Dear Valued Clients and Friends,

April 2 was Liberation Day, all right. It was a day that the shackles came off, and true freedom and liberation were found. It was a day that opportunity increased, that entrepreneurialism was stoked, and that many found their voice and the needed spark they wanted to better produce, better serve, and generate a better economic result for their clients, customers, employees, and stakeholders.

I am, of course, referring to April 2, 2015, when The Bahnsen Group was born. That is the Liberation Day I wanted to write about today, and the liberation I wanted to celebrate. It was, indeed, the beginning of a ten-year journey I have plenty to say about. But, alas, my planned topic for today’s Dividend Cafe has been replaced by the other “Liberation Day” that took place this week.

To set the table before we dive in here. It was Wednesday, after market, that President Trump made his announcements about his Liberation Day at the White House. It was Thursday that the markets dropped the most they have dropped in a single day in nearly five years (when the world was in global shutdown). The video and podcast of this week’s Dividend Cafe were recorded after the market closed on Thursday afternoon. This written commentary was submitted Friday morning just as the markets were opening, down another 3% or so across the board (well over a thousand points on the Dow). So, all I can do is assume that by the time you are reading this, markets are down another 3% or so. It could be more; it could be less. But keep that state of affairs in mind as you are reading – a market down, and going down more as we enter Friday’s trading session.

It wasn’t a tough call to make – to skip my planned Dividend Cafe about the highs and lows of The Bahnsen Group’s ten-year journey and all the gratitude we have for our clients, our team, and the doors God has opened for us over the years. That topic sounds lovely right now, but we are in an utterly bizarre and self-induced market turmoil moment that requires commentary and attention. And it also requires a response from you as investors. Jump into the Dividend Cafe for all of that and more. These are the times for which we work.

|

Subscribe on |

A recap on what was done on Liberation Day

The tariff announcement on Wednesday afternoon amounted to a “worst of all possibilities” scenario for markets, first by representing far more draconian costs than previously believed and second by leaving open significant uncertainty into the future around implementation.

The President announced the following tariffs:

- 10% baseline on all imports – not based on fairness or reciprocity – just a baseline no matter what

- Mexico and Canada were exempt here, but they now have a 25% tariff on non-USMCA products

- 25% auto imports from any country in the world – parts and automobiles – covers half of all cars sold in the United States (this was announced last week and reiterated on Wednesday)

- 25% on all steel and aluminum imports from all countries – this was announced in March

- And then, “reciprocal” tariffs that ended up not being reciprocal at all. What they did was assess a U.S. tariff rate on imports from countries based on their trade deficit with us, divided by the level of imports we bring in from them. The President had said for months he wanted to impose tariffs based on “fairness” and “reciprocity,” but in the end, it became based on the difference between what we buy and what we sell, and not their costs imposed on us. In what has to be one of the most disappointing things I have ever read from a White House official, they conceded that the process was driven merely by who we buy the most from:

“The numbers [for tariffs by country] have been calculated by the Council of Economic Advisers … The model they use is based on the concept that the trade deficit that we have with any given country is the sum of all unfair trade practices, the sum of all cheating.”

- This results in massive increases in tariffs on Swiss imports, who has virtually 0% tariffs on us. In fact, Switzerland’s new tariff rate will be higher than the rest of the European Union, where other tariff costs on our exports are higher.

- It results in huge tariffs on imports from Vietnam (clothing, footwear), who also has very low tariffs on us, but who sells us 10x more than we sell them (you may have heard that we are a bigger and richer country)

- It results in massive tariffs on South Korean imports, who has less than a 1% tariff on us.

- When all is said and don,e it equates to a 34% tariff on Chinese imports, a 24% cost on Japanese imports, and a 20% cost on European imports. Of course, based on sheer volume alone, the most significant component is the Chinese tariff.

What was not done on Liberation Day

We did not come out of it with real clarity, and in fact, “full modification authority” was left with one single person, the President. This discretion is what I predicted last Friday would be the primary outcome. Vice President Vance is very transparent about how this is all being done:

*Wall Street Journal – April 3, 2025

*Wall Street Journal – April 3, 2025

Secretary Bessent said on Thursday, “let’s see where this goes” – not exactly the stuff of certain, firm clarity.

I cannot even put into words the volume and hysteria of calls the White House is getting, pleading for exceptions, waivers, exemptions, delays, and carve-outs. There are a few days until some of these tariff changes are implemented. There is simply no way to know what will end up actually happening, how quickly it will happen, and what the potential for adjustments will be. The uncertainty was not resolved on Liberation Day.

So the double whammy evidenced in markets Thursday and Friday: Bad news, and Uncertainty.

Cost in Dollar Terms

The announced tariffs represent a tax to the economy of over $400 billion, which equates to 1.3% of GDP. This is well over 10x the cost of the 2018 tariffs. It represents the largest tax increase in the American economy since 1968.

Two can play at this game. Or Two Hundred.

China announced overnight that it will retaliate with tariffs of its own (a 34% levy on all U.S. imports). Companies with large exposure to China feel it the worst, but it is contagious throughout markets because no one expects China to be the only country to retaliate. China will buy energy and agriculture products they are used to buying from us from someone else. Tit for tat and all that.

Europe and Canada will soon be making their own announcements regarding retaliatory tariffs of their own.

Law and Order

Many have asked how the President can unilaterally impose tariffs since the power to tax is given to the Congress in the United States Constitution (Article I, Section 8, Clause 1), and since there was once a time that a bunch of colonists got really, really mad at a King for imposing taxation without representation. It is not a question I can give a good answer for because I do not have one. The President has used Section 232 of the Trade Expansion Act of 1962 to claim that many of the tariffs are necessary for national security. He has the right for temporary, emergency tariffs if an “import surge” is being responded to under Section 201 of the Trade Act of 1974. Congress has legislative ability to restrict and intervene in all of these excesses or implementations, but let’s just say that Congress has not seemed very willing to jump into all of this and, well, be a Congress.

A conservative legal group, the New Civil Liberties Alliance, filed the first lawsuit today. I expect many more lawsuits in the days and weeks ahead challenging the Constitutional legality of some (not all) of these tariffs, and I expect that to add to the uncertainty risk premium in markets.

Impact

I am a little blown away by how much my phone rang this week, not from clients panicking about the market, but from business owners in severe distress over the impact to their business. It seems that for some reason I can’t quite make sense of the impact to large, publicly-traded, multi-national Fortune 500 type companies is supposed to just “not matter” to us (as if their employees and stakeholders are not worthy of consideration), but generally speaking, most Americans still seem able to hold their emotional and logical sympathies in place for small businesses. Take note of this particular communique I received, printed verbatim, from a business owner who also informed me that he voted for President Trump (just to make clear his concerns do not reflect a partisan hostility; quite the opposite):

“As a business owner (and a majority US manufacturer/exporter at that) our estimate right now is a direct cost of about 10% of revenue only taking into account direct cost and not run on effect of suppression of the industry and economy as a whole or lost sales due to retaliatory tariffs which is already happening. We run 15% net margins on a good year. Devastating doesn’t begin to describe the effect. We will mitigate but that will be expensive in its own right. I employ 40 people, we 60% export and about 60% of our cogs we manufacture in house or are purchased domestically. The remaining 40% are sourced globally largely Asia. It’s exhausting and demoralizing to have spent more than ten years building a business, survive covid craziness and finally really be hitting our stride as an organization and end up here. The cost of this is about 50% of our annual payroll expense, so it’s that much less cash flow I have to increase payroll which we are working extremely hard to do in an ever more expensive and restricted labor market.”

I have already written of the devastation this has done to small business optimism. I think this will prove the Achilles heel of this in terms of economic impact and broad popular response … The stock market impact is one thing; the devastation to small business is another.

I am reading all the same reports you are about anticipated hits to GDP and to CPI. Apollo released a report this morning estimating a -1.5% contraction in GDP and a +1.5% increase in inflation. Others are near those estimates. I take it all with a grain of salt. What I know is that production is coming to a halt, global trade is in a near freeze, capital goods orders are evaporating, and the clock is ticking for those things to not do significant damage to Q2 and Q3 economic activity.

Motivation, Intent, and Outcome

I do not believe President Trump wants to ruin the American economy. I actually do not believe we have had a President who wanted to ruin the American economy. I think we have had Presidents who advocated for policies and who implemented policies that have done bad things to the American economy because their intent was different than the outcome. This is often because of bad advice:

- President Nixon – Wage and price controls would really help improve prices for the middle class.

- “President Bush – The American people will not mind you raising taxes; ‘read my lips’ was campaign talk.

- President Obama – The need of the hour is a $800 billion stimulus spending bill that will bring unemployment immediately down.

- President Biden – The decision to get Americans more cash even after the last few COVID bills will prove to be inconsequential to deficits and prices.

In all cases, I think these four Presidents got really bad advice, and made really bad decisions, and suffered really bad outcomes. In all four cases, I think the outcomes were predictable. And in all four cases, I think the motivations of the Presidents involved were not the problem. Many people, including Presidents, politicians, advisors, legislators, think-tankers, pundits, and more, operate from either very “flexible” principles and beliefs or from wrong principles and beliefs. And in this case, I believe President Trump has one fatal belief driving him, combined with some really bad advice coming to him. That fatal belief is that trade deficits inherently reflect something unfair. That bad advice is that we can somehow re-order the entire global trading system with top-down central planning and taxation.

Once more for those in the back

The expectation that tariffs were coming to “even the playing field” had not scared markets that much because there are not that many inequities in trade conditions; as if there were, wait for it, the trade would not happen. That the rationale would turn to simply what the trade deficit is with a country, predicated on a belief that any gap between imports and exports inherently means cheating could never have been comprehended. What I believe readers need to understand is that …

- We run a massive trade SURPLUS with the world when it comes to SERVICES – hundreds of billions of dollars.

- Yes, we buy more goods from the rest of the world than we sell to them. We are a richer country and so have more money to spend on goods.

- Trade deficits go down when we have recessions. Most have not historically seen that as a good thing.

- A trade balance between two countries (let alone between one country and the entire world) is a by-product of a million things, primarily the individual decisions of millions of people and companies. Attempts to centrally plan or micro-manage such from elites in positions of power have not historically ended well.

- U.S. cost of production could be decreased with lower taxes and regulations and greater competition. It cannot be decreased with higher input costs and downward pressure on global trade volumes.

The question in front of us

I am surprised by how many people continue to believe they know what President Trump is going to do in the weeks or months ahead. Because I happen to know that he doesn’t know what he is going to do, it is odd to hear so many so sure that “he is going to back down and reverse course” – or “he is never going to back down and take an off ramp.” In both cases, the people asserting so are projecting their own frustrations or opinions, or, in the best case, making a prediction that has a 50% chance of being correct (because of how coin flips work).

Here is what I know about President Trump: I believe there is a pathology at play that observers would be wise to think about psychologically, and not ideologically. Does his compositional make-up fear being told he capitulated if he “finds an off ramp?” I think that’s a fair question. But on the other side, is he predisposed to not liking the idea of a “Trump recession” or “Trump crash”? Also seems fair. It seems to me a non-partisan, objective, reasonable thing with what the American public knows about President Trump (those who love him, those who hate him, and those in between) that there could be a scenario where his psychological motivations push him to double down on this, and there could be a scenario where they push him to seek an off-ramp, and those psychological motivations are the same in both possible scenarios.

I can’t see how this is either a compliment or an insult, nor how this is all that controversial. I also can’t see how anyone believes they know which way the wind will blow on this. I think it is a fair binary construction of the matter at hand, and I think it is unknowable for investors. I appreciate those who are so sure they know what he will do (or not do) next. I apologize for not believing that you do.

Bottom line

There are going to be days in the weeks ahead that rally, if I were a betting man. There will be more downside volatility. There is a lot of uncertainty. There is a greater chance of recession than we have had. There is a political fallout or consequence. There are all sorts of things that, for some, will be good sport, some will be aggravating beyond words (I took the test open book), and some will be confusing. And none of it justifies abandoning an investment plan, believing one can time or predict the market or the outcome, or attempting to game any of this with panic selling (or panic buying).

I just can’t say it any simpler than that. It is THE undisputed lesson of market history: Those who tell you how and when this will play out for investors will be wrong. Exit timing and re-entry timing are fool’s errands. Receiving growing dividends through the entire process are the rewards for investors who took on that risk-reward trade-off. No one likes this level of market price volatility. I may know deep down that, mathematically, these periods make money in the end for patient, disciplined, properly-invested investors, but I also know that they are emotionally challenging for many people along the way. I say that with a lot of experience, and a lot of empathy.

Don’t do this by your gut. That doesn’t seem to be a good plan for anyone. The disciplined plan and philosophy you had is the one you should have. I want to say that to clients, investors, and readers, and candidly, I want to say to it to a lot of other people these days, too.

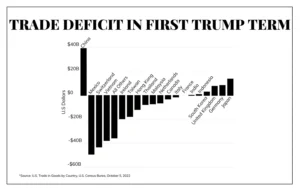

Chart of the Week

In the first Trump administration, we did change the trade balance with China by $40 billion, but then just saw it go the other way with Mexico, Switzerland, and Vietnam. Changing trade dynamics move chess pieces around, but central planners are limited in what they can do to manipulate outcomes exactly the way they want.

Quote of the Week

“If you don’t have a competitive advantage, don’t compete.”

~ Jack Welch

* * *

I really wish I could have written about April 2, 2015, this week. Our move to liberated independence was one of the greatest things we ever did for our clients, our team, our people, and our love of this business. But duty calls, and I hope you got the information you needed this week to watch the Final Four in peace this weekend. This, too, shall pass. But it will be a bumpy ride along the way, we know. So that end we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet