Dear Valued Clients and Friends,

Please join us Monday as we host a special national video call featuring an updated look at the economy, a post-inauguration feel for market expectations of Washington DC, and more. The replay of that call will be part of Monday’s DC Today.

The idea that there are more significant things facing investors than the moving and shaking of the beltway is anathema to many in this politicized culture. The 24-hour news cycle did not create a national obsession with national politics, but it has fed it, exacerbated it, and fueled it. The cultural reasons politics have become an Olympic sport – a consumer activity – really ought to be the subject of an entirely separate article.

As the country has said goodbye to the prior administration over the last couple of weeks, and as the new administration has begun to settle in, I have focused last week’s Dividend Cafe and this week’s as well on what I believe is a non-political and yet more important topic for investors than anything the beltway has to offer. Part of the reason is fatigue and exhaustion. This election cycle was a doozy, and we gave abundant coverage to election-oriented implications in the markets. But beyond the doozy of this year’s election cycle, coupled with all of the COVID realities, the post-election period this year was particularly exhausting and ultimately even trying. Along the way, the daily presumption for market pundits was that the nooks and crannies of Georgia, of the election disputes, of the incoming Biden team, of each and every aspect of what was happening around the Potomac were front and center for markets.

I am sure I have become a broken record for many of you as to why this thinking was and is fallacious. A quick glance at the TBG YouTube Channel reflected something like 80% of recent media appearances asking some version of what markets thought about some aspect of the political domain. But the point I am making today is more than just “politics is overrated in evaluating market conditions” (even though that is very true). I not only believe this subject of Inflation vs. Deflation is more important than anything else in understanding the 3-year, 5-year, and 10-year state of financial markets, I also believe it is a welcome reprieve from what is just overdone, over-covered, over-saturated, and ready for a break.

But I also cheated a little last week when I said that this topic is not itself quite as apolitical as it seems. And I do think I will explain what I mean by that this week. But it won’t feel like a political diatribe. It ought to feel like what it is – a deeply embedded economic reality that our society is learning to live with, and that is going to lead to many good portfolio decisions and many bad ones.

Inflation vs. Deflation Part II – jump on in to the Dividend Cafe.

No more teasing

I asked last week …

If you believed that interest rates were going to be 0-2% would you invest capital differently than if you believed they would be 5-7%?

I believe interest rates are bound in the < 2% range, not the higher range.

If you believed that inflation would run 1-3%, would you invest differently than if you believed it would run 4-6%?

I believe inflation is going to run at the lower end due to disinflationary forces that the Fed cannot control, with standard price inflation still eroding purchasing power over time (1-3% compounded over 25 years is still a 50% reduction in purchasing power), yet with deflationary forces being the greater societal impediment than inflation for years to come.

Does one’s view on interest rates and forward-inflation impact their expectations for P/E ratios (market valuations)?

I believe P/E ratios run higher than historical averages when prevalent interest rates are on the lower end.

If credit is going to tighten (ease of access to capital and cost of capital), would that alter one’s allocation to corporate credit, private equity, public equity, and a host of other risk asset classes?

I believe that the policy bias in our country is overwhelmingly for looser credit and that, in fact, we have created an addiction to easy credit that will distort prices, foster mal-investment, and lure people into certain investments that will eventually end badly.

Would one’s view on the U.S. dollar potentially influence their allocation to domestic vs. foreign assets?

I actually did reveal our perspective on this last week. I believe the dollar was over-heated entering 2020 and spent the post-COVID quarters giving back some of its froth of the prior years. But ultimately, how the dollar does relative to other currencies is a two-sided equation, with our own attractiveness as a source of foreign investment one piece and the other piece being everyone else’s attractiveness as a destination for capital.

And regardless of how one’s views on interest rates, inflation, credit, and currency impacts the decisions, they make on investment decisions, will all of these things impact the expected return on all asset classes (whether or not it alters your weightings in such asset classes)?

I believe that the expected return of broad asset classes will be lower than many are used to when priced against a risk-free rate of 0% vs. more normalized monetary conditions.

And if these things impact expected returns in various asset classes, does that have practical significance to one’s financial planning, accumulation goals, withdrawal goals, and other such tangible dimensions of wealth management?

I believe that one’s expectations in financial planning must be more yield-centric than total return centric in this environment and that yields are compressed (pushed down) by the present landscape. This means that investors either alter their cash flow withdrawal plans (not going to happen) or change how they monetize their financial goals (different risk levels, higher spend-downs of principal, different asset allocation, etc.).

Okay, with all the conclusions on the table, let’s go about defending them.

When a bottom is not a bottom

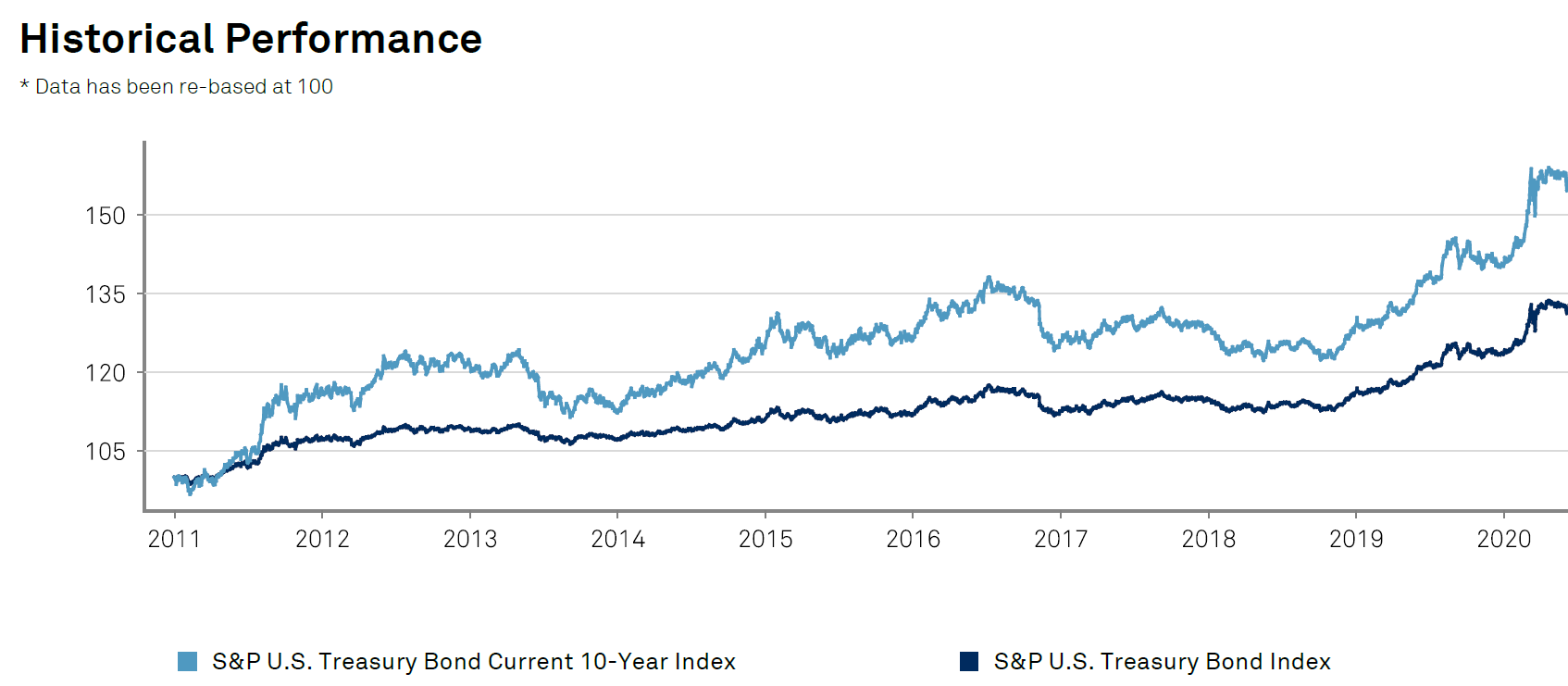

I didn’t take the time to review my own writings on the subject, but I recall vividly a pretty fair amount of coverage from 2010-2019 on the relative unattractiveness of bond investing with yields at 2-3% (using the 10-year as a reference). And I am sure I, and the abundant consensus opinion on the subject, were not wrong that risk-adjusted, it was hardly an enticing place for capital. Yet a 20% return for a 30-year bond last year and an 11% return for the 10-year comes on top of what has been non-stop positive returns for these “over-valued, under-yielded” instruments for the entire post-GFC era. These bonds derive 100% of their return from (a) Their coupon, and (b) The price increase that comes when yields go down. In short, they keep making money as interest rates keep going lower. And the bottom has been elusive, to say the least.

*S&P Global, Treasury Index, Dec. 31, 2020

For my purposes in evaluating what all this means, I do not first have to understand why it has happened; I first just need to be abundantly clear that it has happened. From there, we can do the work we need to do. The reason I say that is that I believe the vast majority of arguments used against continued disinflationary forces are arguments that should have and could have and often were made in the last decade, with even more force. So when we establish the “what was” versus “what we would have thought” about the past, it makes us more open-minded and intellectually curious as it pertains to the future.

Why are rates low?

One popular theory is that the Fed has forced rates down, and there is obviously truth to this, since the Federal Funds rate is, well, zero percent. But the Fed Funds rate is an overnight lending rate, and it is controlled by the Fed “targeting” it, then using open market operations to help implement it. They can’t fully control the ten-year yield because it is far outside of their policy purview. Now, I believe the longer end of the curve is influenced heavily by the short end of the curve, but my point is this: If the Fed didn’t buy a single Treasury bond, we know that the market pricing for the ten-year Treasury is, well, about the 1% it currently trades at.

The market is not expecting enough growth and/or inflation to push long-dated bond yields higher. This is the reader’s digest answer to the question. But when we expand on it, we get more information important to our investment decisions.

How it works

First of all, an issuer of debt (the borrower) does not need to pay more interest than investors are willing to accept, and in this case, the issuer/borrower is the United States government. The buyers/lenders are people who want a safe haven for their dollars or foreign actors who want to convert their currency into dollars. The decision for safety-driven actors (sovereign wealth funds) is relative to other currencies. The United States has seen its bond yields pushed down for years by the sheer violence of downward pressure on bond yields in other countries. If Japan and Germany are issuing debt at 0% (or lower?), why should the U.S. have to pay much more than, say, 1%? Pretty logical, right?

But this “global competitive reality” that has enabled low rates for so long is (a) Only part of the story, and (b) Evolving into a new story right before our very eyes.

Ultimately my view can be summarized as follows: Higher government spending as a percentage of GDP has created a negative feedback loop where we have suppressed economic growth (like in Japan), requiring more stimulus to offset the effects of that lower growth, which further suppresses growth, rinse and repeat.

I owe it to you to explain the case. And I will start with the clear economic reality that as spending and debt have exploded, bond yields have responded by going down, then down more, then down further. If you would have expected the opposite, you are not alone. An explanation is forthcoming.

Putting it into perspective

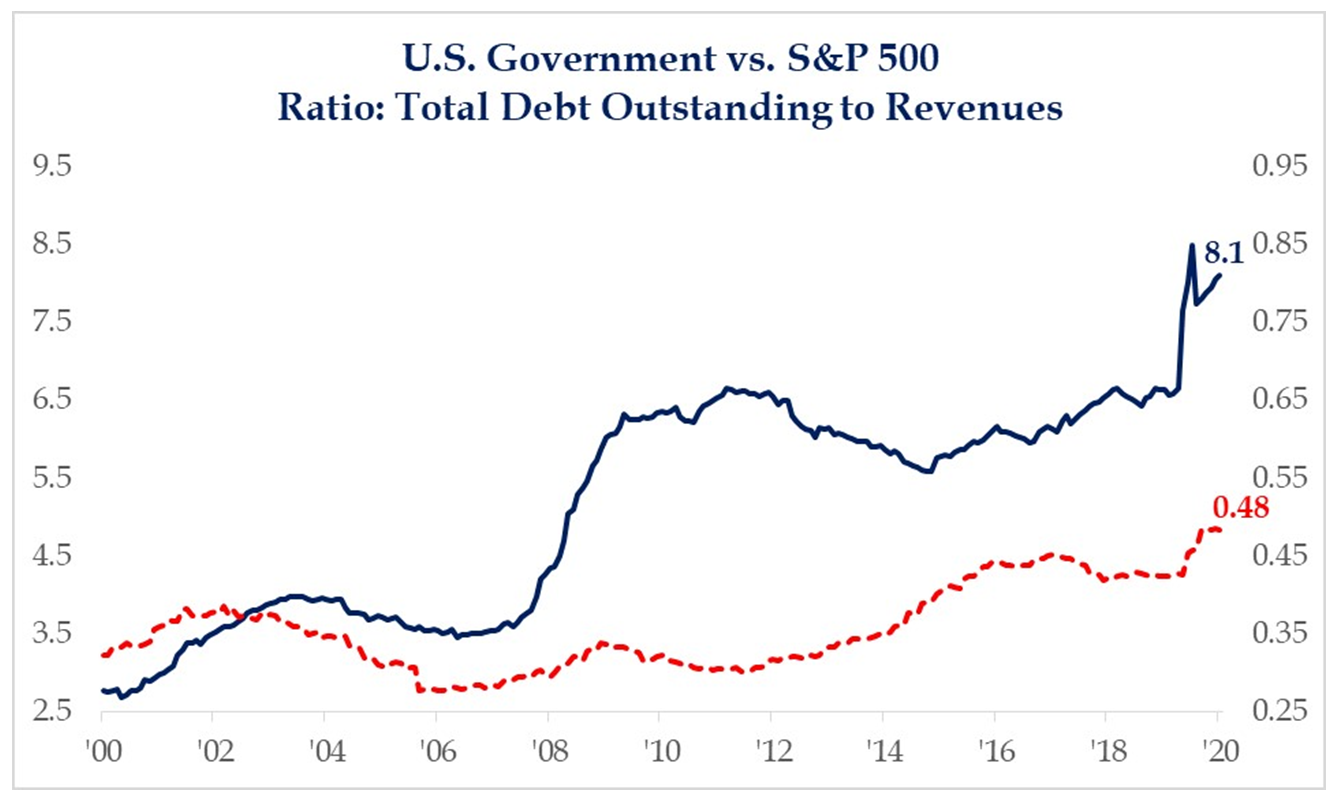

Pretending the U.S. government was a company (it isn’t), they currently have $27 trillion of debt (and that does not include entitlement liabilities like Medicare and social security), and they collect $3.4 trillion in annual revenue, so a revenue-to-debt ratio of 1-to-8. The S&P 500, on the other hand, has $11 trillion of annual revenue and $5.5 trillion of debt, so a revenue-to-debt ratio of 2-to-1. This 16x difference between the debt/revenue ratios of [reasonably highly-indebted] public equities and Uncle Sam is almost unfathomable to consider.

*Strategas Research, Daily Macro Brief, Jan. 22, 2021

Multiplication reality

The key tenet in Keynesian economic thinking is that government spending can be used to generate a “multiplier effect” in the economy – that when the private sector is down and out due to economic doldrums, the government can use the power of its purse to make up for that lost output, and achieve a greater economic impact from those expenditures that can foster economic growth and health. It can work when that multiplier effect is positive. It can not work when that multiplier effect is negative.

And that is where we find ourselves – where government funding of deficits (the process of taxing the private sector in the present or in the future via borrowing) are putting downward pressures on productivity and undermining growth, not facilitating it.

Keeping my promise

I would be totally sympathetic to the claim that it sounds as if I am setting this up for some sort of political agenda against government spending, and prima facie, I suppose that is fair enough. But that is actually not where I am going – not in any political sense. We have had a steady and heavy increase in government spending under two administrations post-GFC. One was Democrat; one was Republican. Congress has had leadership alternate between both parties as well. Various aspects of fiscal stimulus have been used that were at times pleasing to one party and at other times pleasing to the other. None have changed my narrative.

This is as non-partisan and apolitical as it gets because I am not speaking to the legitimacy or necessity and certainly not the political preferences of what the spending has been about; I am only speaking to the math and the economics. Transferring resources from their best and most productive use to some use that is less productive by definition subtracts from organic growth, period. That is not a super controversial statement. And neither is this: Growth achieved by debt spending is pulling future growth into the present, thereby lowering future growth. If you buy new living room furniture today with your bonus coming next year, the growth you would have achieved in wealth and income next year is less than it otherwise would be. Yes, you have new furniture now, but your growth in the future is diminished. Maybe it is worth it! In fact, maybe you have to do it (who wants to have no place to sit in their living room). But it is still, as a basic law of math, a compression of future growth.

Sometimes government spending is needed. The legitimacy of the spending is outside my agenda here – I am simply talking about cause and effect. In other words, I merely want to follow the science. And to the extent that we, like every other developed country on earth, have grown our debt (and done so substantially), we have put downward pressure on future growth.

Can’t debt be used productively?

This is where the conversation gets a little muddy, for there is surely no debate about the fact that sometimes debt – sometimes that pulling of future growth into the present via borrowings can be extremely lucrative. This is why companies use debt in their capital structure. Borrow at 5% to fund a project that creates a 20% return, and you have built wealth, not destroyed it. There are risks. There are limits. But productive debt, economically, is not the mathematical suppressor of growth that I am describing. Fair enough.

The problem is that countries reach the point where their debt levels become the opposite of productive. This diminishing return is a law of nature, and it is true in the private sector, too – at some point, there are not enough productive projects for a company to invest in with borrowed money, and they end up wasting great resources for projects that generate less and less of a return to the company (perhaps even a negative return), even as the cost of that debt and weight of that debt grows. This is all the more true of a government, where a profit motive is not driving expenditures. There is a point on the axis at which debt begins subtracting from growth in a nation-state, and we have been at that point for some time now.

Prove it!

Okay.

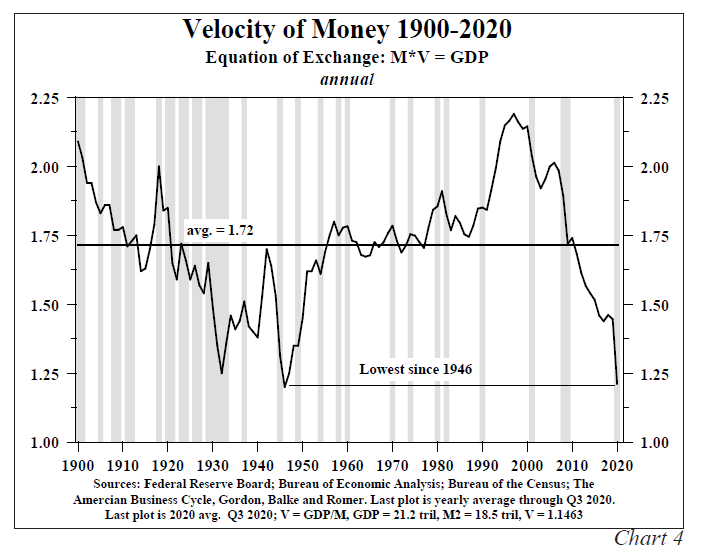

And remember last week’s point that inflation was the by-product of (a) Increased money supply (we have had plenty of that), Multiplied by (b) The Velocity of that money (it’s turnover in the economy)?

Velocity fell almost 18% in 2020, but of course, the economy was shut down for much of the year. It’s hard to “turn money over” when you are locked down, right? But that is the exception that proves the rule – the flooding of money into bank reserves, the explosion of government spending, and all of the various monetary and fiscal stimulus tools still could not foster the velocity and money productivity that are needed.

What do lower rates and heavily liquefied credit markets do, then?

All things being unequal …

We know lower rates stimulate borrowing. Who tends to borrow more money? Wealthier people and people buying assets (especially real estate assets) with borrowed money.

We know lower rates push up risk asset valuations (i.e., stocks). Who tends to own more stocks? Wealthier people.

Now, I refuse to add to the silly narrative that only wealthy people buy real estate and stocks. The argument that this Fed policy approach exacerbates the gap in wealth is indisputable because of the proportion of ownership between wealthy people and less wealthy people of risk assets. But that is not the same as saying that middle-class people do not own stocks (401k accounts, IRA’s, pensions, etc.), let alone saying they do not benefit from a lower cost of home borrowing. There is an absolute benefit to a large percentage of the population, sure. But relatively speaking, if this kind of thing matters to you (it seems to matter to a lot of people until Fed policy comes up), there is no question that it disproportionately impacts wealthier people.

It’s rude to blow bubbles

The crucial missing ingredient in my above paragraph is not how Fed actions “help” stocks and real estate, or “who” it “helps” more. Rather, it is what inevitably happens when any “help” is given at all outside the organic forces of the universe. Well-intentioned interventions are still interventions. And some interventions with side effects are still necessary (think: vaccines). But no intervention can ever, ever be presented as if its benefits are the end of the story. There are trade-offs. And history has been merciless in its verdict that central bank interventions lead to distortions, and we need to understand this from A to Z as investors. Few things are more important.

Are all distortions bubbles? Of course not. But many distortions turn to bubbles or have the potential to turn to bubbles, and all distortions are still, well, distortions. What that means is, simply put, they create mal-investment. And what that means is they direct capital to a place that may very well (and usually is) a sub-optimal place. Best case? They distort the relationship between risk and reward so that even if capital goes to a “functional” place, it does so without a clear picture of the risk involved.

This is one of the reasons (amongst many) that we are so fond of dividend growth equities. We don’t want our client’s investment return to be dependent on the price level and the valuation level of assets. Dividend growth allows us to drive a return from something far less “manipulatable” – free cash flow, and our receipt of it.

Inflation? Yes

My belief that the economy is fighting dis-inflationary forces, based on everything I have said above, presupposes an understanding of some core economic truths. Prices in the economy do not move in perfect harmony with one another; they move in response to changes in supply and/or demand for a particular product or service. Therefore, the entire concept of a unified price level in the economy is a myth, and it always has been. Prices matter only when contextualized to a specific person, need, expenditure, and situation. A plethora of examples are available to reinforce this point, but one that sticks out to me from when I first began studying economics three decades ago is this: Talking about a “price level” in the economy is like talking about “average rainfall” for golfers and expecting it to matter to a particular golfer at a particular course on a particular weekend. Hopefully, I need not say more.

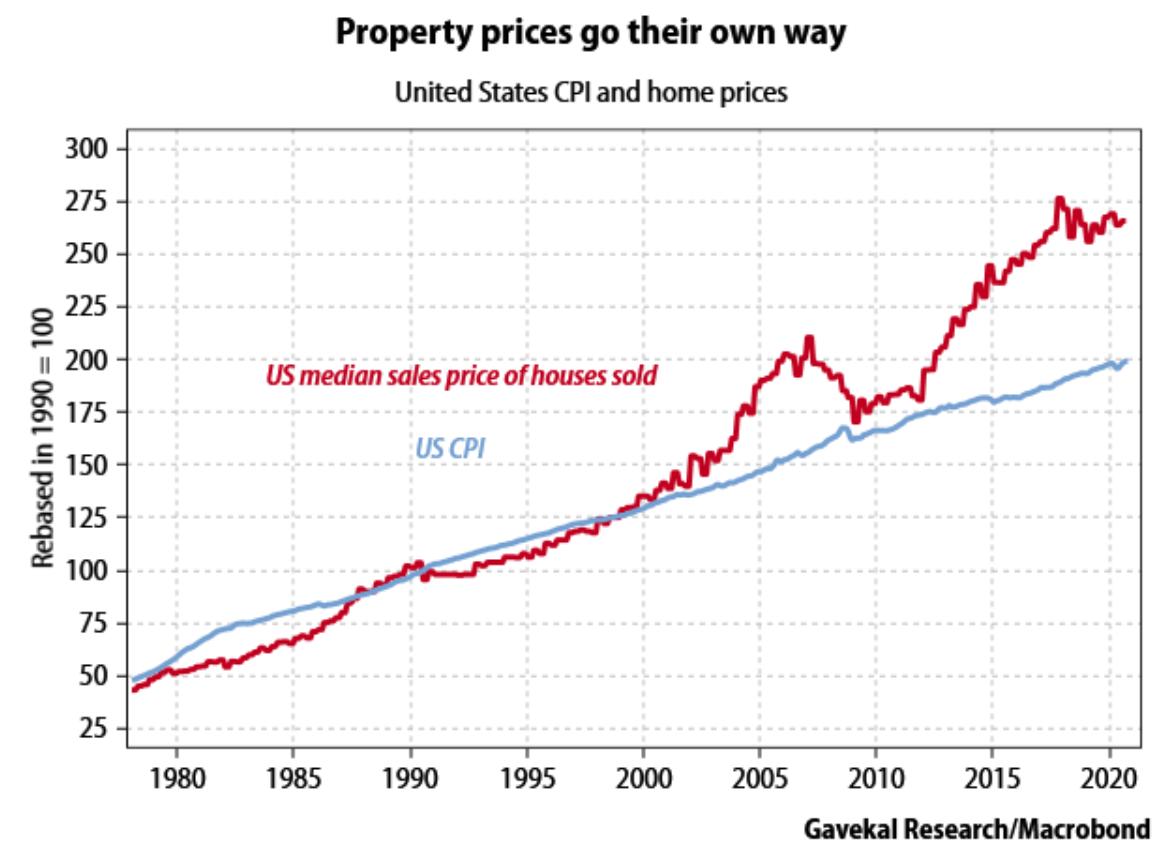

So, therefore, this chart, and one of the fundamental conclusions of this treatment on inflation and deflation and investing should not be too counter-intuitive for you. Believing that there is and/or will be price inflation in certain assets or expenditures is not at all inconsistent with the larger thesis that dis-inflationary forces are a greater economic challenge than an inflationary one.

Housing prices in the United States are a perfect example. They behaved in a pretty right harmony with “consumer prices” (CPI being one of the imperfect but consistent measures to try and capture a price level, or at least an apples-to-apples comparison of prices year-over-year) for decades! Then they “bubbled” (or “inflated”) even more than CPI throughout the U.S. housing bubble of 2003-2007. Things corrected, and the great “reflation” in housing prices of the last eight years has further disconnected prices in housing from general consumer prices.

Why does this matter? Because as the prior point of what lower interest rates tend to inflate (asset prices vs. wages and vs. consumer prices), divergent inflationary realities will be present, and will lead to plenty of bad analysis, and will distort the proper action plan for many investors. Oil prices that go up in response to a weaker dollar or in response to their own supply/demand realities will cause some to say, “see, inflation is back!” Housing prices, like any asset price, are a by-product of supply and demand, but also of the supply and demand for the money that is used to buy it.

How to manage prices?

The best way to manage prices is to not manage prices. We essentially do not have much of an issue with “price stability” in our country and in our economy anywhere but where we attempt to manage such prices. Therefore, where we get interventions in the inflation/deflation construct, it is through interventions in the supply/demand of the MONEY used to buy ASSETS, not in the “prices of things.”

Conclusion

This, my friends, is what we are dealing with. We have an intense management of the price of money (interest rates) and the supply of money (Fed, QE, M2, etc.), and that plays directly into the prices of assets. It creates distortions. It surprises investors. It plays into wealth and income gaps. It has sociological implications. It does a lot of things, some good, some bad.

But it does not raise interest rates because the wage growth that comes from organic growth, not interventions in the supply and demand of money, does not materialize. GDP growth that reflects more trade, more production, more consumption, more economic activity, is muted by the factors I described above (crowding out of the private sector, future growth pulled to the present). Deflation rules the day, and we push on a string trying to get out of it. This is the state of our economy. It is called Japanification. It wants inflation (to lower the real impact of paying back the debt), but it can’t get it.

So we face the hangover of a monetary and fiscal binge that hasn’t even ended yet, and we seek to avoid what may become “bubblicious,” all the while recognizing policymakers have made conventional assets like cash and bonds less attractive. This is the foundation out of which Operation Magnify was born, whereby we apply the principles of dividend growth, alternatives, and true risk management to each individual client, based on each individual situation.

You won’t find a better solution than that. I am not sure I could come up with one if I wanted to.

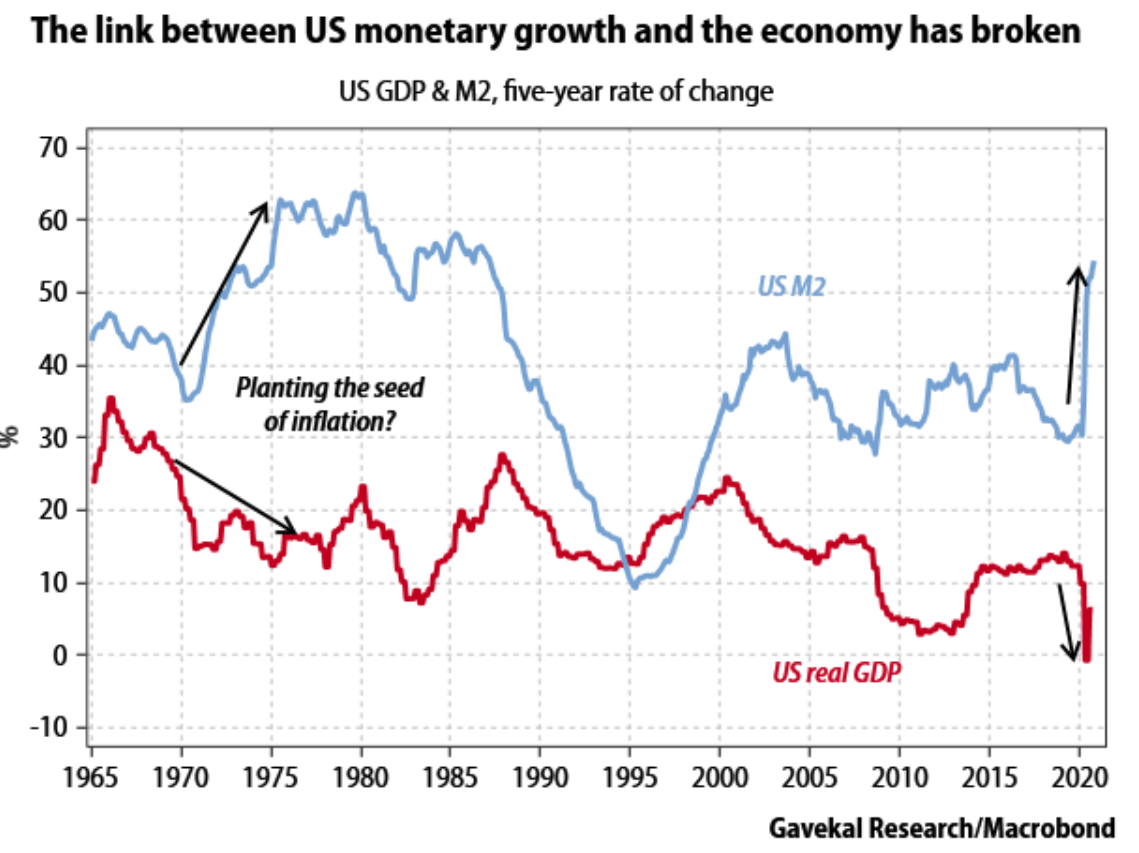

Chart of the Week

In line with my earlier points of the diminishing return of stimulus, more FISCAL stimulus (government spending) has not created better GDP growth. But more MONETARY stimulus has not either. We have seen in a clear manner the disconnect post-GFC, and it is widening further now.

Quote of the Week

“ There is only the fight to recover what has been lost and found and lost again and again: and now, under conditions that seem unpropitious. But perhaps neither gain nor loss.

For us, there is only the trying. The rest is not our business.”

~ T.S. Eliot

* * *

I have very much enjoyed writing the Dividend Cafe today, and I really hope both this and last week’s commentary scratched some itches for you. The implications are vast and wide, but I also know it is all complicated, and it takes a bit of patience to sort through. I won’t let these topics go, so you don’t need to absorb it all by kickoff time Sunday. =)

Speaking of which, enjoy the weekend ahead, reach out with any questions or feedback, and thank you for your trust in The Bahnsen Group. We will never, ever fail to be trustworthy. To that end, we work. No deflation coming of that chief end.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet