Dear Valued Clients and Friends,

Where to begin, indeed. It may have been exactly the kind of week investors wanted to start off 2021, but it certainly wasn’t the kind of week anyone wanted to start off 2021 from the vantage point of our country, her peace, her well-being, and her example to the world. The concept of a city on a hill is not working well, and this patriot feels total exasperation and desperation.

But I do know the readers of Dividend Cafe do not come to this publication for perspective on national conscience or psyche, especially not my clients. I believe there is a lot in this week’s Dividend Cafe that you will want to read, that matters to investors, that can better inform your beliefs and understandings in financial markets. So I am going to do what I normally do, and welcome any questions and comments any of you may have – as always.

If the Dividend Cafe today seems a little different than normal, understand that this has been a very content-rich week at The Bahnsen Group. There is nothing I want you all reading more than our annual white paper reviewing 2020 and providing 2021 outlook. We also put out a two-part podcast on 2020 and on 2021, with videos on both as well (2020 here, and 2021 here).

But if you aren’t overloaded on Bahnsen content, let’s take a whirl around the world, and see if we can’t get smarter. The world needs smarter people, after all.

Markets and Capitol Hill Turmoil

I suppose you can understand why the markets didn’t respond negatively to the events that transpired in the capitol on Wednesday. After all, Vice President Pence did do exactly what most of us knew he was going to do (or put differently, didn’t do what he had been asked to do, that many of us knew he would never, ever do). And despite the objections of a few 2024 contenders, the electoral college was certified as has been the tradition in our country forever. This can’t minimize the gravity of what happened, and what could have happened, on Wednesday. But from a markets standpoint, that embarrassing and contemptible barbarism and lawlessness lasted a few hours, and the idea of a peaceful transition of power not happening was put to bed hours later.

As I said yesterday, markets are discounting mechanisms for corporate profits, and markets [rightly] do not perceive any adjustment to expectations for profits from what took place this week. You and I may believe that we are living in tumultuous times (we are), and that a serious moment of division and cultural incompatibility is becoming more and more apparent (because it is). Some may believe it will get better (I do). Some may believe it will get worse (it likely will, before it gets better). But for our purposes in the Dividend Cafe and your purposes in thinking about what capital asset pricing is, please understand – Markets are the most non-partisan and culturally-agnostic institution you will ever encounter.

But the world is laughing at us?

Sure. Some countries like Turkey and Zimbabwe chose to exploit our national tragedy to dunk on us with trolling tweets and such. And many countries rightly pointed out the history of American political stability and its role as a global example, not a laughingstock. But those countries are not about to stop doing business with us, and we are not about to stop doing business with ourselves, and so forth and so on. The same headwinds we had last week we will have next week (getting a full-blown opened economy, dealing with significant deficits and debt, etc.) – and the same tailwinds still exist as well (an economy on an inevitable rebound, pent up demand, broadening market participation, etc.).

Speaking of that economy and re-opening …

The jobs number today was about what I expected – as December payrolls were down by 140,000 versus November. This basically was netted out by an upward revision of 135,000 from the prior two months. ALL of the losses – literally, ALL – were in leisure and hospitality (down 498,000 jobs). Hourly earnings were up on the month, only because more lower-paid employees were unemployed. This is a broken record, but it needs to be said until it is no longer true … The weakness in the labor market is thus far concentrated in just a very specific part of the economy, and really cannot improve until economic restrictions are lifted and mobility is restored. It’s coming.

Is it a united government now?

It is hard to believe how quickly the Georgia Senate results left the news based on the events of Wednesday, but there is a market reality that, technically speaking, the Senate ended up in a 50-50 tie (which based on a Democrat in the White House results in a Democrat majority in the sense that the VP is the tiebreaker vote).

If markets were concerned about a Democrat majority in the Senate before the election, why was this not a market mover? For the simple reason that a 53-47 or event 52-48 majority would have provided a wider margin on some potential votes, and required less dilution and horse-trading, for certain policy ramifications that would not be market favorable, where a 50-50 tie with three moderate Democrat Senators in West Virginia, Arizona, and Montana, there is much less market concern about “tail risk” (really damaging policy decisions like eliminating deductibility of interest expense, large penalization of private equity and private credit markets, taxing unrealized capital gains, higher rates for s-corp proprietors, etc.).

One of these days all investors may fully grasp the difference between what gets said on a campaign stage and what really happens in legislation. In the meantime, we at least now (as market investors) get to deal with the far more boring reality of the latter, versus the seemingly more concerning noise of the former.

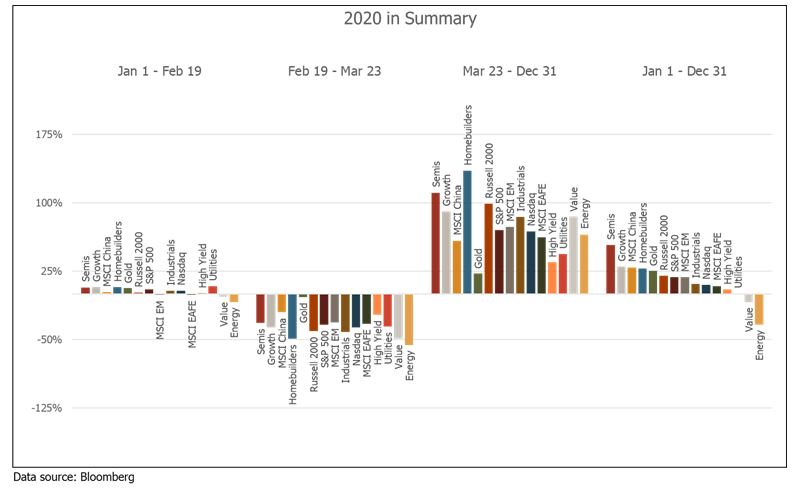

2020 in Three Stages

When we look at 2020, I really like looking at the year in these phases – the pre-COVID normalcy, the COVID panic and national margin call, and then the post-peak rest of the year. Note how each of those periods impacted various asset classes and equity sectors, as well as what it all looked like for the whole calendar year.

Stronger, Weaker

Will 2020 be the year of Weaker Economy, Stronger Markets, with 2021 being a year of Stronger Economy, Weaker Markets ?

I would say that is a pretty likely scenario – that those same index returns in the S&P 500 and Nasdaq are highly, highly unlikely to be repeated (multiples would have to go to a place we can’t even comprehend) – and that the economic picture of 2021 will be far better than it was in a year in which much of the year saw the entire economy virtually shut down.

The problem with this statement on relative results doesn’t tell us much about absolute results. In other words, saying the Nasdaq is not likely to be up 40% again does not mean it will be down 40%. Up 10% is a good return, and yet it is a lot weaker than +40%. Do I think the Nasdaq will be down 40%, or up 10%? I haven’t the foggiest idea. I merely think it will be less than 2020’s return, and I think the same about the S&P 500.

Investment policy gets made in goals/absolute needs – not relative comparative navel-gazing.

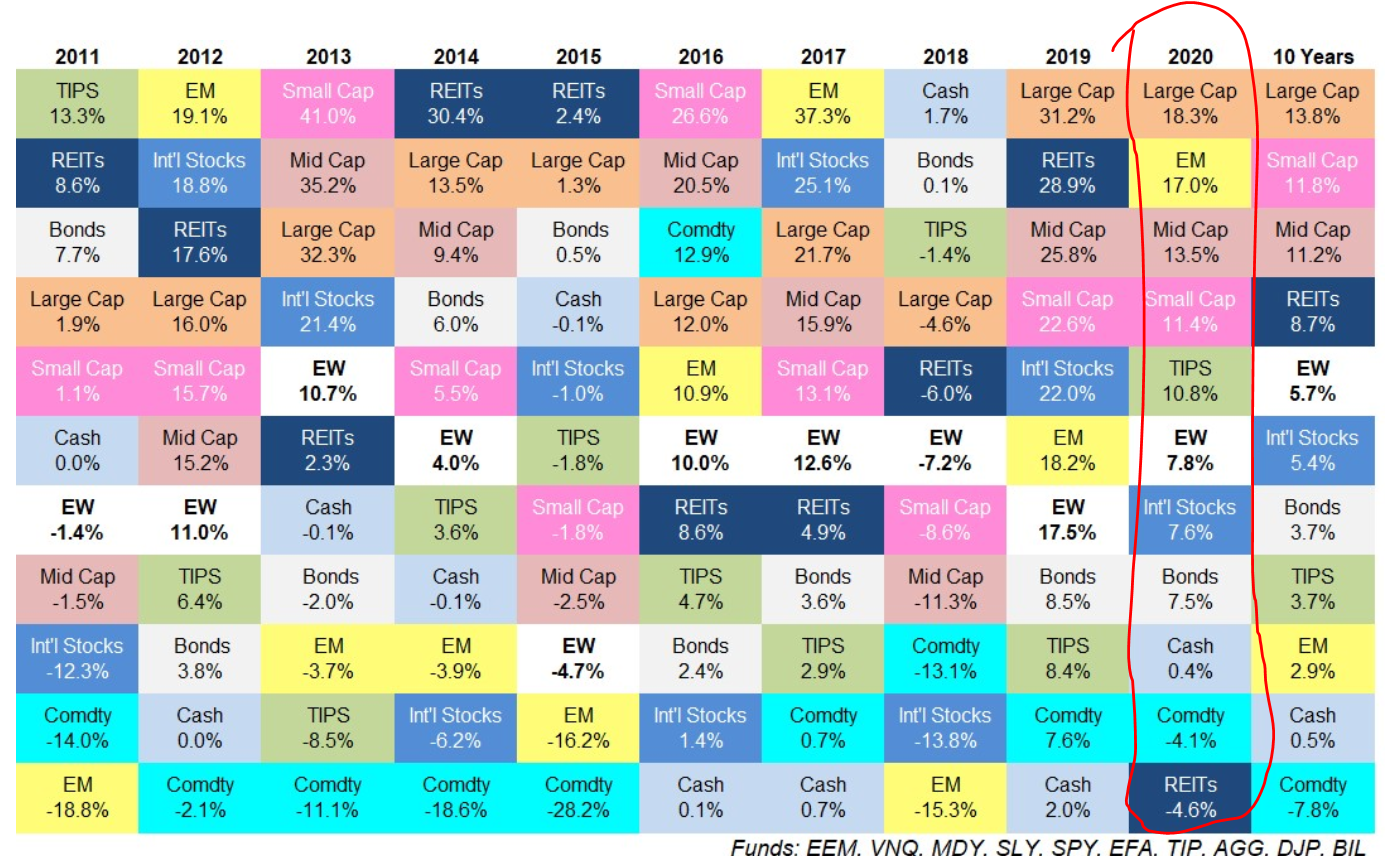

Why do we asset allocate?

No further comment

*Wealth of Common Sense, Ben Carlson, Jan. 5, 2021

Are any of these your favorites?

Note how far down some of the best performing asset classes of 2020 went down in a 4 week period back in Feb/March last year (h/t Ben Carlson) … Intra-year volatility is the source of risk premium that investors use to pay for their future financial goals. Never, ever forget that.

- S&P 500 (SPY) -33.9%

- Small caps (IWM) -41.1%

- Foreign stocks (EFA) -33.9%

- Emerging market stocks (IEMG) -34.7%

- Junk bonds (JNK) -22.9%

- Long government bonds (TLT) -15.7%

- Aggregate bond market (AGG) -9.6%

- Corporate bonds (LQD) -21.8%

- Gold (GLD) -14.0%

- Bitcoin -52.4%

The final return for those same asset classes?

- S&P 500 (SPY) +18.3%

- Small caps (IWM) +20.0%

- Foreign stocks (EFA) +7.6%%

- Emerging market stocks (IEMG) +17.9%

- Junk bonds (JNK) +5.0%

- Long government bonds (TLT) +18.2%

- Aggregate bond market (AGG) +7.5%%

- Corporate bonds (LQD) +11.0%

- Gold (GLD) +24.8%

- Bitcoin +304%

2008 still wins

I was quite convinced back in the spring that 2020 would end up being the most volatile year in history (not the worst market year in history, but the most volatile – meaning, the most extreme up and down movements). Things settled so much in the second half of the year when the market got its arms wrapped around COVID that things changed. But 43% of market days were up or down 1% or more last year (that is a LOT), which was not the 53% of days that 2008 was. #Memories.

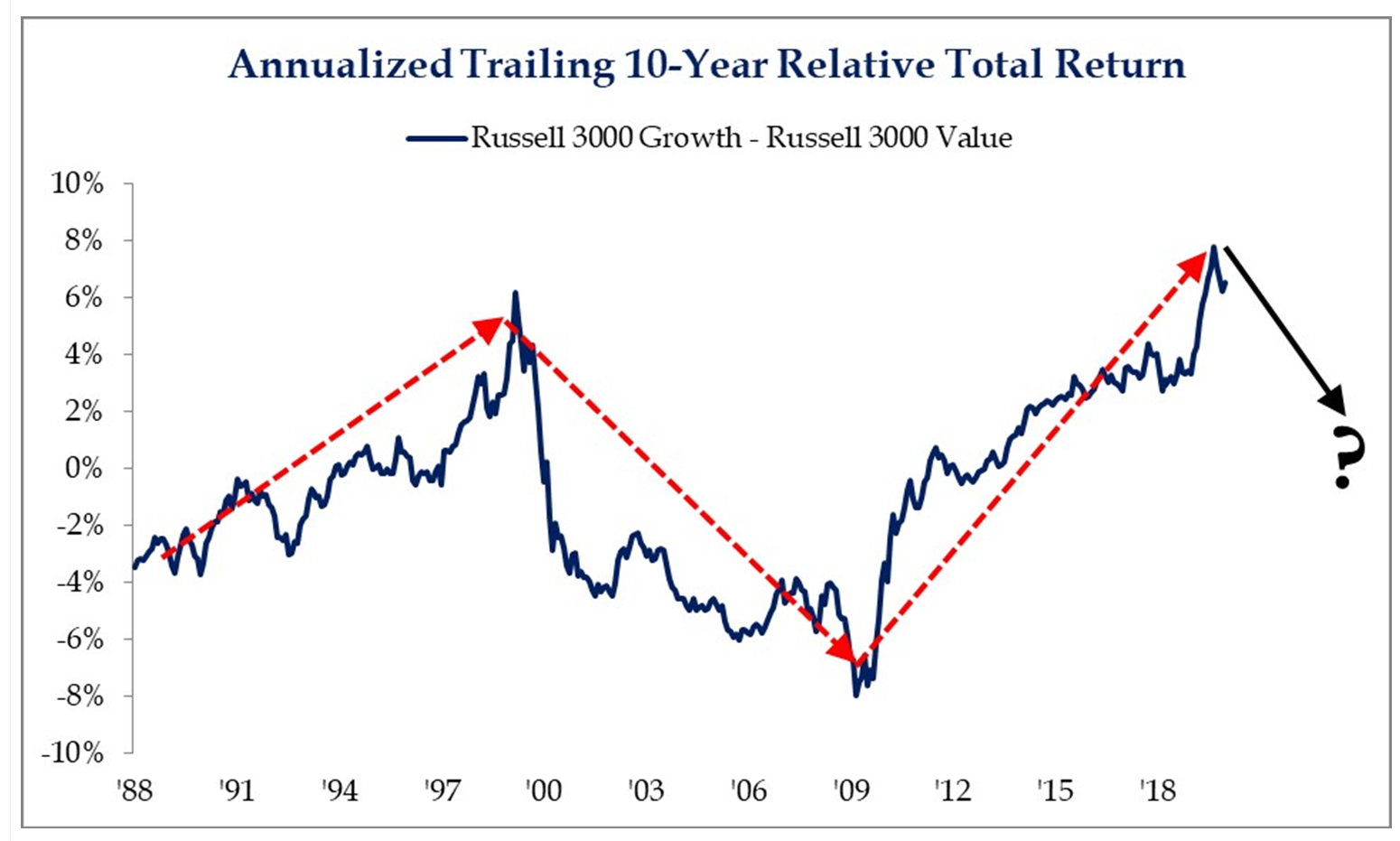

Growth into Value Rotation is our Belief. And history’s.

Again, this doesn’t show absolute returns – it shows relative returns – the kind you cannot pay bills with or feed your family with. But relatively speaking, a big decade of growth outperforming value was followed with a big decade of value outperforming growth, and then a decade of growth outperforming value. And so here we are. And …

*Strategas Research, Daily Macro Brief, Jan. 8, 2021

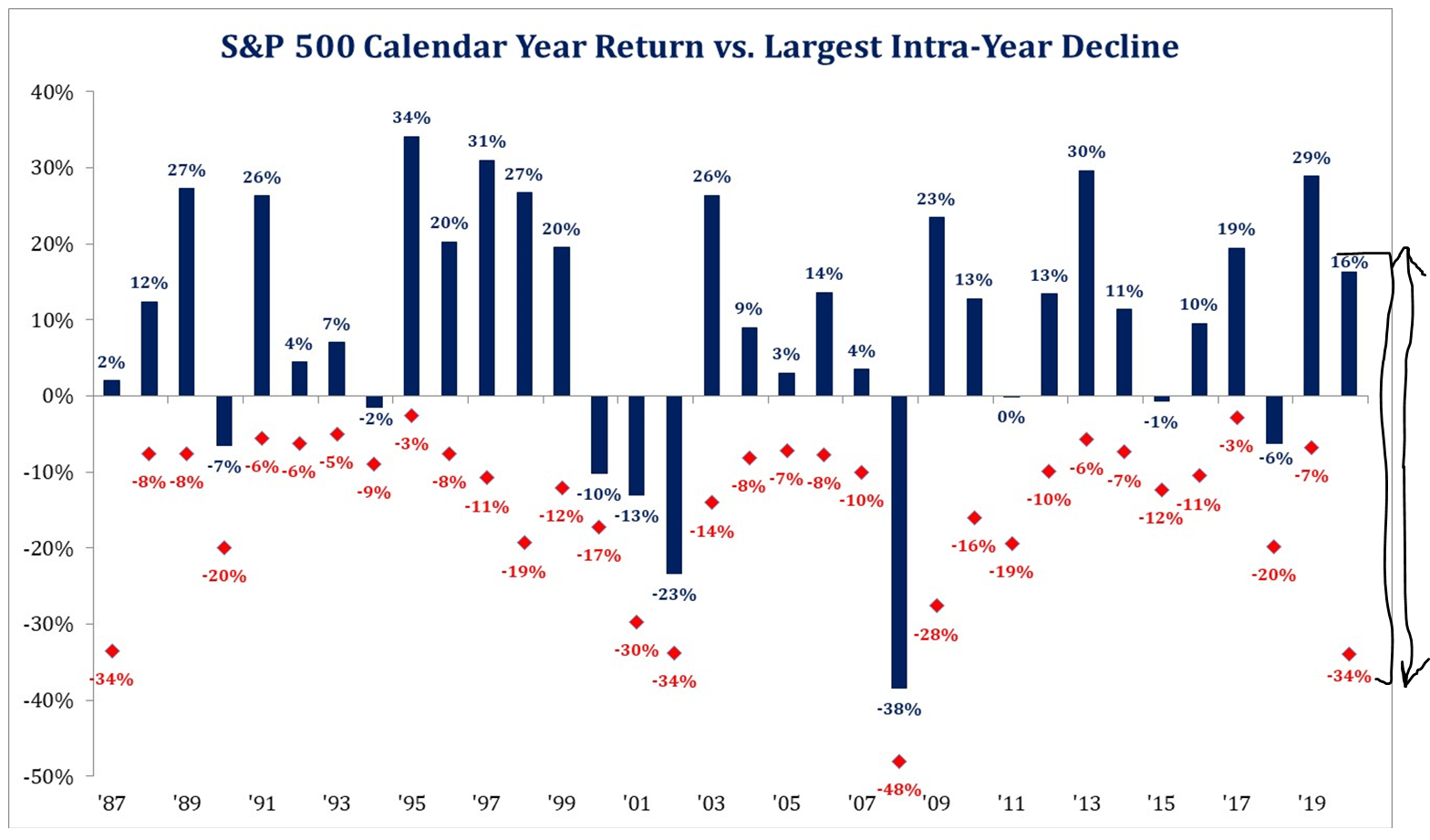

Chart of the Week

The volatility that drives the risk premium that drives long-term returns.

Up and down movements of a VIOLENT nature are awful. Up and down movements of a less violent nature are PAR FOR THE COURSE. And all of it can be remedied through asset allocation – through custom, targeted, truly personalized understanding of an investor’s needs, appetites, tolerances, goals, overall situation, etc. It is time to Magnify these things.

*Strategas Research, Daily Macro Brief, Jan. 4, 2021

Quote of the Week

“The line separating good and evil passes not through states, nor between classes, nor between political parties either—but right through every human heart—and through all human hearts.”

~ Alexsandr Solzhenitsyn

* * *

If you have not studied the great Solzhenitsyn, you owe it to yourself to.

Freedom is a treasure. And the line between civilization and chaos is far thinner than anyone wants to talk about at parties.

Hope springs eternal. God bless America. And God bless the free markets that drive opportunity in our country. A miracle for hundreds of years and counting. I, for one, want to keep the miracle going.

You can trust us to tell you the truth this year, and every year. To that end we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet