) and because most people can understand why rates matter to them (mortgage borrowing, etc.). Today, we will make the case that the whole QE/QT thing matters a lot, especially to investors, and in many ways much differently than people think.

Come for the balance sheet talk; stay for the laughs and good times – let’s jump on into the Dividend Cafe …

|

Subscribe on |

The Future in the Futures

By the time you are receiving this, Jerome Powell will have given his speech at the annual Jackson Hole Economic Policy Symposium. I would imagine the futures market will move after his speech because I will be very surprised if he does not give markets some hint or some indication about rate plans for the upcoming September meeting, and perhaps some additional clarity on what to expect for the rest of the year. I am surprised that as of my own press time the fed funds futures have moved down to a 71% chance of a quarter-point rate cut at the September meeting (meaning, a 29% chance of no change, again). 71% is still a pretty high number, but it was 99% a little over a week ago. The very hot PPI report last Thursday gave markets reason to hedge on the idea that Powell was ready to cut. Put differently, it gave people reason to wonder if Powell now had some credible cover to again resist pressure from the President.

I am pretty well on record that I believe monetary policy is too tight, that it is restrictive without a real reason to be so, and that the inflation talk around tariffs is not a monetary issue. If prices do go up from tariffs (and there is absolutely no doubt many prices will, and already have), that still has absolutely nothing to do with the Fed. In fact, based on my belief that it will lead to derivative effects that push the demand curve down and begin to soften production, it would prove a reason to be more accommodative in monetary policy, not tighter. So I am not one who leans into the narrative that the Fed should stay tight, let alone that there is some anti-inflationary reason in doing so. I think that is simplistic, fallacious, and in many cases, disingenuous. But at least it is a soundbite, and man, do some people love soundbites.

I also am very much on record that executive branch pressure on the Fed is a very, very bad idea. I am always confused by people who say, “the Fed is too political” or “the Fed’s credibility has been undermined,” who then conclude, “so therefore we should make it more political and therefore we should damage its credibility even more.” It is not a great way to think, nor does it work. A reduced estimation in global financial markets of central bank credibility will hurt other initiatives of this administration, and I believe Secretary Bessent knows this. The process is playing out with typical Reality TV flair.

In short, I believe the fed funds rate is too high; I believe the President is asking for it to be way, way too low; and I believe the whole process is tragic to watch.

And I believe they are going to cut at the September meeting (note: I typed this before Powell’s Jackson Hole speech, so if I have already made me look an idiot, kudos to him!).

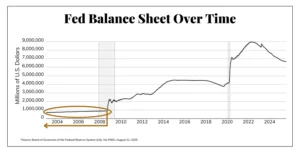

The Olden Days

I am old enough to remember the olden days of a Fed balance sheet that looked like the circled area below:

In fact, the aggressive use of buying bonds by the Fed was not a policy tool for our Fed at all, until the immediate aftermath of the financial crisis (GFC). The initial announcement came in November 2008, and I do not believe it even had a name attached to it at that time. The Fed buying $600 billion of mortgage-backed securities then was widely seen as a crisis management tool and not a monetary policy tool (at that time). But in March of 2009, when the amount of bond-buying was expanded to $1.25 trillion, and Treasury bonds became the main target of the bond buying, it was clear that this was a “bonus” tool of monetary easing (a way to ease further when you are already at a 0% federal funds rate). QE1 ended up seeing about $1.75 trillion added to the balance sheet of the Fed, with the policy objectives essentially being to:

- Impact rates on the long end of the yield curve,

- Add to excess bank reserves.

- Specifically, bring stability to mortgage markets that were largely frozen.

I am not sure if I would say that the above sequence represents a good “in order of importance” list, or not. If I had been inside FOMC meetings, then I may have walked away believing the priorities were the exact reverse of that list, but it isn’t really material now. Almost anything done by policymakers in late 2008 and early 2009 was understandably seen as an emergency measure, and it was not really analyzed as a “new normal” of perpetual policy – because it sincerely was not seen that way (by markets, by analysts, and I believe not by central bankers, either).

When the Fed announced another round of quantitative easing in 2010 (an announcement, I should say, made at Jackson Hole exactly fifteen years ago today), no one believed it was anything other than a macroeconomic policy boost representing a hyper-aggressive form of monetary stimulus. Credit markets had been functioning for over a year. Mortgage markets had normalized. Financial market liquidity and bank stability were perfectly adequate (though by no means robust). The QE2 rationale made no sense apart from the classic stimulus of demand using monetary manipulation, and Chairman Bernanke was quite transparent about such. The size of QE2 was “only” $600 billion, but risk assets immediately priced in the fact that the central bank was taking a Japan-bazooka approach to avoiding recessionary deflation. An unemployment rate of 10% two years after the recession started was all the fodder Bernanke needed to make this call.

But then the real bazooka was QE3, and this was the occasion for me to fully grasp that American central bankers did not view Japanese monetary policy as “lessons to be learned from and to avoid” but rather “lessons to learn from and emulate.” Inflation was very low (basically 1.5%), giving the Fed huge latitude with its critics who had all wrongly prophesied hyper-inflation because of QE. The economy was slowly growing, a double-dip recession had been averted, and yet growth was slow. The Fed basically made an “open-ended” commitment to continue buying bonds and growing its balance sheet (a mix of Treasuries and mortgage-backed securities). At one point, Chairman Bernanke explicitly stated that QE would continue “until unemployment got to 6.5%.” It would get there (and go lower, still), and yet QE3 would continue as the Fed rightly concluded that markets were addicted to the sugary love of abundant financial liquidity. The S&P 500 would be up 32% in 2013. Any talk of ending QE3 caused stock (and bond) markets to throw up. Ultimately, the Fed would continue buying assets onto its balance sheet (QE) all the way until late 2014 (fully six years after the financial crisis had started).

Quick Clarity

When we refer to “adding to the Fed balance sheet” and “buying bonds,” what we mean is the process of the Federal Reserve crediting cash to the accounts of major banks and primary dealers in exchange for Treasury bonds and Mortgage bonds they held. At first, there was limited financial liquidity, so this process was intended to facilitate those who needed cash (institutional holders) by providing an additional buyer in the market. By QE2 and especially QE3, there was not a lack of liquidity, so the sellers were not “cash-starved financial actors needing an additional buyer,” but rather it was basically just the central bank crediting additional cash to the excess reserves of banks. Because the Fed was buying these bonds with money that didn’t exist, it is said to be stimulative – that is, creating new reserves in the banking system – without adding money to circulation. This put downward pressure on interest rates, in theory, and also allowed investors to take advantage of excess liquidity by replacing their treasuries and mortgage bonds with cash that could then be deployed into higher-return assets.

That was the intent. Those were the mechanics.

The Bank of Japan was the trailblazer with this process; they became the vast majority of the Japanese bond market (they did it so aggressively). Federal Reserve QE was very, very similar, but in lower magnitude to the size of our domestic bond market and lower magnitude relative to the size of GDP than Japan’s version.

Back to the Modern Era

So Bernanke and QE1-3 and 2008-2014 are all soooooo old school that I am sure it feels like I am about to start quoting from Shakespeare or something. And I assure you, something is rotten in the state of Denmark, if you know what I mean. The Fed didn’t add to its balance sheet or reduce it in 2015 or 2016. This was one of the only periods since 2008 during which there has been no quantitative easing or quantitative tightening. In that sense, we have mostly been in a new world since 2008, in that the size of the Fed balance sheet did not change much pre-crisis, and since then it has mostly been changing a lot, one way or the other, every year. But 2015 and 2016 were steady-state exception years.

In 2017, Fed Chairwoman Janet Yellen began a very, very modest reduction of the Fed balance sheet, but here again a clarification is needed. I referenced above that quantitative easing was the Fed “buying” bonds, so I suppose it seems logical to interpret quantitative tightening as the Fed “selling” bonds. But here, there is something a little more passive going on … Actually, the bonds the Fed held would mature, and the Fed would just not reinvest all of the proceeds. They were reinvesting some, but the amount they targeted for reduction of the balance sheet would not be reinvested, essentially “rolling off.” This meant the Fed never had to be an active seller of bonds and was never aggressively pulling liquidity from the financial system. Yet, the level of assets on their balance sheet was being reduced (albeit at a snail’s pace).

In 2018, the new Fed Chair, appointed by President Trump, one Jerome Powell, began a slightly more aggressive pace of quantitative tightening while also increasing the federal funds rate from the 0% it had been since the financial crisis (technically it was at 0.25%). This two-headed tightening, modest by today’s standards, caused a credit market revolt in 2018, ultimately leading to his infamous reversal of policy in early 2019. At this point, those who had spiked the football began to wonder if the Fed’s high balance sheet could ever be reduced without severely disrupting financial markets and economic activity. The theory was that the patient would be ready to walk on his own, but 2018 called into question whether or not the crutches could ever be put down.

Ironically, a Fed Governor had predicted this in 2013 when Bernanke initiated QE3. This Fed Governor questioned whether QE3 would not have a diminished return relative to QE1 and QE2, and suggested that the “costs and risks had to be carefully weighed” before proceeding.

That Fed Governor’s name? Jerome Powell.

COVID Clarity

Those who remember the COVID era may remember it as a period of tremendous ambiguity in public health policy, but there was one public policy realm where there was no ambiguity for this economic analyst whatsoever: The Federal Reserve was undoubtedly going to use hyper-aggressive quantitative easing for any financial turmoil America faced as a default position going forward. The manner in which trillions of dollars were so immediately added to the Fed’s balance sheet with no discussion whatsoever of “costs and risks” left no room for doubt. It wasn’t controversial. It wasn’t debated. It wasn’t resisted. Granted, the economic moment of pandemic shutdowns was severe, but the impulse was crystal clear: The Fed’s balance sheet was now a weapon to use whenever liquidity conditions warranted such. The central bank believed that the use of QE1-3 post-GFC was a success – inflation predictions had proved laughable; the dollar had not fallen; financial markets had stabilized; a double-dip recession had been averted. So why not? Call it QE4 or QE5 if you want, but the Fed’s balance sheet doubled in a very short period of time.

Gone was any discussion of reducing it back to GFC levels. Now we were wondering if the new play was QE-infinity.

One of These Things Was Not Like the Other

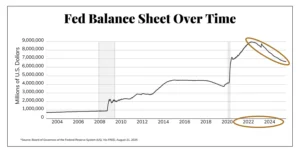

I have no problem admitting that I am [pleasantly] surprised by what transpired next. Since mid-2022, the Fed has reduced its balance sheet by about $2.2 trillion. They absolutely continued adding to it for way too long, but they started reducing in mid-2022, also in concert with rate hikes, and nothing like 2018 happened this time.

Credit markets did not freeze up. Levered loan and high-yield bond defaults did not skyrocket. Spreads did not blow out. And somehow, the 2018 outcome just did not play out at all.

Now, you will note that the balance sheet remains much higher than it was pre-COVID, so they have hardly “normalized” even by post-GFC, pre-COVID standards, let alone by pre-GFC standards. That. Ship. Has. Sailed. It isn’t going to happen, ever. Not in my lifetime. Not in your lifetime. Not in your grandkids’ lifetime. But I digress.

How did the Fed get away with $2.2 trillion of quantitative tightening over the last three years without much collateral damage? I am open to a number of theories, but the avoidance of hubris keeps me from reaching any overly dogmatic conclusions. I believe it is sensible to assume that QT was so well-telegraphed this time that there was less “shock and awe” to financial markets, and more of a “baked in” dynamic that minimized disruption. Financial market liquidity was also a lot stronger going into the tightening period, with many corporate balance sheets well-liquified from low-cost borrowing in the 2020-2022 period. I also believe markets knew that the Fed would reverse if they needed to (like in 2019), which made the likelihood of them needing to much less.

So What Does it All Mean for the Here and Now?

I hate when I am getting to the end of my own Dividend Cafe and my own sub-titles are asking me to get to the darn point, yet I want to keep typing for hours. But alas, it is time to bring this to a conclusion.

My basic takeaways for you regarding QE/QT, even as all eyes are on Jackson Hole, the Fed meeting in September, where interest rates are going, and who will be the next Fed Chair (not to mention one or more Fed governors that get appointed between now and then) are as follows:

- The reverse repo facility is now almost at $0. There was nearly $2.5 trillion at its peak when the 2022 QT began. That large excess was necessary post-COVID because there was more liquidity than needed, and the open market operations of the Fed couldn’t affect its interest rate targets if the money wasn’t parked in reverse repo. Those days are over. The liquidity dynamic is real, now, and QT will truly drain reserves from the financial system in the months ahead if it continues. And I do not believe it will.

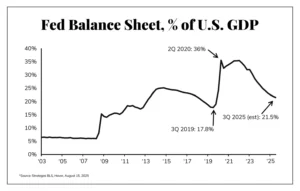

- I made the point above that the Fed’s balance sheet is still $2.5 trillion larger than it was pre-COVID, and that is true. But here is how I believe the Fed now sees it, and how more and more analysts are coming to see it:

Using nominal dollars for the “right size” of the balance sheet is not going to fly. That the balance sheet was 18% of GDP pre-COVID and has decreased from 36% to 21% now will be used as the rationale for a permanently higher balance sheet. If something can’t happen, it won’t, and I do not believe they can reduce the balance sheet to pre-COVID levels. But if something can’t happen and it needs to be explained, this percentage of GDP rationale is the best sales bit they have.

- By continuing with a little tightening (reduction) of the mortgage securities on their balance sheet, they can effectively do a little easing (addition) of Treasuries, effectively helping to finance T-Bills and control rates, all the while taking a balance sheet neutral approach. In other words, by offsetting QT with MBS and QE with Treasuries, they get to a place of neutrality in the total balance sheet, but effectuate a couple of policy goals at the same time.

- The three-year grace period of hangover-free QT does not mean that QT is no longer a “risk and cost” for QE. It is, and we remain completely without any historical precedent domestically or abroad of a country using asset purchases at its central bank as a monetary tool, and then completely undoing it, so as to teach markets what to expect. It has never happened. All central bank balance sheets that blew out have stayed blown out – every single one. And therefore, making predictions of a benign outcome around future monetary policy operations is speculation, not rooted in historical precedent.

- The markets would respond more favorably to reports of financial liquidity enhancement via “quasi-QE” or “stopping QT” than to even another 25 basis points of rate cuts. It is a policy tool I expect to see more broadly used for accommodation in the months before Powell’s term ends and in the month after Powell’s term ends, no matter who his replacement proves to be.

- If you really want to see a dynamic change in monetary policy, either to tighten or to ease, it will not be with the balance sheet, but with the interest paid on excess reserves. All the build-up of excess reserves you can fathom (QE) addresses financial markets’ liquidity, but it does not stimulate the economy. The Fed’s Interest on Reserve Balances is the key policy rate to stimulate credit growth. Getting that rate to a point where banks are highly motivated to lend is at least 100, if not 150, basis points away. Is there loan demand for this? Do banks have the willingness to go there? Is private credit doing what bank lending is not doing? These are not questions easily answered in the short term, and I will say this: I doubt they are best answered by central bankers, anyway.

Conclusion

But do I think it is coming (the Fed lowering interest on reserves to a point that stimulates credit growth)? I do. Not this year, but at some point, I do. Central bankers have better memories than a lot of people. I have a lot of gifts and a lot of weaknesses – but my memory remains a gift. And I remember well the various times our central bank had to decide how to juice the economy. One thing I have learned is that when you do not fear a hangover, many people do not fear having the next drink.

Quote of the Week

“Just because nobody complains doesn’t mean all parachutes are perfect.”

~ Alfred Hawthorne Hill

* * *

Lots of kids going to lots of schools this weekend, and the real end of summer is upon us. And then next weekend, the real, real beginning of fall comes when college football kicks off. In the meantime, enjoy this weekend ahead, take in another weekend of heat and sun, and reach out to us about anything, any time. This may have been a heady Dividend Cafe, but what it means for you is our job. And to that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet