Dear Valued Clients and Friends,

In a sense, this week’s Dividend Cafe is one long “Ask TBG” because this is a topic that I have been getting a lot of questions on for quite some time, most of which overlap with each other in some way or another. There is no question that the #1 way in which most Americans have exposure to the U.S. stock market is through an S&P 500 index fund. Index funds (passive vehicles meant to capture the return of an entire market or market index) have exploded in popularity over the last ~20 years. It is the right time for me to dedicate a whole Dividend Cafe to this subject.

You would be forgiven for assuming that what I want to do now is use the Dividend Cafe to make a case for the active management of dividend growth investing vs. the passive approach of index investing. I do speak to this subject quite a bit (here in the Dividend Cafe and elsewhere), but that is only going to be tangentially addressed today. I actually have a different agenda in mind.

My objective in this week’s Dividend Cafe is less about talking my own book and more about exploring the impact on all investors from index investing, even those who do not practice index investing. I get questions all the time asking if the flood of indexing gives markets a permanent and growing bid that can only make it go higher (speaking of someone talking their own book). I get other questions, wondering if the large increase in index investing presents systemic risk (to all of us). And still others want to know what the advantages and disadvantages of indexing may be.

All are valid questions, and all are going to be addressed in this week’s Dividend Cafe. Whether one believes in indexing as the be-all and end-all of their equity exposure, or not, one thing should be abundantly clear when you are done: For good or for bad, today’s indexing is not the indexing that existed 20 years ago.

Let’s jump in to the Dividend Cafe!

|

Subscribe on |

Steel-manning the argument

Even for active investors like us, it is very easy to make the case for index investing. As a matter of basic pragmatics, buying an index fund gives the investor a diversified equity portfolio at a very low cost. It eliminates the discussion of “outperforming” or “underperforming” the market in a given segment of time, and just accepts the “market return.” Since you may have heard that, over time, “market returns” are pretty darn good, receiving the market return at a low cost can be a very good thing. Basically, “beta” does not cost a lot of money, and a Beta of 1.00 to the market can always be bought cheaply by, well, buying the whole market.

What is often missed

Many people talk about “under-performing” or “out-performing” the market in the context of an apples-to-oranges comparison (and sometimes an apples-to-carburetors comparison). Their portfolio may have a good portion of large-cap U.S. stocks, but they also own, say, bonds, real estate, or other diversifiers that are intentionally designed to decrease the volatility of the portfolio. That kind of portfolio design is supposed to under-perform the market when it is screaming higher (that investors owns less of the “best-performing” thing), and to out-perform the market when it is hemming and hawing (as it will do every year at one point or another in that year), and as it will do to great effect, on average, every five years). People can agree or disagree with the decision to decrease the volatility of the portfolio relative to the whole market, but when that decision has been made comparing their portfolio to the whole S&P 500 is like wondering why you are not burning as many calories running three miles as someone else is running five miles… it, is, math (I just made that analogy up as I was typing so if I come up with a reason later why it doesn’t work, I’ll recant it; for now I am sticking with it).

If an investor had no income goal, no timing goal, no consideration of downside volatility comfort, and basically was just a robot whose sole investment objective was “give me the return of the S&P 500 at all times for as low a cost as possible,” an S&P 500 index fund would be hard to improve on. I have found that many investors have a lot of goals besides that one, and I refer to those investors as “human beings.” But I will state until I am blue in the face that the S&P 500 has delivered a market return since Kingdom come, done so with minimal add-on fees, and has done so with no need to discuss what is doing well and what is not doing well. I get why a lot of investors like it, and I certainly get why a lot of advisors want to use it.

This fee thing

Now, before I forget, most investors who own the S&P 500 in an advisory relationship are getting the index fund for “very cheap” (not quite totally free), but they are rightly paying for the relationship. I would presume that if they continue to pay their fee, they are happy with the value they are getting that comes with their ownership of the S&P 500 index fund, and the services that the advisor provides (financial planning, estate planning, or most importantly, behavioral advice in those times of market distress). There are a lot of services that good wealth firms can offer, which make their fee worthwhile, and I can’t speak for how all firms present and deliver their value proposition. Many investors might own the S&P 500 outside of an advisory relationship, and in that case, they are, presumably, investors who trust themselves to avoid bad decisions in key times. Human nature is a very, very bad investor, and the advisory profession is supposed to exist to keep investors from doing the wrong thing at the wrong time. This vital part of a value proposition can (and should) exist regardless of what the portfolio management approach is.

At my practice, we actively manage money, incorporate multiple asset classes into our portfolio management, and make buy and sell decisions around dividend growth equities in-house. We employ a wide array of analysts, traders, and portfolio analytics personnel, and invest in a significant investment infrastructure for this to be a part of our client experience. It costs us millions of dollars per year to run. But we do not charge more for it. Whether we were using index funds or the active approach we utilize, our fees would be the exact same. We are charging for a very deep and sophisticated level of planning, of tax and estate work, of a custom asset allocation to truly align each client’s unique situation and goals with a bespoke portfolio, and most importantly, to serve as the ballast that is needed in times of temptation (whether to panic or euphoria). So while we charge fees for our advisory services, our fees are not higher or lower than they would be if we presented clients with an entirely “index” oriented strategy. We manage money the way we do because we believe in what we are doing to our dying breath. Our fees are not higher than those of an advisor who presents an index approach, but the margins to us are certainly lower. That is a business decision I made – to invest in and financially support an investment infrastructure that enables us to do what we believe in. I actually didn’t have a decision to make – there was never, ever, ever an option of doing anything differently. I bring it up to make clear that we are not talking about “fees for investment” vs. “no fees for investment.” We are talking about “fees for advice, with an active approach” vs. “fees for advice, with a passive approach.” The only way to get around the fees in this whole thing is to go for the “no advice” route, and we haven’t found that to go very well for most people in our time on earth. In fact, to that very end, we work (and work and work and work).

Back to the subject at hand

There are very few investors who only own the S&P 500. It inherently contains more volatility than many investors are comfortable with as a 100% weighting in their portfolio. It lacks exposure to other asset classes that many investors [rightly] feel would enhance their portfolio. Since many investors have some form of income or cash flow objective, a yield of barely > 1% doesn’t cut it for a lot of people. There are plenty of reasons investors may want to own something besides the S&P 500. So the fact that so many portfolios are compared exclusively to the S&P 500 when almost no one owns “just the S&P 500” is odd, and frankly a bit irrational. That said, per the opening paragraph above, the low-cost, easy, highly liquid, diversified nature of the S&P 500 index fund makes it a widely-owned option for most investors, whether it be their whole portfolio, a large portion of their portfolio, or just a portion (of any size) of their portfolio. And these options (whole, large, some) can exist for investors with an advisor, or without.

Okay. I think my introductory thoughts are now out of the way.

What has changed and why

Let’s start with the sheer change in size. In the late 1990s, the total assets in all S&P 500 index funds were $280 billion. The famous S&P 500 ETF, ticker: SPY, had launched in 1993 and by 1999 had a whopping $20 billion of assets in it (which by the way, was whopping; now it is Nvidia’s monthly coffee cart budget). Fast forward to today, and SPY is $675 billion in size, and total S&P 500 index funds are $3.7 trillion in aggregate size (combining ETFs and mutual funds). Note, this is only S&P 500 index funds – not all index funds that seek to replicate other market indices or specific sectors, etc.

Now, some astute readers may be thinking, “Well, no duh, the S&P index funds are larger now – the market is up big!” And alas, that is true… The market cap of all S&P 500 companies put together 25 years ago was $14.3 trillion, and it is $56.9 trillion now, so the market is up 4x in nominal terms. But the growth of the index market is over 13x !!! Market appreciation doesn’t even come close to covering the explosion of size in indexing.

The growth in size can be explained by a handful of factors. First of all, ETFs themselves became a very friendly vehicle for exposure to index ownership. Mutual fund index vehicles existed before, but ETFs provided greater access with lower costs and significantly reduced friction. In short, American capital markets and our obsession with never-ending innovations and efficiencies (I could not possibly be saying this with more enthusiasm and excitement) paved the way to better index replication, easier ways to access these improved products, all at a lower cost. So yes, it became more popular!

I also believe that the post-GFC dynamic gave way to an increased appetite for passivity. Active management in the 1990s was largely focused on heavy concentration in (wait for it)… technology… because (wait for it again), that was what was performing well. So active managers piled into the best-performing and most popular stuff, and when that popular stuff blew up, active managers were left blown to smithereens on the floor (next to the remains of their investors and their former portfolios). I suppose this dynamic repeated itself in the 2000s as a lot of the top-performing managers and funds post-dotcom and pre-GFC were heavy in financials, housing, mortgage, and related sectors, and then, well, 2008 happened.

In other words, managers’ propensity to chase fads led to them doing really well until they blew up, and it led to a lot of investors saying, “can’t I pay less money to NOT blow up?” After the two implosions to start our new century, the low-cost, less-concentrated, less-human fallible dynamic of index ownership made a lot of sense. But then something really, really profound happened: The post-crisis bull market.

Call it ZIRP (the Fed holding rates at 0% for 14 years).

Call it QE (the Fed adding $4 trillion to its balance sheet and consequently to the financial system’s reserves, and another $5 trillion after COVID).

Call it financial repression (where real rates were negative for most of the last 17 years – that is, interest rates net of inflation have been a negative number, highly incentivizing people to move up the risk curve to achieve a positive real return on their capital).

Call it earnings recovery, where earnings across the S&P 500 were $50/share in 2008 and are $270 now (this is, of course, the real story of markets).

Call it ~16 years without a recession (the COVID anomaly notwithstanding).

But no matter what you call it, call it an unprecedented period of earnings growth, multiple expansion, and market performance that was captured in index ownership with slightly lower-than-average volatility.

The biggest changes of all

I have written about this over and over and over again, and I don’t see any reason to stop now. The top ten stocks in the S&P 500 right now have a 40% weighting in the basket of five hundred stocks. The S&P 490 is 60% and the S&P 10 is 40%, if you follow me. Nvidia is roughly 7.5% of the market, Apple and Microsoft are over 6.3% each, etc. This is double the weighting that the top ten companies represented twenty years ago, and quadruple what they represented forty years ago!! Yes, in 1985, the top ten companies were 10.5% of the market. In 2005, it was just over 20%. And here we are at 40%.

It is perfectly legitimate to argue that having ten companies be 40% of a 500-stock portfolio is a feature, not a bug. It has obviously been a feature for the last three years.

It is perfectly legitimate to argue that having ten companies be 40% of a 500-stock portfolio is a bug, not a feature. It presents an entirely different concentration and valuation risk for markets. The 23x P/E ratio of the market would be < 20x if the top ten companies were 25% instead of 40% of the market (and that would also align their projected earnings to their weightings, I might add).

But what is not legitimate is to argue that this dynamic is not different. Whether it is good or bad, it is different. And investors ought to know that.

Is index ownership driving index value?

Are the indexes driving these “big ten” names higher, or are those big ten names driving their weightings higher within the index? The answer is yes, and that is the only intellectually honest answer. The volume being bought in indices is proportional to the market cap of those companies, and that valuation is not set by the weighting… the weighting is set by the valuation. The chicken and egg here is far easier than people realize. Now, having received a high valuation, do market functions (like passive equity purchases) help to support and sustain? Yes, they do – until they don’t. And this is where I wish people could just “keep it simple.” Volume does not drive price one way. If you believe volume sets price (“it ultimately does not” – Ben Graham, Warren Buffett, and all smart people), then you have to believe that in good and bad markets. It would just mean that whatever “exacerbation effect” you are describing in a bull market works in perfect reciprocity in bear markets. But it misses the point that the value set on a given company is ultimately a by-product of that company’s earnings and the market sentiment around that company’s earnings. Index volume has to match that price, but it does not set the price. And if it did, then how do we ever get changes who are atop the leaderboard? Wouldn’t the market dynamics hold the leaders in that position forever? The fact of the matter is that it has never worked that way, and never will.

Is there systemic risk?

Plenty of work exists exploring the impact heavy indexing has had on overall financial markets. That indexed trading has pushed correlations amongst stocks higher seems perfectly logical to me (we call this convergence of beta, but essentially it means that the correlation individual stocks have to the overall market has gone higher). But there is also ample evidence that, well, this is not true when it is not true. In other words, through this period of a 13x increase in index ownership, there have been periods of greater idiosyncratic dynamics that “bucked that trend” – and anything that is only true when it is true is not true. The fact of the matter is that passive indices own 30% of the market, which means that 70% of the market is outside the forces of index activity… But more importantly, index buy/sell volume is only 5-10% of daily trading volume, soaking wet. Price discovery is dominated by traders, hedge funds, arbitrageurs, and a wide variety of market actors with entirely different objectives than index funds. And while correlations have always, always, always tended to go very high during bad markets, moments of idiosyncratic risk (and reward) are no less prevalent now, with > $3 trillion of S&P 500 market cap than they were when index investing was embryonic.

The more compelling argument around systemic risk is that in periods of heavy selling (significant drawdown events for markets) there is liquidity and redemption risk that can impact all of markets. When I say that it is compelling, I mean that it is structurally sensible to think there could be execution hiccups. Many asset classes have been subject to much more structurally challenged circumstances than large cap equity over the years in times of true dislocation, and having lived through those moments many times I remain of the opinion that… (a) they only get better over time (bid-ask spreads compress, more liquidity comes each time there is a drawdown, these dislocations end quicker than they used to, AND (b) I couldn’t care less. I believe the freeway remains a dangerous place to go sit and write Dividend Cafe, but I have done a good job over the years writing Dividend Cafe at my desk, and not sitting on the freeway. In other words, whatever market dislocations people fear being exacerbated by market function breakdowns in times of poor liquidity or market function, these are not dislocations I have any intention of ever trying to sell into. There is no trademark or patent on that last sentence – put it to work in your own life and portfolio.

In all thy getting, get this

I don’t believe there is a better way to summarize the possibility of higher systemic risk from increased indexing than this: It is very likely that if I do something really stupid in a period of market dislocation now, the consequences will be worse than if I had done something really stupid in a period of market dislocation in past periods. I do not know that this is true, but I am 100% willing to believe it is. But re-read the sentence and see if you can’t come up with a solution.

The entirety of concerns people bring up around increased systemic risk from massively higher indexing all refer to some degree of trading risks, of mechanical risks, of liquidity risks, and of operational risk. I am sorry, but those are not risks for the disciplined, long-term, prudent investor. And they sure as you-know-what are not risks for a fiduciary advisor worthy of the name.

Do I think 23x as a forward P/E ratio for the S&P 500 is expensive? Yes, I do. Do I believe that forward returns are historically more attractive when bought at lower valuations, which is to say that forward returns are historically less attractive when bought at higher valuations? Yes, I do. So valuation and concentration are risks I respect and recognize. But they are not systemic in the way that term is being used – they are risks (and rewards) for those who own such in such a way.

Conclusion

Index funds have exploded in popularity over the last ~25 years for some good reasons and some not-so-good reasons. Along the way, they have changed a great deal. The changes are not ones that present systemic risk concerns for all equity investors, provided those equity investors behave themselves. Rather, they are changes that have, for good or bad, dramatically changed the risk-reward characteristics of the index itself. We at the Bahnsen Group are less concerned with these things because we have a particular investment philosophy that is focused on something different than market beta and expanding P/E ratios. Valuation becomes an intensely important part when devoted to passive market ownership. Earnings growth will ultimately carry the broad market, and that volatility profile should be understood by all investors who go that route. Dividends become a much less important part of return when one is index-focused, and that is not how we want to be invested. But the idea of a technical vulnerability in markets because of heavy index activity and ownership is mythical, and to the extent it ever produced a cog in the machine of markets for a day, or two, or thirty, we couldn’t care less.

Neither should you, no matter how you are invested (active, passive, dividend growth, what have you).

Noise comes and noise goes, as do all investment fads.

But cash flow is forever.

To that end we work.

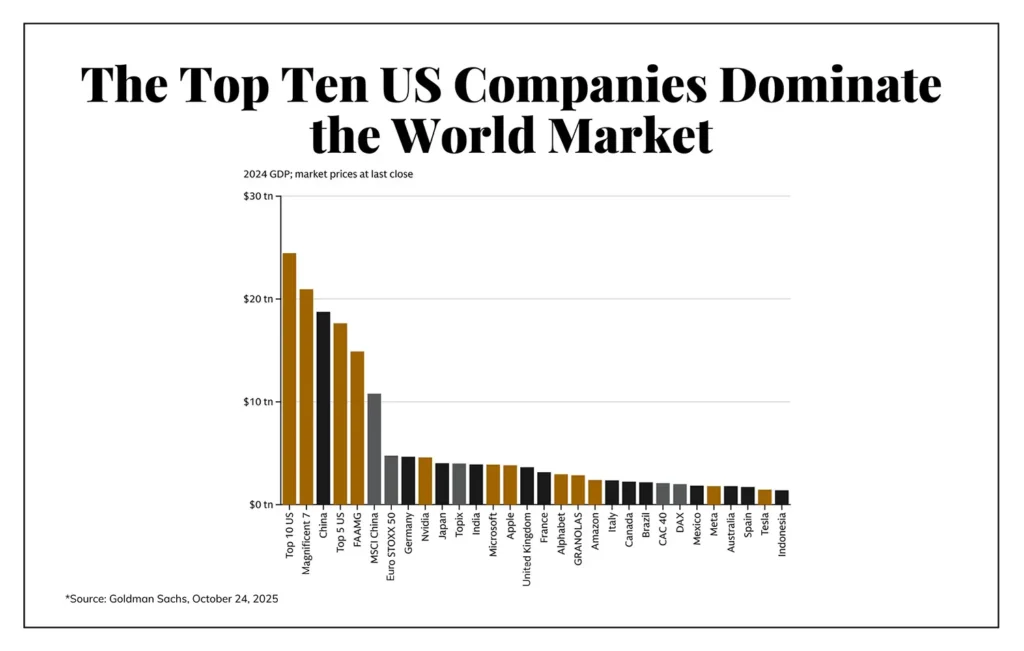

Chart of the Week

What could go wrong?

Quote of the Week

“In the long run you want to be an owner, not a lender.”

~ Barton Biggs

* * *

I went way longer than I intended with this, but I enjoyed writing it, researching it, and presenting it. I hope the takeaways are as clear as I intended them to be, but if you are struggling to understand what to do with them, feel free to ask. And better yet, if you are not a client of our practice and want a second opinion on what you are doing with your portfolio, don’t hesitate to ask. We are never, ever, ever going to push for anyone’s business – we are doing just fine (and that is doubly true if you have a good advisor already taking care of you). But if you want a second opinion on whatever it is you do have, and don’t want to be sold anything after asking, you can do worse than hitting the link above.

In 17 years of writing this weekly screed, I don’t think I have ever put that out there. But there you go. =)

Back to California from NYC tomorrow, with a whole week in the California office ahead. New York autumn will be hard to leave, even for a short period, but duty calls. Have a good weekend, all.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet