The bible tells us, “Pride goes before destruction, and a haughty spirit before a fall” (Proverbs 16:18) a warning about overconfidence and how arrogance frequently leads to failure. In our culture, we often hear these famous last words precluding a fall, “It’s a sure thing.”

If you’re a frequent visitor to Thoughts On Money then you know I love the game of basketball. I love playing basketball, talking basketball, watching basketball, and anything else that relates to the game of basketball. My wife can attest to the fact that I even sometimes let our two-year old eat in the living room with me, so we can watch the game during dinner – of course, this is absolutely justifiable, as we are amidst the NBA playoffs.

Today on TOM we will discuss basketball, Bitcoin, leveraged ETFs, gambling, and why investors should always beware of a sure thing. What a combination of topics! And off we go…

Zero for Nineteen

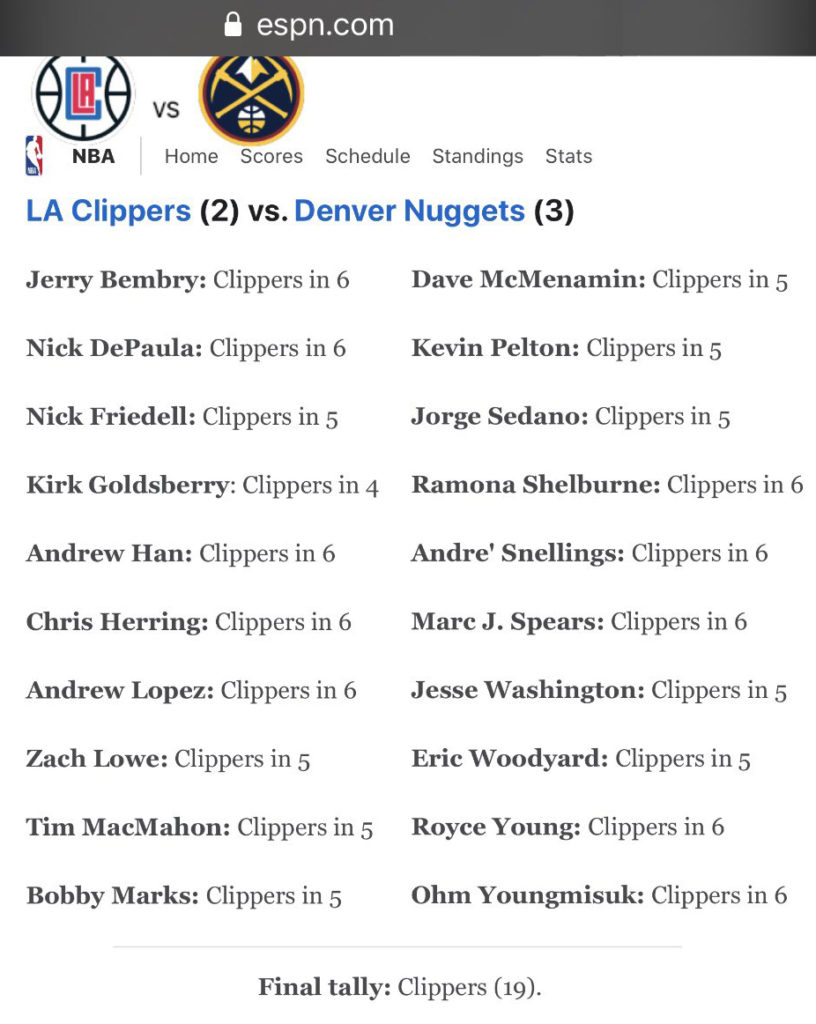

A wild thing happened the other night, the Denver Nuggets who were down 3 – 1 in a seven games series won three games in a row to knock out the championship favored Los Angeles Clippers. A Clippers team that acquired two of the best players in the league in the offseason and were expected to be the team to beat. Now, the playoffs go on less the Clippers.

Everyone believed the Clippers were a sure thing. Here were the predictions of 19 well-respected ESPN analysts prior to the series:

Source: ESPN

For these analysts, most of them won’t think twice about this false prediction. They are paid to forecast, predict, and pontificate about their opinions. They are wrong all of the time and that’s ok, as rarely does anyone keep tallies of their track record. There is no money on the line for them, it’s just another day in the office. In this case, 19 out of 19 analysts were dead wrong.

The real losers in this story are the countless gamblers who leaned into this consensus prediction and did put money on the line, hoping to prosper from this sure thing. Some lost pocket change and others probably wagered beyond what they could afford to lose.

What was the recipe for this disaster? As I said, the Clippers made two HUGE offseason signings, and these household names – Kawhi Leonard and Paul George – started a spark of expectations before the season even started. The herd of fans and pundits that touted the teams expected success further amplified this sure thing mentality. It’s these types of inputs and influences that feed into overconfidence and quietly build up biases that we are often unaware of.

Google: “Bitcoin”

We see this same story play out in finance all the time. An investment or strategy begins to yield some success, its popularity grows, the herd jumps on the bandwagon, and short-lived early successes start to provide this impression of perpetual bliss. This is how bubbles are formed. The problem is that you never know exactly how big a bubble can get and often it grows bigger than you expected which thickens the allure and magnifies the eventual burst.

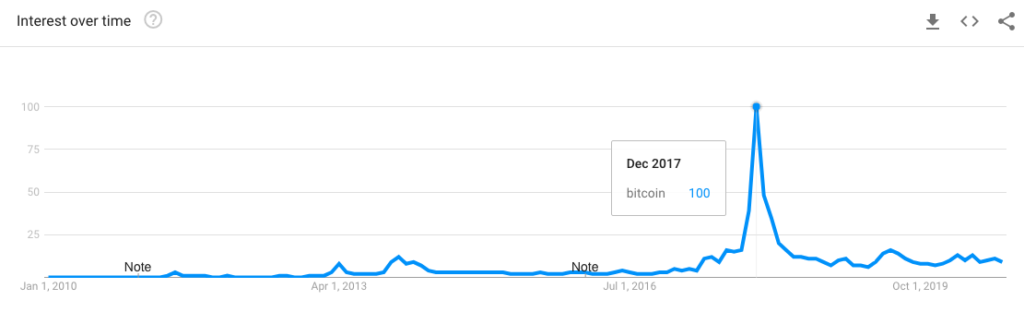

In basketball, this year it was the Clippers, but in 2017 in finance, it was Bitcoin. You couldn’t go a day without reading a Bitcoin headline, overhearing a coffee shop conversation about Bitcoin, or getting a text from a friend wanting to chat all things crypto-currency. Here is the search popularity on “Bitcoin” from Google trends:

Source: Google

The search popularity peeked in December 2017; you know what else peaked in 2017? The price. Nearly three years later and this crypto-currency is trading at a price almost 50% lower. Just like our sports analysts, many people had a lot to share about Bitcoin in 2017, there definitely wasn’t a lacking of opinion, but it was the part-time speculators that really felt the pain of this price pinch. Investors piled into what they thought was a sure thing and then felt bamboozled when they learned that the momentum carried in both directions – what was once skyrocketing was now plummeting.

Tripling Down

So, why write this article now? Was this just an excuse to chat basketball? No, although I do enjoy taking basketball. It was this cringe-worthy Bloomberg headline that inspired today’s conversation:

Source: Bloomberg

Investors have seen the year-to-date performance of the Nasdaq, which is littered with familiar tech names, and they’ve decided to double down and triple down their investing dollars on this speculative bet. These investors feel like this is a sure thing.

Here’s what scares me, you know how we all know the facts about the long term negative effects of nicotine yet many still choose to ignore this truth and indulge, these triple leveraged products are the exact same. Here is a direct quote from a proprietor of these leveraged products, “Investors who choose to hold leveraged ETFs for periods longer than a single day should recognize that their holding period is not in line with the fund’s investment objective and such investors should regularly monitor and adjust their position to maintain a level of exposure consistent with their investment objective.” (Source: Direxion). I will repeat for emphasis, “Should recognize that their holding period is not in line with the fund’s investment objective.” This is the surgeon general basically telling you that these things are lethal. A product meant for professionals to use for short term hedging purposes has become the drug of choice of your average retail investor.

Focus on the Plan

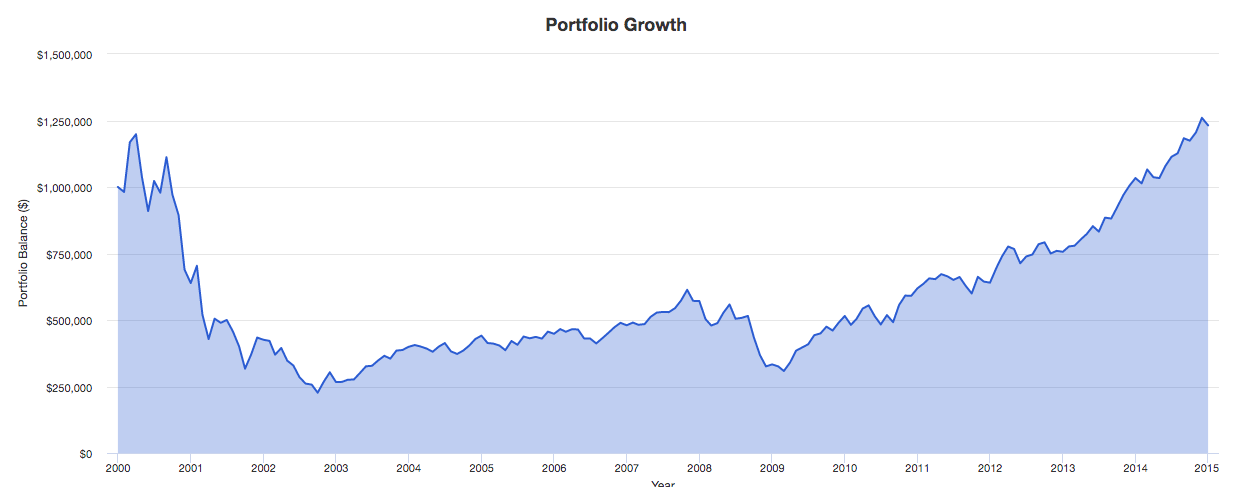

Let me help you out – your financial plan doesn’t need “a sure thing” and it might not be able to endure a detrimental misstep caused by a misallocation of capital. Sticking with our themed example of the Nasdaq, here’s an investor’s experience who piled a $1mm into the Nasdaq in the early 2000s and spent nearly 15 years underwater, having to endure one period where the portfolio depreciated in value greater than 80%.

Source: Portfolio Visualizer

Please don’t misinterpret what I am saying – this discussion is not a discussion about disparaging cryptocurrencies or the technology sector. The examples I could have provided go much beyond these assets – we could’ve explored the history of gold prices, or the Nifty Fifty, or Japanese equities in the late ’80s. The real take away is to beware of the lure of speculation – getting sucked in by a fear of potentially missing out, being seduced by temporary or early success, and then being left to pick up the pieces when things fall apart. Again, your financial plan doesn’t need a sure thing; it shouldn’t rely on the stars aligning.

Calculated

A lot of what we are discussing today seems like the greatest harm is created when someone finds himself or herself gambling with their investment accounts. This is true and I want to hone in on that word “gambling.” We often associate gambling with this thought of polarizing outcomes – win big or lose big and we equate the outcome to luck, not skill. Yet, we also know that some do make a profession of gambling, so how do they do it? The great ones always think in probabilities. If you’ve watched a World Series of Poker Event you know that on TV each player’s hand always reflects their odds and these players are constantly sizing their bets based on those probabilities. We see the probabilities calculated for us on the TV screen, while the players are responsible for doing that mental math on their own. A great poker player knows the damage emotions can cause on their game, they even have a word for it, they call it being on tilt. A player on tilt stops sizing bets based on probabilities and they lean on their emotions generated by previous hands – this is typically a death sentence in the game of poker. A great poker player knows that there is no such thing as a sure thing, they never wager more than they can afford to lose, and they understand the destruction caused by overconfidence.

Amateur poker players don’t operate like professionals. They go to Vegas with some allotted “fun money” and they are often content to leave that “fun money” in the casino chalking it up to entertainment. Amateur investors don’t operate like professionals. They go out seeking BIG wins and often risk more than they are aware of. Investment professionals like Financial Planners know that it’s not about hunting for big wins, they prioritize risk management, and know that the investment portfolio has just one objective – meet the needs of the financial plan. This is an important truth to note, look at the order, 1st a financial plan is created and 2nd an investment portfolio is designed to meet the needs outlined in that plan. Most of the world has this backward, they set out to 1st design their investment portfolio and then just hope it will create some future benefit for them.

A Sign of the Times

I am writing on this topic today because I am concerned that these destructive distractions are alive and well right now. Like I said, that Bloomberg headline scares me. Maybe the work-from-home movement is leading to a spike in amateur investing, maybe the lack of sports is attracting gamblers to the stock market, I can’t pinpoint it exactly but I can smell the speculation in the air. Be careful out there. The headlines, the coffee shop conversations, the posts on social media will try to lead you astray – resist. Remember, pour your focus and energy into calibrating your financial plan and then work with your advisor to affirm that your portfolio harmonizes well with your plan. This will bear much fruit.

With that, I will sign off. As always, please reach out to me at with any questions you might have. I will be back next week with more of my Thoughts On Money.