Dear Valued Clients and Friends –

This week’s Dividend Cafe took a funny twist over the last 24 hours.

First, I ended up flying back to California from New York late Thursday night for a Friday matter that came up (I was supposed to fly to California on Sunday). This substantially altered my reading and writing plans for this commentary, along with work issues. On Thursday the market had a little reaction to the shocking – shocking – news that the Biden administration was looking to raise capital gain taxes on high-income brackets. I say “shocking” because it had been, well, you know, on their campaign website all of last year, and discussed and mentioned 37 times since his inauguration. And because nothing in the announcement came with Bernie Sanders replacing Joe Manchin in West Virginia or Elizabeth Warren replacing Kyrsten Sinema in Arizona.

And by the way, as of press time Friday morning, the market is down a whopping ~150 points on the week – a rounding error – after a few up days and down days mostly offset each other this week.

Still, though, the cap gain tax issue does matter, so I wanted to address it this week along with a few other things that seem to be a source of worry right now for many investors.

But you can’t spell “investor” without “t” and I found that out the hard way when I arrived at JFK’s Admirals Club yesterday and the “t” button on my keyboard was not working. I had a DC Today to finish, and ambitious plans for 5+ hours of work on a cross-country flight. Well, I did all I could, but just so you know, a lot of words in the English language have “t” in them – a lot. And doing a “Ctrl-C” and “Ctrl-V” for all your T’s is enough to make someone want to ask for the bartender (I don’t drink, so had to settle for my typing productivity being, well, diminished).

But the use of an iPad Bluetooth keyboard, a munted attempt with the munted keyboard, my desktop at my California office, and a brand new Surface Pro laptop I had overnight shipped the second I discovered the trouble have all coalesced together to make this Dividend Cafe possible. And to think my dad wrote 500-page books on a typewriter!!!

Jump on into the Dividend Cafe!

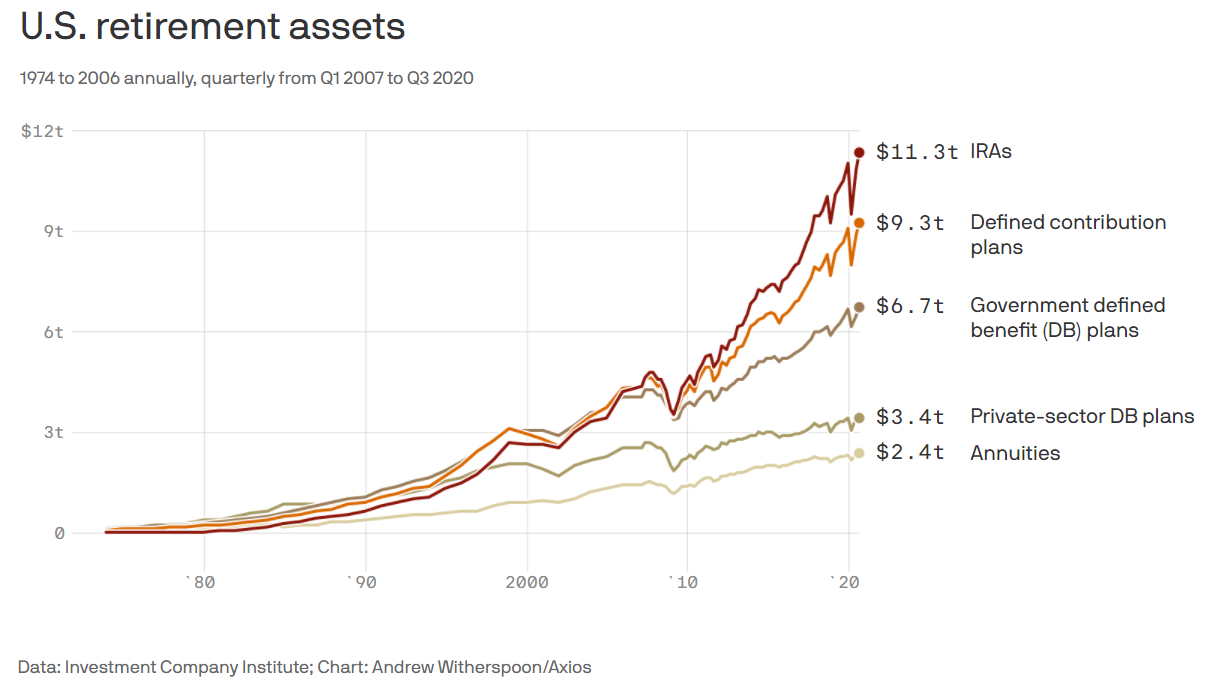

Off the bat – $33 trillion not subject to tax increase

If a doubling of the capital gain tax were to actually pass and become law, it certainly would be a negative for markets (I am highly skeptical it can pass as proposed, but we’ll leave that alone for now). How much of a negative is a legitimate subject for debate. A significant ownership of stock market is in non-taxable account categories (IRA’s, 401k’s, pensions, endowments, foundations, etc.). As in $33 trillion worth …

But it is not good …

The two major problems are this: (1) Obviously after-tax profits for those subject to the tax are now less; that gives less incentive to invest and less capital to reinvest, meaning less capital formation. But the far bigger problem involves all other investors, and worse, other businesses … And that is the huge incentive there will be now for “stale” assets. Not selling an asset that should be sold because of aversion to tax consequence is just as distortive to markets as selling an asset that shouldn’t be sold for some unproductive reason. Not allowing natural market forces to function where economic actors sell what they believe should be sold and then reinvest in new arenas they believe should be invested in leads to sub-optimal capital allocation – period.

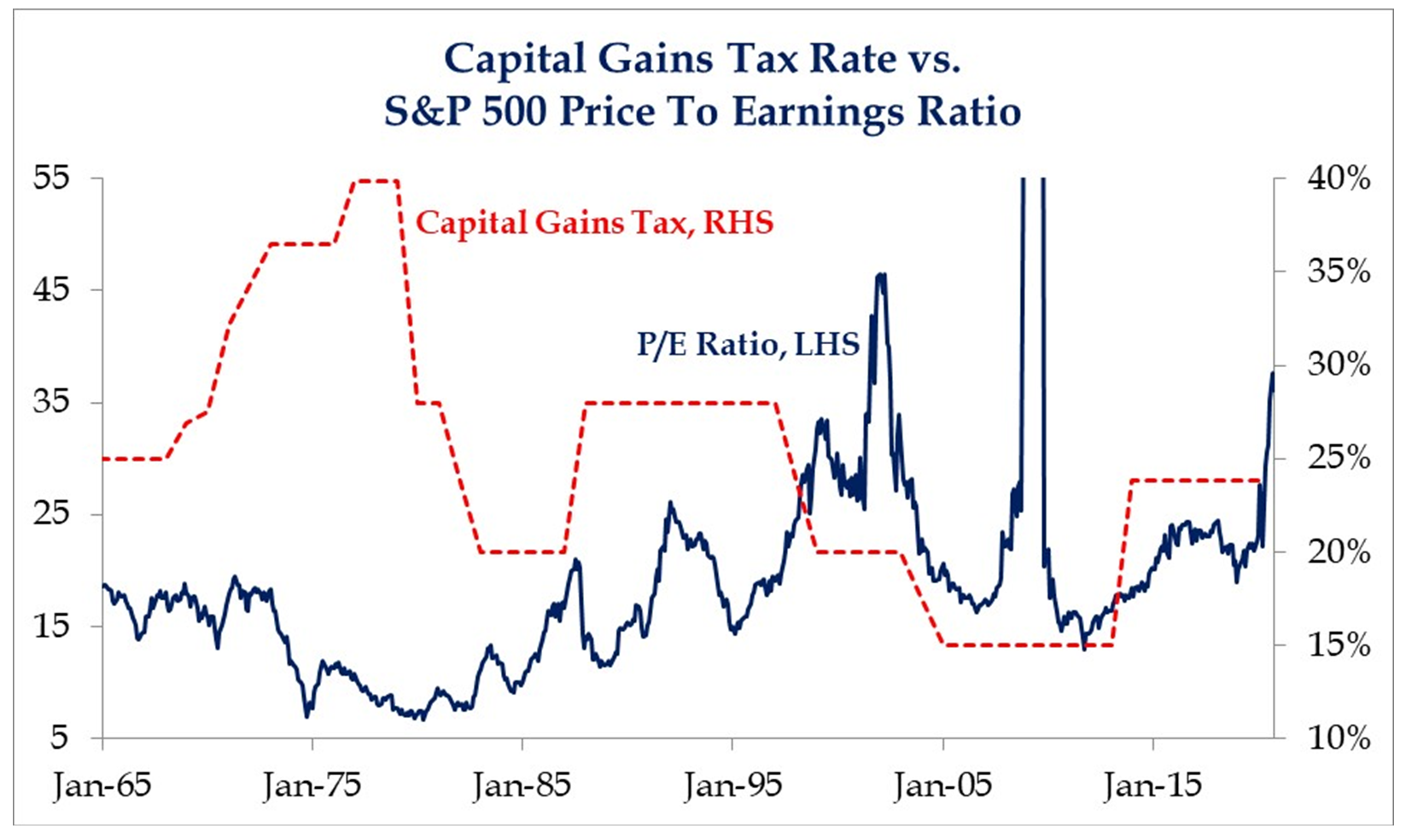

Most effected?

On a relative basis, the greatest short-term vulnerability IF cap gain taxes were to be increased is where the return is most dependent on multiple expansion. On the margin, and all economic impact has to be understood in the margins, higher cap gain taxes diminish the price/earnings ratio. High P/E stocks have the most to lose here, assuming the proposed policy were to really be enacted, and relative to other categories of risk assets.

*Strategas Research, Daily Macro Brief, April 23, 2021

Putting cap gain tax worry on my list as a portfolio manager …

It’s on my list, but it is not at the top of my list. But candidly, much of that is because I don’t believe they can do some of the worst things they want to do (due to political realities). My views on the deleterious impact of higher taxes on capital are not primarily about the impact on individual investors but rather the impact to forward-economic growth. Well over a decade of sub-trendline economic growth is no time to be taxing more of something that we need more of (i.e. capital investment).

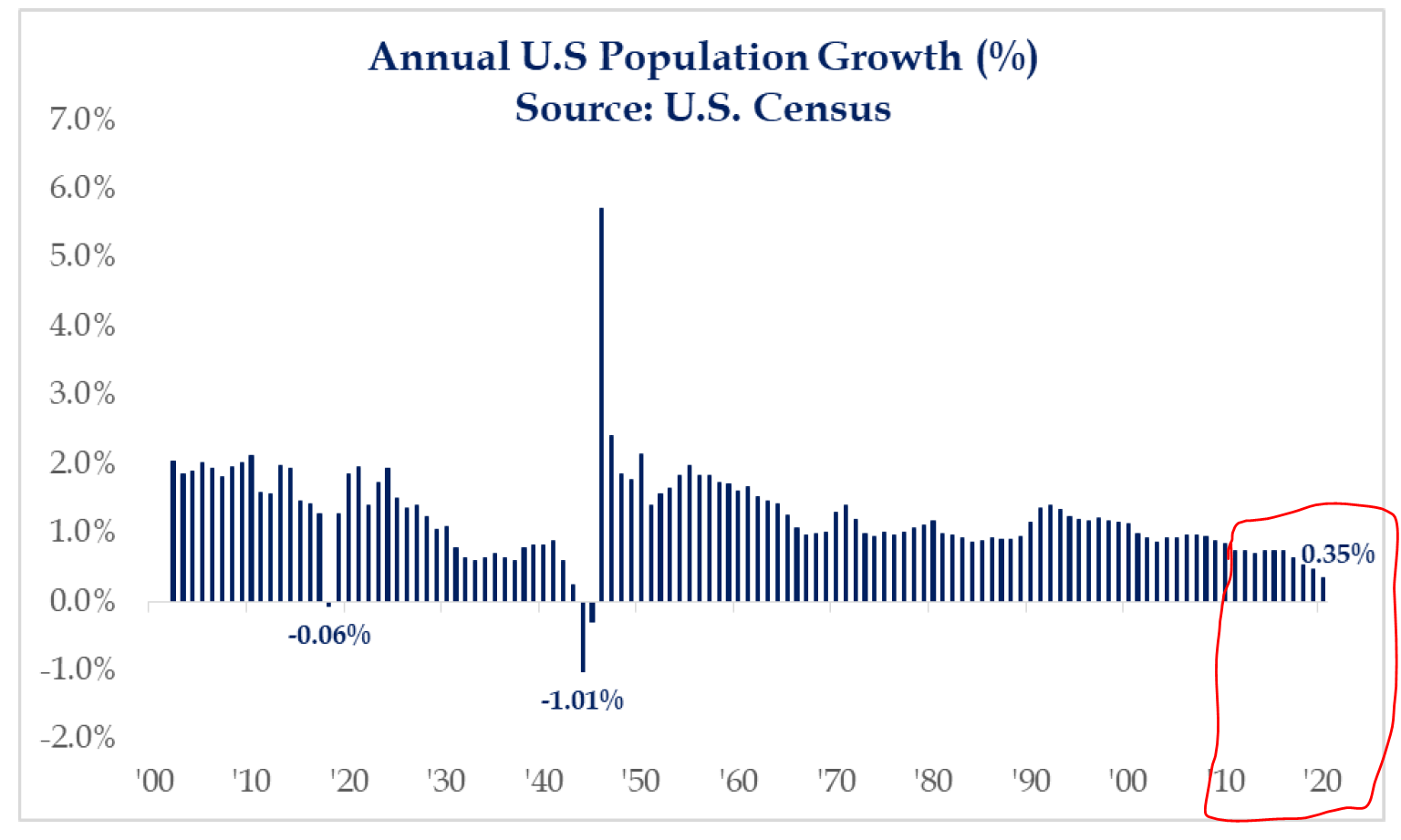

If you want something to be long-term concerned about, try this on for size

There are a grand total of two ways to see one’s population grow: Births and Immigration. If you come up with a third one, please let me know. I don’t want to chime in on the politics of the immigration debate – not because I have ever been afraid of controversy (I wrote an entire chapter on this subject in my book, Crisis of Responsibility), but because it isn’t pertinent to the subject at hand, and my views don’t fit squarely into either side’s “box.” But be that as it may, we aren’t exactly running up the score with immigration as a driver of population growth these days, and many are happy about that (for right or for wrong).x`

But because we continue to have this thing called “deaths” in our country, for “births” to mean “population growth,” the birth count has to be higher than the death count (let me know if I need to slow down on any of this stuff). So there are two ways that this demographic conversation can drive population movement – one is the death rate accelerating (generally when there is an aging population), and the other is the birth rate (obviously a higher birth rate driving more population growth and a lower birth rate doing the opposite).

I offer no social or cultural commentary about what I have circled here, though I assure you I could if you wouldn’t want me to. I merely want to graphically illustrate that since the time of the financial crisis, population growth has shrunk substantially, and it is not a rising death rate causing it. Fewer babies mean less population, and to the extent, we combine fewer babies and less immigration together, we get even more “less population growth.”

Why does this matter for long-term economic growth? One of the simplest and least controversial tautologies in all of economics: Economic growth = Population Growth + Productivity. If one of those two ingredients drops at a rate faster than the other, economic growth contracts. If the rate of one decreases below trend-line historical expectation, the rate of economic growth will be below trend-line historical expectation.

*Strategas Research, Investment Strategy Report, April 16, 2021, p. 1

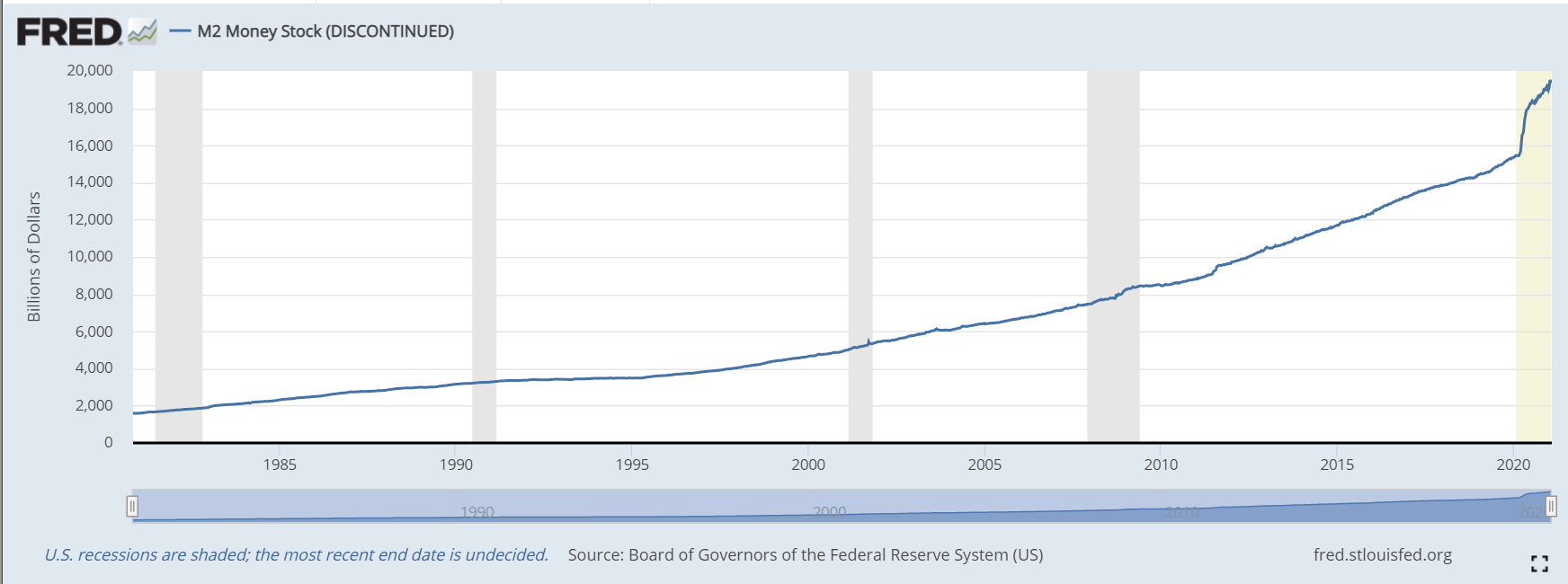

Just Can’t Leave This Topic Alone

One can see, visually and clearly, how “M2 money supply” has increased since the financial crisis. We then see another spike higher last year out of the COVID moment. My question has been why this would mean secular inflation post-COVID when it didn’t mean such a post-financial crisis, but that is a different topic than various indicators of cyclical inflation (which are inevitable). But yes, this chart would indicate potential inflationary concerns worth worrying about …

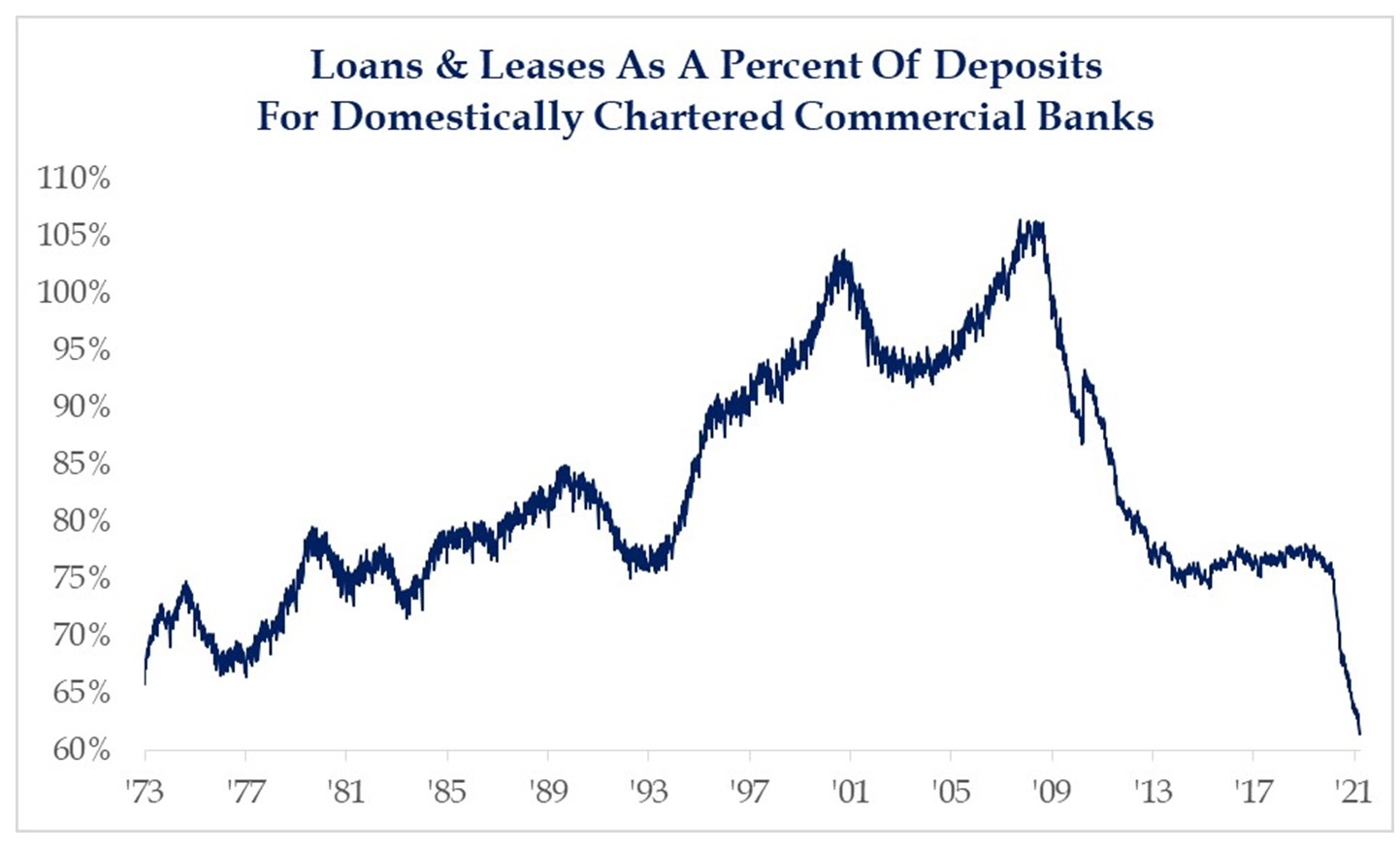

Until We See This Chart …

This chart essentially tells you two things: (1) Why the growth of M2 money supply has not proven to be inflationary, and (2) Why we DO have something to worry about …

What we have here is a tale of two countervailing forces. A growth of money supply and at the same time loan growth has collapsed. This is where velocity has collapsed. And this is why new money has not been created at the level sufficient for secular inflation. And yes, this is what the Fed simply cannot do anything about.

As had been discussed in a prior Dividend Cafe, new money gets created in our system when someone borrows money (that comes from a bank that has it from the Fed creation), and then adds it to their bank account (or someone else’s bank account) in the form of a deposit. A new deposit does not create a new loan; rather, a new loan creates a new deposit. The decline of loans as a percentage of deposits is anti-inflationary.

So why is this in my commentary on what I worry about? Because I want a healthy growth of loan demand. I certainly do not want inflation, but I do not want the dis-inflationary forces that are repressing economic growth in our society. We have a complicated relationship with inflation in our society (where we get perpetual inflation in the three areas that are subsidized – health care, higher education, and housing – and where reflationary cycles can mislead us into feeling that we have broken the deflationary pressures brought about by excessive debt, growing debt, distorted debt ratios, and ultimately, a diminished private sector).

*Strategas Research, Investment Outlook, April 6, 2021

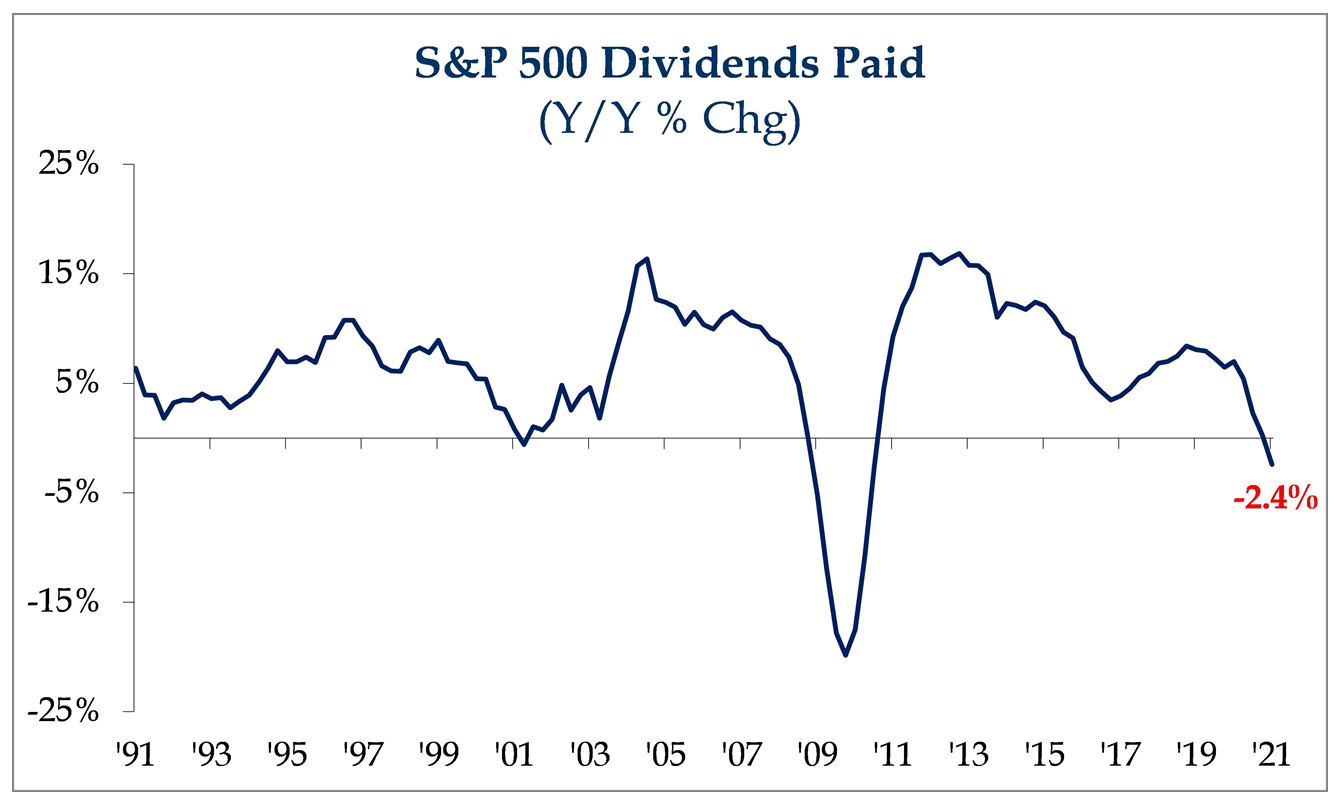

Are dividends declining?

I have to selfishly say, this chart does not make me worry – it benefits me. What I mean by that is this: To the extent index investors face declining income and declining yields out of increasingly expensive assets, it really serves to highlight the value of that area in the investable universe that is NOT seeing declining income or declining yields. In other words, the decline of dividends paid from the S&P makes approaches (such as ours at The Bahnsen Group) more attractive relatively speaking. I would love to get a high focus on dividends, dividend growth, and dividend sustainability, passively. My family would love it too (not for our own balance sheet, but because it would mean I could work less than the ungodly hours I work now). But dividend growth can’t be obtained passively, and this trend in the index enhances the value of what we do, not the opposite.

*Strategas Research, Daily Macro Brief, April 9, 2021

All that said …

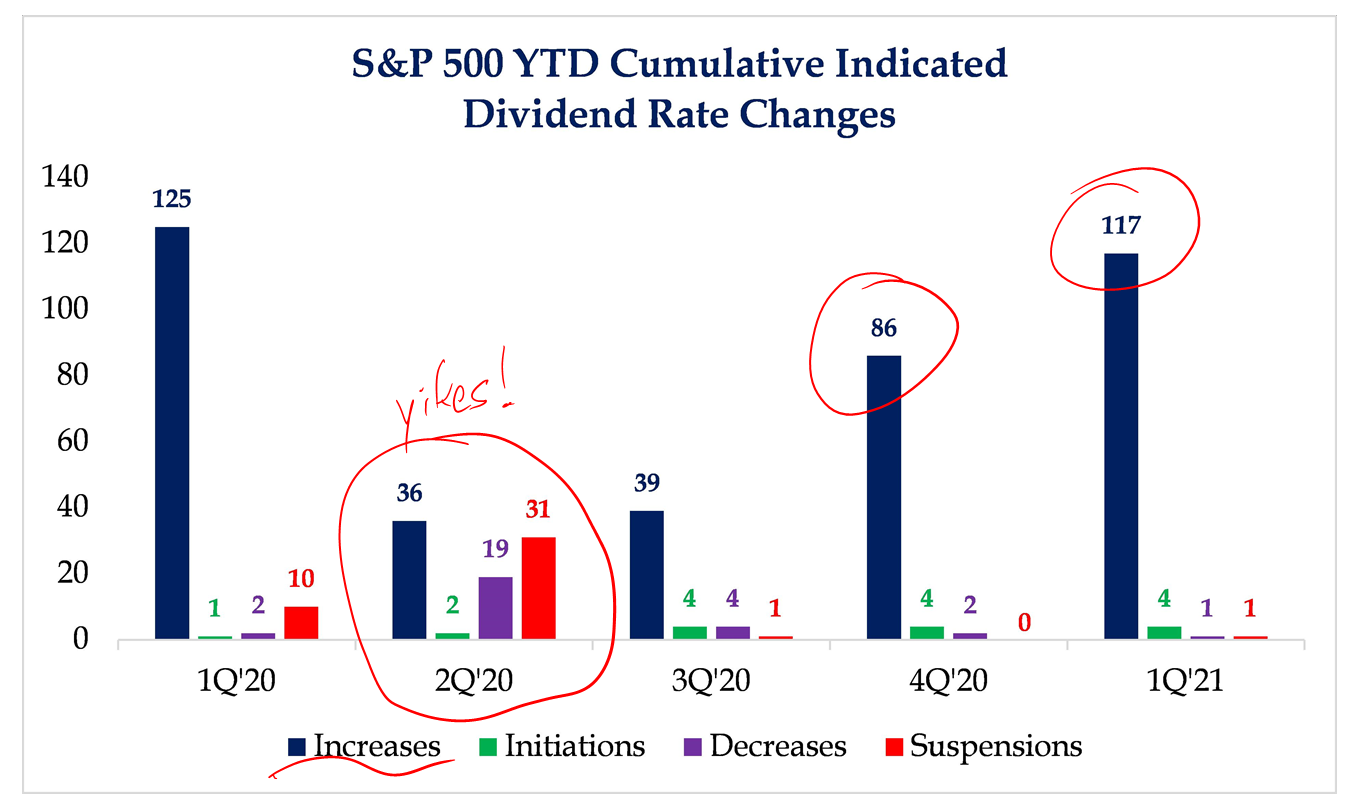

While what happens to the dividend levels of passive index investors during times of market distress bothers me immensely (see Q2 2020 below), like my point above on declining dividend generosity, it reinforces the value of actively management dividend growth. But I also would note – even if marginally – across the equity universe, a higher number of dividend increases is coming back as one would expect with recovering economic conditions and corporate profits.

*Strategas Research, Daily Macro Brief, April 9, 2021

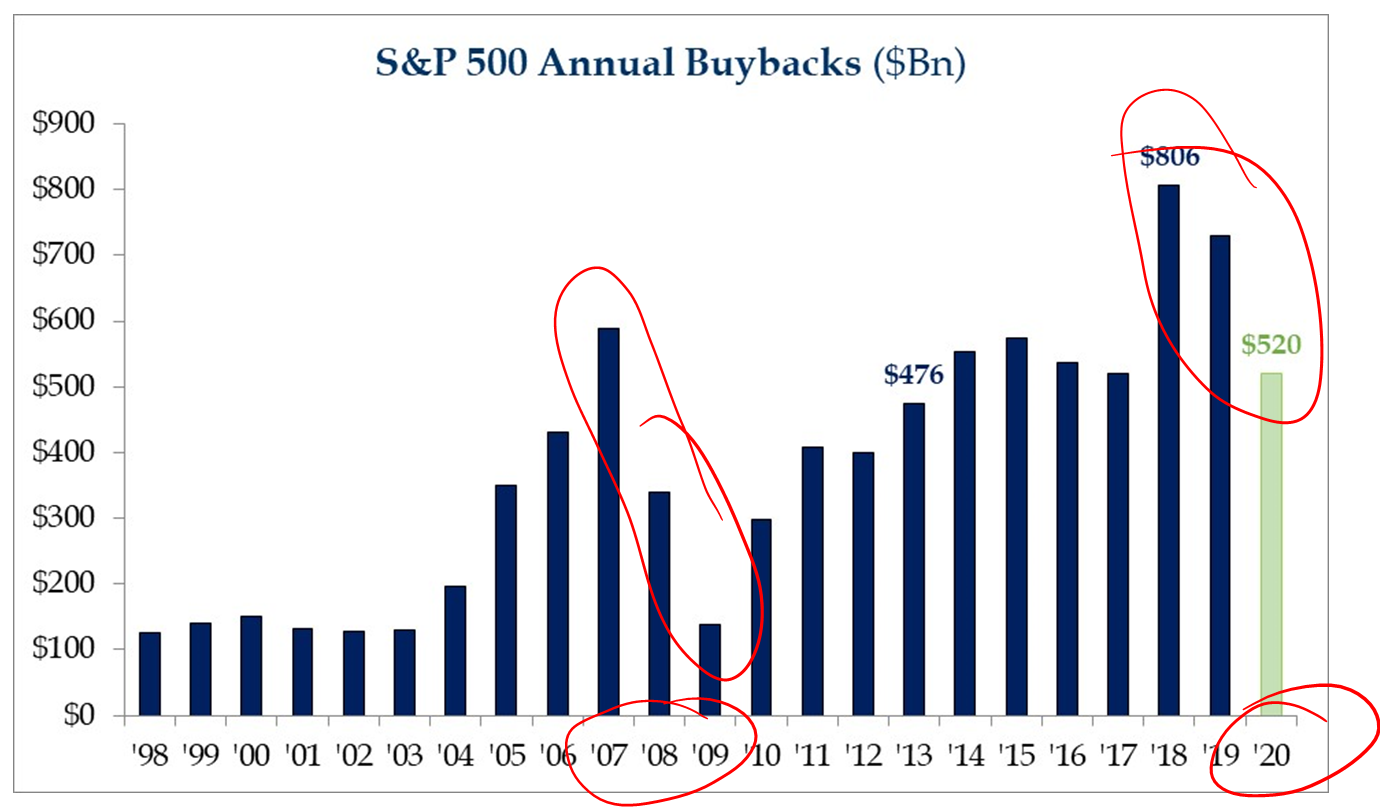

What got pummeled last year, and I mean pummeled, as a “strategy for capital return” was stock buybacks. Now, one may say, “sure, but now things are better and this means stock buybacks can resume, too!” Yes, this is true. Just in time for a 35x Nasdaq and a 25x S&P 500 all up ~20-30% from pre-distress levels. Rinse and repeat.

*Strategas Research, Daily Macro Brief, April 9, 2021

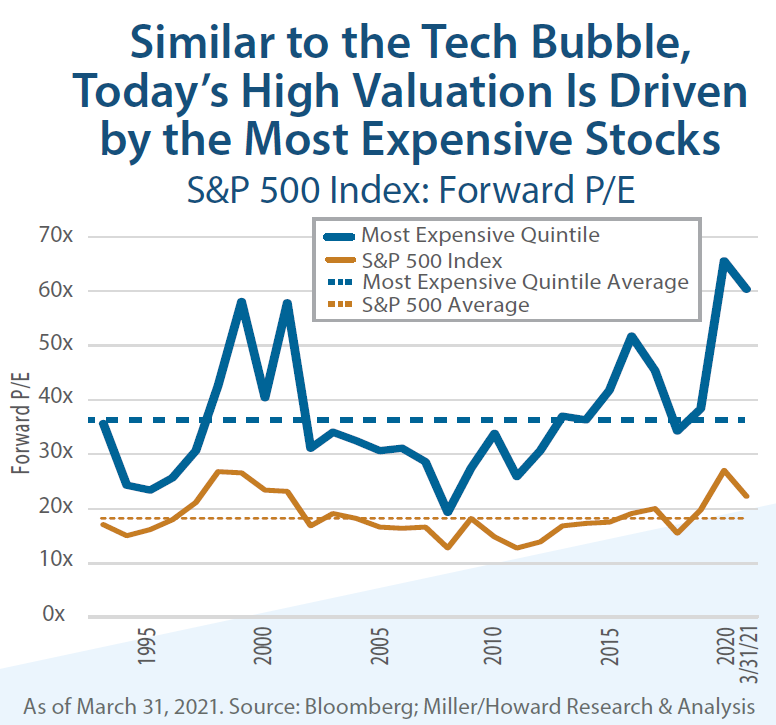

Chart of the Week

This could be included in things I do not particularly worry about, either, and that is – valuations levels that seem high in aggregate, because of one of the parts. In other words, I have to monitor valuation levels of what we own, not what we do not own. And when looks to what is elevating the valuations of the broad market, it is as much as any time since 1999 quite limited to one scope of the marketplace, a scope outside of our investing universe.

Quote of the Week

“Ironically, when a bunch of very smart people are sitting around a table for hours trying to figure out whether they should do something, that tends to not necessarily lead to the best results.”

~ Stephen A. Schwarzman

* * *

I have a book coming out at the end of the year (just in time for Christmas) called There’s No Free Lunch: 365 Economic Truths. I will be binge-writing most of the weekend ahead. And yes, I will do so with a fully functioning keyboard!

Enjoy your weekends, and reach out with any questions or comments, any time.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet