Dear Valued Clients and Friends,

Long-time readers of Dividend Cafe know that the real intent of this weekly commentary is to delve into the macroeconomic – the big picture – the high-level stuff that impacts investor decisions and behavior. Today in honor of the obsession over Jerome Powell’s speech at Jackson Hole (being delivered shortly after I hit “submit” on this commentary), I want to talk not an iota about the Fed, monetary policy, or really any aspect of macroeconomics. (In fact, I shared on Varney/Fox Business this morning why I was so sick of this cult obsession).

Rather, I want to actually dive into a question that is hyper-practical – more micro than macro – and that is when to sell a stock. I was in the process of answering a question about this topic for the Ask David section of The DC Today when I realized it really warranted the full Dividend Cafe treatment.

So here we are – a Fed-free Dividend Cafe dedicated to the ever-practical issue of sell discipline. We’ll discuss Jackson Hole in Monday’s DC Today (only because I have to), but for today let’s talk about how dividend growth equity investors like ourselves think about the right time to sell a stock. Let’s jump into the Dividend Cafe …

|

Subscribe on |

No Outsourcing Here

While the weekly Dividend Cafe may generally revolve around “macro” themes and realities in the economy, we actually are very bottom-up investors in our day-to-day activities. Throughout the week we obsess over portfolio particulars and implementation. Our firm manages money in-house and does not outsource decisions over asset allocation to a turnkey third-party platform as so many fee-charging advisors do today. Not only are we making all asset allocation decisions for our clients in-house, but we are doing so on a completely custom basis, client by client by client.

Asinine Asset Allocation

We operate off an investment methodology that we built and designed in-house called “Operation Magnify” with a grand total of seven potential asset classes on the table for every single investor. While many professional investors were trained in the business to believe asset classes are such things as “small-cap growth” and “international equity,” we chose to structure our organization of asset classes around their actual function for clients. Why would an investor own small-cap growth stocks? For long-term capital appreciation of value with a high acceptance of price volatility along the way. Why would an investor own international equities? For long-term capital appreciation of value with a high acceptance of price volatility along the way. They are two different types of stocks, but their risk, reward, and objective considerations are the same.

The “style box” approach is lazy, marketing-driven (by the asset managers and third-party consultants who need to justify their existence), and unhelpful to clients who don’t (or shouldn’t) care about the difference between mid-cap value and large-cap growth (as if an investor’s actual financial objectives are connected to the market capitalizations of the companies they own).

Our proprietary structure for asset allocation revolves around:

- Core Dividend Equity

- Boring Bonds (taxable or tax-free)

- Credit (taxable or tax-free)

- Growth Enhancements

- Income Enhancements

- Alternatives

- Directs/Illiquids

Each of these “asset classes” is quite distinct from one another in terms of how they matter to an actual investor. They are distinct from one another in some core function or criteria. Yes, Core Dividend Equity can include a $3 billion company and a $1 trillion company. Yes, a Growth Enhancement can include a Small Cap stock and an International stock. The distinctions in these seven categories revolve around the practical matters of embedded risk, liquidity, volatility, and investor goal.

Dividend Focus

You would be right to suspect that Core Dividend Equity (of the above asset categories that make up the building blocks of our portfolio construction) is our “core” ingredient. For some clients, it may be 70% of their total portfolio, and for others, it may be 30%, but it generally serves as the primary component in a portfolio because of our belief in the general investment merits. For more information on such, see: everything I have ever written and said for the last 20+ years; OR, if you don’t want to expose yourself to such tedious torture, you can always pursue the cliff notes via video or podcast).

While we handle all asset allocation decisions for all clients across all seven asset categories ourselves, we do utilize specialist managers in some asset classes that either bore us to tears (boring bonds) or require hyper-specialization (the emerging markets within Growth Enhancement, for example). But Core Dividend Equity is our baby – wherein we are not only the asset allocators but the portfolio managers as well. Therefore, my focus on “when to sell a stock” today is within the context of the over $2 billion we directly manage in the dividend equity genre.

Market Timing

So allow me to offer this nuance or distinction right up front … There is a difference in this discussion between “when to take equity exposure from 50% to 0%” (hint: never), or “when to take equity exposure from 58% to 52%,” versus, “when to sell ABC stock within your equity exposure.” The subject of today is the latter. The question I am answering has to do with particular sell discipline around a particular security, which is different than coming in and out of the market en masse. We do not believe jumping in and out of the market has worked well for people over the years other than abject liars who never seem to produce their statements or confirm when I ask for proof (all of them – the brilliant exit and the brilliant re-entry). The point we have made time and again is that the predominant determinant of investor success is behavior, and market timing subjects investors to too many opportunities for horrid behavior, most notably the vicious regret cycle that has decimated people for decades).

So “in and out of the market” sell decisions are best left to truth-challenged folks at the bar.

Weight shifts within asset classes based on valuations, risk-reward calculus, and other asset allocation decisions are also not the subject of this commentary. Modest knob-turning in allocations is generally reserved for rebalancing purposes, and when there are tactical target weight shifts, they are usually marginal and valuation-driven (which includes a heavy dose of contrarianism mixed in).

But what about an individual stock? What drives our process and decision there?

To Sell or Not to Sell, that is the Question

I start with the basic premise that, ideally, in a perfect world, I would love to hold all companies we buy forever. I also start with a premise that it is not a perfect world. But if it were not for such imperfections, to hold companies that are reasonably priced and growing their dividend reliably forever would be splendid.

Now, sometimes facts change. A company could have a long track record of dividend growth but begin to do things that bother us (poorly planned M&A, excessive debt, a new questionable business strategy, etc.). There are things that happen that change the investment thesis of a company, and all ideals regarding long-term holds notwithstanding, responding to substantive and verifiable change is prudential.

What if ??

The person who asked me this question for Ask David wondered if we would sell a stock once it was up +30%. We would never, ever, ever sell a stock because it was up 30%. We have stocks up +100% and +65% just this calendar year that we are not selling. Some gains may become large enough relative to the movement of other stocks in the portfolio that our desired weighting becomes too disconnected from the actual weighting, forcing a “rebalance” of sorts. But selling a dividend-growing company with a still-reasonable valuation in the context of opportunity cost and a thesis for dividend growth that is not penetrated would be outside of my comprehension.

I should add – a company being up +30% or down -30% is completely immaterial to where the company is now and where it is going in the future. It only speaks to where it was when it was bought. Stocks do not care what you paid for them; they are vicious forward-looking pricing mechanisms with no capacity for memory whatsoever. A stock can be down -40% and very expensive (I can think of a couple of mega tech ones right now), and it can be up 5,000% and quite cheap. The unrealized gain/loss a given investor has on a particular stock is as irrelevant to the business prospects of a company as any data point could possibly be.

An objective criteria

We believe in owning a company for the receipt of its future earnings potential, and the capacity of that company to share the fruits of those earnings with us, the shareholders, in the form of dividends. Because we want companies that will grow earnings year-over-year, we expect to get dividends that grow year-over-year. And this becomes both a cause of investor return (actual dividend receipt) and an effect of investor return (the fruits of a company creating measurable value through the free enterprise system).

We save ourselves and our clients a lot of grief by actually having a sell discipline that can be defined in some way other than arbitrary finger-in-the-wind feeling about momentum or P/E expansion. Our BUY discipline is rooted in prospects for sustainable dividend growth; therefore, our SELL discipline is rooted in fears of losing sustainable dividend growth.

A lost margin in cash flows. A vulnerable business strategy that is susceptible to great reversal. Leverage ratios that require perfection to maintain the dividend. A capital intensity that is not flexible in down times. A new acquisition that is not accretive and adds debt service expense in a way that jeopardizes the dividend. And one of the easiest to identify – governmental control of the dividend due to some regulatory or political event that all but assures a dividend cut or elimination.

Getting cut by a cut

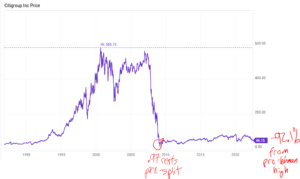

We can be wrong about a company’s likelihood of cutting the dividend (that is, the “false alarm” factor), but we rarely are. The opposite has played out many more times (selling because we feared a dividend cut could come and then having it play out later as suspected). From Citigroup in 2007 to BP in 2010 to General Electric in 2017 to AT&T in 2018 to Boeing in 2020, the majority of times we have sold a stock projecting a dividend cut ended up being proven right in due course.

Now, it is always possible we sell a stock out of fear of a dividend cut coming, and that dividend cut does not come (Omega Healthcare comes to mind). It is also possible, but extremely rare, that a company cuts its dividend, and in due time the stock price is rewarded, not punished. But more often than not, this happens:

*YCharts, Citigroup 1985-2022

Call me nostalgic, but I will always consider our pre-crisis sale of Citi a career-making moment.

The company’s messaging

We care about the company’s confidence in their own prospects via their declaration that is a dividend (where it is set, and how it is adjusted year-over-year). Companies that manage to a dividend growth with the free cash flow to cover it speak louder than a stock chart does, a quarterly announcement does, a press release does, or a talking head on TV does. Dividends are signals, and when responsibly paid and sustained, we have better inside information than anything else we could obtain to make a decision.

Opportunity Knocks

Sometimes we will trim a stock’s weighting to free up cash for another opportunity. Consider a stock bought at $50 with a $2 dividend (4% at purchase) that over ten years goes to $150 and now pays a $4 dividend. The dividend income is up 100%, yet the yield has gone from 4% to 2.67% (tough problem to have, right?). We may modestly “trim” the target weighting of that company from 3% to 2%, essentially “capturing gains” incidentally, but more practically, freeing up cash to purchase what may have more current income and future income growth potential. Now, the company being trimmed may still have great dividend growth in front of it, and in fact, companies that do that generally are “aristocrats” – that is, highly dependent dividend growers over many years and even decades. There remains a compelling thesis for ownership, so the company is not to be sold. And yet, “trimming” from gains allows a compounding of capital in pursuit of new opportunity.

Trimming, not selling, in pursuit of better opportunity.

Conclusion

We own companies right now we have owned for many, many years that we hope to own for many, many more years to come (and are confident we will). We can’t say “forever” because the history of corporate finance is filled with famous implosions, disruptions, bad CEO hirings, failed M&A, and other forces of creative destruction in this crazy thing often called capitalism (I prefer free enterprise). There are companies we own now that have a dividend today equal to over 100% of the stock price in 1985, 1981, 1978, 1965, etc. The compounding of capital that dividend growth properly executed makes people is a wonder to behold, and we have no desire to forfeit exposure to that modern miracle.

The right time to sell is never, unless facts or thesis change. And the right time to “trim” is when opportunity knocks.

To these ends, we work.

Chart of the Week

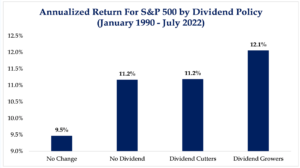

The great fallacy I have long rebutted in my work on this subject is the idea that, while dividend growth may be a less volatile or vulnerable way to invest, it requires one to forfeit return potential over time. The objective facts tell us differently.

*Strategas Research, Daily Macro Brief, Aug. 26, 2022

Quote of the Week

“The American dream of human progress through freedom and equality of opportunity in competitive enterprise is still the most revolutionary idea in the world today. It’s also the most successful.”

~ President Ronald Reagan

* * *

Maybe today’s Dividend Cafe will prompt more questions. Maybe this is information you already knew about our methodology. And maybe it scratched an itch or two. Next week you are in for a real treat as we analyze the fate of markets over the years relative to USC’s destiny on the gridiron. It only seems right. One week to go until the fall is upon us.

Fight on, and thank you for trusting us with your sell decisions if you are a client of our firm. We do not take it lightly.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet