Dear Valued Clients and Friends,

There is something incredibly flawed in the title of today’s Dividend Cafe. I pose a question that carries a presupposition which is, itself, flawed. In asking if people will ever care about value again, it assumes that they do not care about value now, or have not cared about value before. This is a generous interpretation, as it assumes that investors have consciously dismissed the relevance of valuation, which is perhaps better than if they have not dismissed it, and instead actually find certain valuations attractive. But even if the title begs a few questions, the substance of today’s Dividend Cafe will not. Today, we are going deep into the heart of all investing, and I mean it when I say, all investing – and that is valuation.

The aim today is to do a little history, a little Investing 101, and a little thought exercise around how these things all work. And in the end, I think there might just be some actionable takeaways from this particular trip inside the Dividend Cafe.

|

Subscribe on |

Buying When it Hurts

Proverbs 20:14 (for those familiar with the Bible) talks about an economic transaction:

“It’s no good, it’s no good!” says the buyer—

then goes off and boasts about the purchase.”

For thousands of years, there has been an embedded understanding that a good part of a transaction’s sense comes at the time of purchase. It may not be fully true that “all money is made at the buy” (that is, buying something so cheap that you can’t lose money), but it is certainly intuitive to most of us that “what we pay for something matters.” It is sort of surreal that this has to be said anymore, but it does. Buying at an attractive price is, well, a good thing.

It pains a value guy like me to be writing this. I feel like I just wrote a whole paragraph for thousands of intelligent people saying, “food is more enjoyable when it tastes good,” or “cars drive faster when they are not out of gas,” or “football is a better sport when the team playing is not wearing a powder blue color.” It all seems so obvious. Yet if it were, would I be writing this Dividend Cafe?

Buying When it Feels Good

The opportunistic merchant of Proverbs knew that there was distress or some stigma to what he was buying, yet believed the price paid represented a value he could brag about in terms of the future opportunity. There had to be some truth to the “it’s no good” claims, or it would have rung hollow, and presumably the seller would not have wanted to transact. The present-tense discomfort led to a future-tense opportunity. It need not be a dramatic disconnect – not every “value” means “deep value” or “severe distress.” But, the point is that there has traditionally been some sense of an investment feeling unpopular at purchase.

This is the polar opposite of how many investors feel today. They want to publicly brag at the time of purchase to feel good about an investment.

“I just bought something that is already up 1,000% the last few years” is not exactly Proverbs 20:14 vibes, but it certainly is the vibe of much modern investing. Whereas the mantra of the most successful investors of the last century (Graham, Buffett, Ackman, Icahn, Marks, Tepper, etc.) has been that the more uncomfortable something was at purchase, the higher the expected rate of return, today’s mantra is that buying something everyone else already likes must be the ticket. Unpopular = bad. Already popular = good.

And it has hardly hurt people, yet. Sure, in 2022, many “momentum growth” investors got a taste of the pain that can befall valuation-agnostic investors. And truth be told, as unbelievable as Nasdaq returns have been, if one entered at the high of 2021, they are currently up an underwhelming 5.7% annualized since then, despite the massive gains of 2023 and 2024. Math is pesky. However, drawdowns on “momentum growth” investments have not lasted long as of late, and there can be a feeling that “buying high, selling higher” is the new normal.

And I am here to tell you that it is not. If we define high correctly.

Caveats, Outcomes, and Examples

A stock can already be up 1,000% and be a generationally attractive investment. There is no rule that a given % return has capped the opportunity set of a company. What drives future returns is, wait for it, future operating performance combined with present valuation and future valuation. Here are a few ways these things can go:

- A company does very well and has great returns because of it. Optimism for the future increases, the valuation goes way up, and then, going forward, the company exceeds that optimistic expectation. This is a good outcome for an investor who buys even after the initial great returns.

- A company does very well and has great returns because of it. Optimism for the future increases, the valuation goes way up, and then going forward, the company meets but doesn’t exceed that optimistic expectation. This is a sub-optimal outcome for an investor because while the operating performance was good, the investor returns are muted or subpar, because the person who sold after the optimistic valuation captured all the premium then that the buyer wanted in the future.

- A company does very well and has great returns because of it. Optimism for the future increases, the valuation goes way up, and then going forward, the company underperforms that optimistic expectation. This is a catastrophic outcome for the investor who buys after the initial great returns.

To just put a basic framework or example around these, think Apple or Google with #1, think Cisco from 1999 with #2, and think Peloton from 2020 with #3. But I could list hundreds of companies in each category off the tip of my tongue if called upon to do so.

Valuation not Price or Results

Note that the operative variable at play is the valuation. The operating performance was very good in the second outcome, but investor results were poor because of valuation. The price was already high in the first outcome, but investor results were still good because operating performance exceeded valuation. The investor results were doubly bad in #3 with the double whammy of disappointing operating performance and excessive valuation.

Price matters only to the extent that it reflects valuation that is either good or bad. It (price) is not predictive or causative. And even operating performance matters to the extent that it is above or below a valuation. This was the essence of Ben Graham’s fundamental investing gospel: that by discounting expected cash flows to a present valuation, a stock price was either less than or greater than its intrinsic value. The impressiveness of the future cash flows was less relevant than what that discount or premium to intrinsic value may be. Show me a company that grows at 25% when it is expected to grow at 40%, and I will show you a bad investment; show me a company that grows at 7% when it was expected to grow at 2%, and I will show you a good investment.

Economics 101 and Investing

Now, here’s the thing I want all readers of the Dividend Cafe to understand: This is not some profound revelation of investing magic that I am sharing. It’s basic human nature, and it’s not remotely limited to our investing decisions about what we buy and sell. All economic transactions fundamentally reflect a decision about valuation. Every day that I do not buy a steak for $1,000, I am being a value consumer, because guess what – I can afford an outlandishly-priced steak, and if I buy it, I am absolutely going to like it. But there is a price at which it does not make sense (and $1,000 is where I draw the line for a ribeye). But in a more serious and widespread sense, our entire economy revolves around second-by-second value assessments. There are very talented people whom we cannot hire because their price is too high relative to the value we would receive from their services. There are technology solutions we pay for (at a high price) because of the value we get, and others we don’t pay for (impressive as they are) because we do an economic calculation that leads us to pass. Every business does this every day. Every consumer does this every day. And yes, every investor does this every day.

Decisions about valuation drive economic activity.

What Undermines Valuation?

It is certainly true that the example of #3 above can lead to valuation hurting an investment (that is, poor operating performance relative to valuation paid at purchase). And it is true that “average” results with a premium valuation can lead to disappointing results. But the fundamental drivers of higher valuations, including ones that become, at best, risky and at worst disastrous, are usually detectable, behavioral, human things. That is, excessive valuations come from too much capital chasing the same investment. The governor of such a thing is supposed to be valuation discipline. But alas, the temptation to invest based on what just got done being a good investment (rearview mirror) is hard to resist. The desire to brag about buying something already popular seems socially risk-free (it remains for me, 25 years into this career, incomprehensible that grown adults care about such a thing).

But there are only so many shares of XYZ hot stock, and XYZ hot stock might very well have an incredible business model (for the sake of argument in this Dividend Cafe just assume it does – that we are not talking about Peloton in 2020 – that we are not talking about a shiny object – that the XYZ stock is one heck of a growing company, just with a valuation already saying so). When demand exceeds supply, prices increase unless demand is tempered by valuation. It often is not because of FOMO – human nature – fear of missing out. And this drives returns higher, and this drives FOMO higher, and this drives demand higher, but none of this is driving supply higher. Rinse and repeat. And next thing you know, XYZ is 80x forward earnings.

Until it is not.

The Contrarian Assumption

Richard Bernstein convinced me some time ago that value investing is rooted in optimism, whereas growth investing is rooted in pessimism. The only reason to pay stratospheric valuations for successful, growing companies is a truncated view of the world – of a market economy, or dynamic innovation, of Darwinian capitalism – that assumes only a select few companies will be able to successfully grow. Value investing presupposes that we can be selective because there will be a plethora of success stories; so we may as well mine for the best deals. Value investing believes that companies can overcome difficult periods and challenging headwinds, and that the current price may not reflect such optimistic achievement.

Growth investing is not about an “exciting future” anymore. It is increasingly (implicitly) about the assumption that innovation and operating proficiency and talented management are obsolete, and that the future belongs to just a few [monopolistic] companies who have already done extremely well.

Value investing assumes lots of companies will grow, but better returns are available to a long-term investor when one’s purchase price is more reasonable.

Not all “growth” investors believe this. They made up a stupid term to describe the dinosaurs who believe that valuation matters even for growth-minded investors: GARP (growth at a reasonable price). Apparently, these GARP weirdos are in contrast to the “who cares what it costs – I’ll have two ribeyes” crowd.

Did I mention my feeling of it all being surreal?

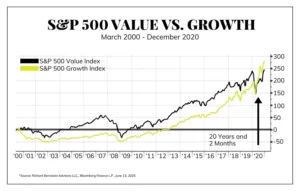

Has Growth Really Beaten Value?

The outperformance of “growth” versus “value” has been so pronounced in the era of Mag-7 and FAANG that many do not know the harsh truth of the matter: Value had outperformed Growth for over twenty years going into the recent post-pandemic period. Growth finally passed value from the beginning of this new millennium after COVID, but it took over twenty years to do so.

How could that be? With the way things went for “growth” throughout the FAANG era post-crisis, why did it take over twenty years? Simply put, the valuations were that stretched in growth at the beginning of this new millennium, and the relative performance of value over growth was that severe in the immediate years that followed.

