Dear Valued Clients and Friends –

The markets rallied substantially today as the Friday threat of renewed tariffs with Europe was pushed aside on the Memorial Day holiday. Today’s is a pretty simple breakdown around the horn, so check it all out.

Dividend Cafe on Friday looked at the new “big, beautiful” bill, the deficit implications, and the real truth about the bond market’s messaging. The written version is here (my favorite), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

- The market opened up +300 points today after the long holiday weekend and steadily moved higher throughout the day.

- The Dow closed basically at the high of the day – up +741 points (+1.78%), with the S&P 500 up +2% and the Nasdaq up +2.48%

*CNBC, DJIA, May 27, 2025

- Credit spreads remain so low that it is just very hard to panic about any disturbances in equity volatility or even prolonged economic fears. Widening credit spreads would become much more illuminating if and when they happen.

- The ten-year bond yield closed today at 4.45%, down five basis points on the day. If last week, the 10-year moving up a few bps meant “the world no longer has confidence in American treasuries,” then I assume today’s action means the world now has confidence again, right?

- Top-performing sector for the day: Consumer Discretionary (+3.04%)

- Bottom-performing sector for the day: Utilities (+0.77%) – so all eleven in the green

Top News Stories

- Putin and the Russian aggressors severely intensified their military hostilities in Kyiv and other parts of Ukraine this weekend, resulting in an exasperated if not surprised President Trump to tweet his disgust at Putin. It is being widely discussed that additional sanctions may now be imposed on Russia as a means of forcing Putin to the negotiating table.

Public Policy

- Obviously, all eyes now go to the Senate to see what they will do with the “big, beautiful bill” that the House has passed (and that I wrote about in Dividend Cafe on Friday). The Senate is widely accepted to make some changes, but not massive ones, and to end up accepting the bill. However, the public pushback from some high-profile Senators and even President Trump, himself, saying there are changes to his own bill he wants to see, makes me believe the bill may get better before it is out of the Senate

- For reasons that I cannot quite comprehend, the press has decided to barely cover the story that the President has done a U-turn on the Nippon Steel acquisition of U.S. Steel and is now allowing the deal to go forward. Labeling it as “investment” instead of “acquisition” is adorable, but the terms are essentially identical to what has been proposed all along.

- From one of the great macroeconomic/policy resources I have (h/t Corbu) regarding pending U.S.-China trade deal:

- Progress is being made for U.S.-designed semiconductors in exchange for China-produced metals and magnets

- Progress is being made on mutually agreeable steps regarding China’s efforts in stopping Fentanyl trafficking (which would take off this 20% tariff surtax)

- Wildcard issue in all of this: Cooperation from Xi in not supporting Putin

Economic Front

- Durable goods orders were down -1.3% in the month of April, far more than the expectations for a -0.2% drop. Capex projects are being delayed, but hopefully not cancelled en masse (behind the uncertainty of the tariff policy)

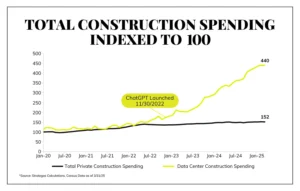

- The “data center build” story seems to be, well, rather important to present economic activity.

Housing & Mortgage

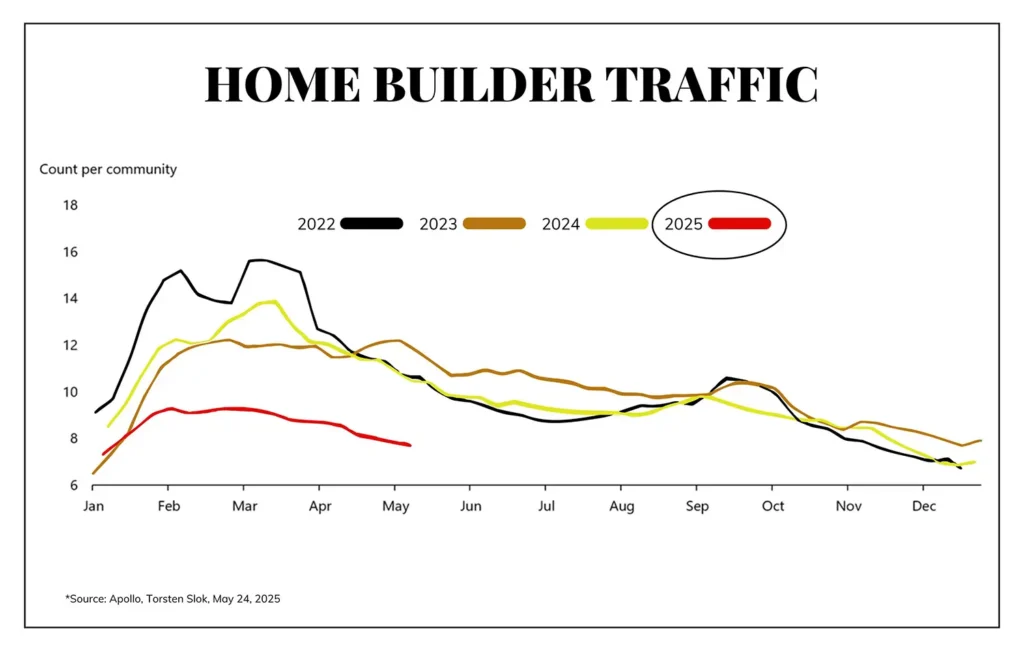

- Existing home sales declined -0.5% in April (to a four million annual rate) and are now down -2% versus a year ago (and a year ago they were way down from the year before level, which was down from the year before level).

- 2023 and 2024 were not exactly robust years for prospective traffic with new home projects, but look at how much weaker 2025 was, even compared to 2023 and 2024.

- President Trump chimed in for the first time in his new term, expressing support for Fannie Mae and Freddie Mac being re-privatized and removed from Treasury conservatorship. No plans or details are forthcoming, but it is interesting to me that he would even chime in on this so early in his term, when the issue is not one of critical importance to his agenda. I am hopeful it will prove to be a priority.

Federal Reserve

- Secretary Bessent said in an interview Friday that they will soon be altering the Supplementary Leverage Ratio, essentially treating treasuries as dollar-for-dollar credits in the risk-weighting formula for how bank balance sheet assets are treated. Why does this matter? It at least marginally and potentially significantly adds to bank appetite for buying Treasuries, which puts downward pressure on bond yields. The one thing I would say: Expect this to impact the shorter end of the curve a lot more than the long end!

Oil and Energy

- WTI Crude closed at $61.10, down -0.70% on the day.

- Midstream energy held up well last week, comparatively speaking, with stocks down over -2.5% and Crude down over 2%, the midstream sector was down just over 1%.

- Natural gas demand continues to present huge upside for pipelines, and financial flexibility remains strong across the sector.

Ask TBG

| “What if a material portion of the market that has poured trillions into shiny, flashy growth sectors suddenly found religion in dividend growth and shifted significantly into the dividend growth market? How would this impact TBG? I know you’ve sold off good dividend growing companies in the past that have become overvalued. What if this happened on a systemic level? Does TBG’s strategy rely on being contrarian?” ~ Adam V. |

| I would love this to happen, but human nature does not work that way. If individual companies become systemically and gruesomely over-valued we would find others that were not. If we get to a point where “there isn’t a single dividend-growing company in the world at a reasonable valuation or attractive yield,” please write me again, then. |

On Deck

- This Friday’s Dividend Cafe – what I would do in Dave-land about the debt, the deficit, and the need for more economic growth

Have a good Tuesday night, and let’s go Knicks!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.