Bubbles That Don’t Burst Get Bigger

The Nasdaq crash of 2000, which led to a 15-year period before it recovered that price level, was not catalyzed by a war, by a company failure, or by a macroeconomic event. It most certainly was not catalyzed by a change in outlook on the internet. It was not catalyzed by a decision to stay in a dial-up modem world, or that e-commerce was a bust, or that the web was less robust in its utility than we had thought. The efficacy of the internet as a vehicle for information, distribution, commerce, and communication did not disappoint – it delivered, and then some. So why did the Nasdaq break in 2000 – not just the absurd little dotcom companies run by 25-year-old party kids with less revenues than I made mowing lawns as a middle schooler, but even the biggest and best that actually powered the internet and technology ecosystem of our country? It broke because it was in a bubble. And bubbles always burst. Always.

The problem with what I just said is that it is a statement requiring hindsight. The level at which a bubble bursts is unknowable. I do not agree with former Fed chair Alan Greenspan that “bubbles are only identifiable after they have burst.” I believe it was obvious, and I mean screamingly obvious that U.S. housing was in a bubble in 2005, and that dotcoms running Super Bowl commercials in 1999 were as well. But that is different than saying that it was obvious when the bubble would stop blowing.

The testing of the mettle of a value investor is when bubbles – that is, things clearly in a bubble – keep bubbling more and more and more. The temptation for investors to join the FOMO crowd in those moments is overwhelming. But many are called, and few are chosen, and one’s ability to resist that seduction is perhaps the most important investment test one will ever go through.

I am doing a Dividend Cafe on bubbles in two weeks, but this week we are not talking about a “bubble” per se – we are talking about excessive valuations of a category of investment versus appropriate or attractive valuations of a different category of investment. This is a reasonable and fair distinction.

What Breaks the Growth Run This Time?

If what broke the growth tear of the 1990s was a bubble burst—a valuation excess that peaked, rather than a fundamental event catalyst—does that mean the current “growth run” is also to run free and clear until such time that the valuation limits finally give way, a phenomenon knowable only in hindsight?

Maybe. Some may even say probably. But not necessarily.

Fundamental events here are also worth considering, and to the extent that none of them materialize, I strongly recommend remembering the valuation concern as a backup. What are these potential catalysts that may or may not precede a valuation excess limit?

- Will the U.S. hold a monopoly on AI the way it effectively did with the internet, and the way it most certainly did with smartphones? Perhaps. But, you know, perhaps not. Is DeepSeek real, or is it a DeepFake? Is there an AI ecosystem in the U.S. that is impenetrable by foreign competitors?

- Antitrust or regulatory concerns. The DOJ’s preposterous suit against Microsoft at the end of the tech boom was not exactly the catalyst for the tech boom’s demise, but it didn’t help Microsoft. Do other Mag-7 names face judicial and regulatory scrutiny that changes their business models enough to at least effect things on the margin? (i.e., Apple and its app store practices, Google and its ad/search practices, Amazon co-owning cloud and e-comm, Nvidia and export controls). Maybe, maybe not.

- Is AI capex going to decline?

- Is AI capex going to not decline, but with AI hyper-scalers wishing it had declined? In other words, is there a risk of disappointing ROI for the AI customers driving the whole thing?

These are not slam-dunk catalysts to pain and suffering. I would hesitate to put odds on any of them, but if I were doing so, they would not be > 50% probability events. But none of them are 0% probability events, either.

Conclusion

I do not know if there will be particular catalysts for the onset of challenges in the high valuation-growth sectors of the market or not. I do not know when valuations will hit a peak, and I do not know how severe the correction will be when that does happen. What I know is that the investment practices of far, far too many have been to buy what feels good, now, and not what ought to feel good, later.

There is, and always has been, something called a “value trap.” Investors put into practice the Proverbs 20:14 idea, only to find out that the reason it felt so bad was because, lo and behold, it was broken. Not everything that is cheap is attractive, if cheap is the condition that merely precedes the condition known as extinct. It can happen, though less than you may think.

But value remains a risk-adjusted tool for the ages. And it is not gone, and for many of us, it is not forgotten. We strongly prefer to receive the rewards of the risk we take in good-value businesses via the growth of the dividend we receive (talk about measurable and objective). But that application of received profits is still a subset of value (and growth) mentality. Perhaps the problem is believing that value is somehow anti-growth. Well, I have some news for everyone:

There is no “value” – where there is no “growth.” The value comes in the price paid for future growth.

And yes, some “growth” is bigger than others. But the problem, my friends, is that some valuations are bigger than others, too.

Quote of the Week

“A pessimist complains about the noise when opportunity knocks.”

~ Oscar Wilde

* * *

I wrote most of this Dividend Cafe on Thursday this week, and of course, by Friday morning, as I was wrapping it up, the overnight Israeli strikes against Iranian nuclear aspirations had taken place. I am confident that more will be covered on Monday in terms of impact on the energy sector, markets, and broader geopolitics.

Brian Szytel will bring you the Dividend Cafe on Monday, as I will head out of the country with the family on Sunday for a week away. I will be back with you for next Friday’s Dividend Cafe, but Brian will take on the mid-week writing and such. As we get into the second half of June to bring the first half of 2025 to a close, there are some very fun Dividend Cafes lined up. In a time where it often feels like value does not matter, value is exactly what we aim to provide in the Dividend Cafe. To that end, I work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet