Time Shares

Exciting news…

You’ve just won a free trip to Hawaii!

What’s the appropriate response to this news? I’d say there are two potential reactions:

- Yippee!!! When do we leave!?

- What’s the catch?

I hate to be labeled as a pessimist or a doubting Thomas, but I absolutely fall into camp #2 or the what’s-the-catch camp.

For this fun little hypothetical, there is a catch. You actually have to “earn” your trip by enduring a timeshare presentation. If you are new to adulting, this could be a foreign concept to you, but if you’ve got a few gray hairs and some experience under your belt, you’d probably rather opt for a root canal than a timeshare presentation.

The key principle I am trying to get across here is the importance and value of reacting inquisitively versus blind excitement. Let’s call this the “tell me more…” principle.

I want to encourage you to use this tell-me-more principle when it comes to investing. Your neighbor tells you that he doubled his money in the last 6 months, tell me more… You see on TV that gold is up over 50% on the year, tell me more…

I can’t teach you how to be an analyst in a 1,200-word article, but I want to give you a framework for how you can lean into your inquisitive side and allow your emotions and excitement to take a backseat in the moment. I believe it will make you a better investor.

Today, I’d like to unpack:

- Concentration

- Multiple Expansion or Earning Growth

- Attribution

- The Boom & Bust Cycle

I believe these concepts, vocabulary, and framework will equip you to be a better tell-me-more investor.

Concentration

Have you ever tasted a child’s first attempt at homemade lemonade? Most first attempts will leave you quite puckered with that burning citrus sensation in your throat. For most people, it’s just not intuitive how much sugar is needed to cut the concentrated sour power of a fresh-squeezed lemonade. Water and sugar are a way to dilute that citrus potency.

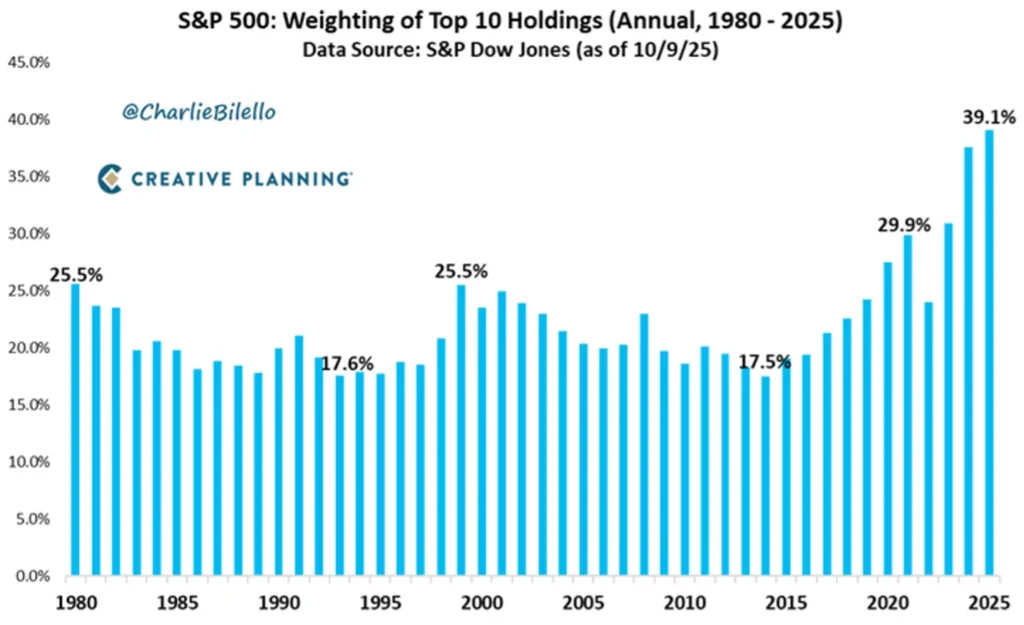

Investing can be quite similar; an overconcentration in one investment or one stock can result in an overpowering outcome. As it stands today, the top 10 companies in the S&P 500 make up nearly 40% of the index. Said in a simpler fashion, every $1 invested in the market allocates 40 cents to the 10 largest companies.

Source: Charlie Bilello, October 23, 2025

This reality should pucker your face in the same fashion as homemade lemonade lacking sugar. If diversification is the first and most important rule of finance, and if we are encouraged to memorize adages like, don’t put all your eggs in one basket, then this reality simply ignores that foundational wisdom.

So, the market is up roughly 15% on the year. Should my reaction be “Yippee!” or “Tell me more…” The reality is that this 15% return is being driven by a small selection of heavily concentrated positions (companies).

This truth alone shouldn’t be concerning; I need to pull on this thread a bit more. I want to know why these particular companies are growing in value. I want to know what exactly is driving the prices higher.

So… tell me more…

Multiple Expansion or Earnings Growth

Here’s a simple reality about the stock market: there are only two things that drive a stock price up or down. Either the company improved its profits (earnings), and this drove up the stock price, or the profits haven’t changed (yet), but investor enthusiasm about the company’s future potential drove the price higher. Or a combination of both. Stock prices rise based on earnings growth or multiple expansion. Multiple expansion is an improving enthusiasm/sentiment, driving investors to pay higher stock prices even without (or before) profits have grown.

One of these drivers can be explained by simple fundamentals (improving earnings), while the other is completely dependent on improving sentiment. One is quantitative, and the other is qualitative.

Let me ask you, which seems like the more solid foundation and lasting impact, improved fundamentals or improved sentiment? A basic study of stock market history will show that earnings growth, in the long run, has a high correlation to stock market returns, while multiple expansion is a mean-reverting metric. The market magnetizes towards its long-term earnings multiple over time. Paying an above-average price (multiple of earnings) historically has led to a lower future expected return as the price is naturally pulled (contracting) towards its long-term average.

That was a mouthful, but the simple tell-me-more truth you want to uncover is whether your investments are growing in value based on earnings or investor excitement. The hope is the former versus the latter.

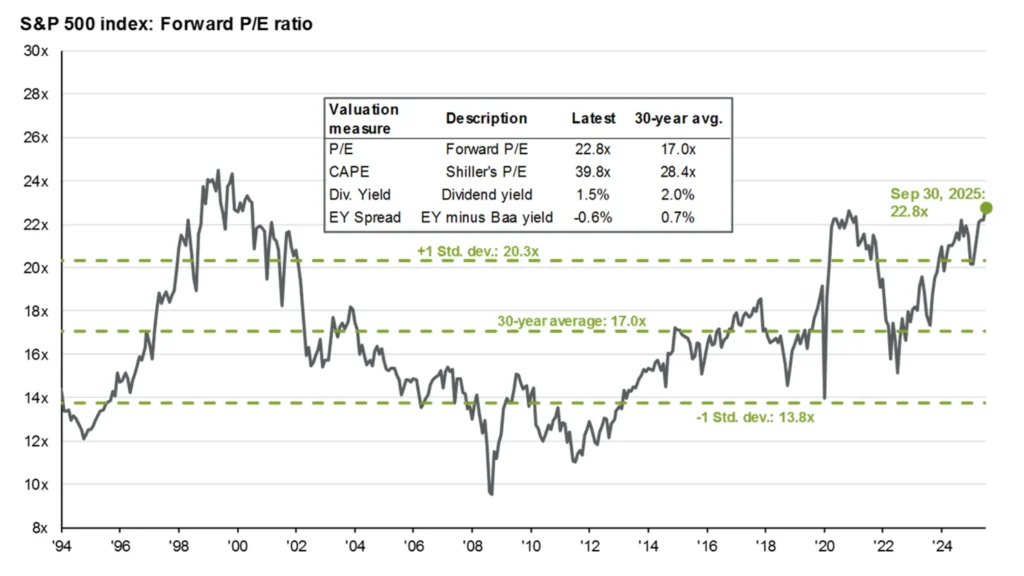

Here is what that multiple expansion has looked like over the last handful of years (see below). As you can see, earnings are growing, but not as fast as prices (multiples).

Source: JPM, October 23, 2025

Attribution

So, now I’ve begun to understand the reality of concentration and the impact it can have on my portfolio. I now know that prices can increase based on clear quantitative reasons or more squishy qualitative realities. Next, I want to understand which investments are having the greatest impact on my bottom line.

Let’s imagine I have 10 stocks that I own with an equal-weighted allocation in each. 10 companies, all with a 10% allocation. Then, let’s imagine that 9 of these companies deliver a 0% return and 1 company a 100% return. How much has my total portfolio grown by? 10%. And what is the attribution based on the individual constituents within the portfolio? Well, one company accounted for all of the returns. The 10% bottom-line increase was fully attributable to the 10% position that doubled in value.

Leaning on our new understanding of earnings and multiple expansion, my hope would be that this 100% gainer grew based on improved earnings versus just improved investor enthusiasm around the stock. If not, there should be a concern about what goes up, must come down – the gravity principle.

Is my portfolio overly concentrated? What exactly is driving my returns – earnings or multiple expansion? What positions have the highest attribution to my bottom-line return? As a tell-me-more investor, I want the answers to these questions.

The Boom & Bust Cycle

Now, here comes the if-list.

If I own a portfolio that is highly concentrated in a few companies or sectors. If this portfolio is primarily growing based on improving sentiment and investor enthusiasm, as opposed to earnings growth. And if most of my returns are attributable to a small concentration of companies, then there is a good chance that I’m also going to be highly susceptible to the boom-and-bust cycle.

These cycles are best described by exaggeration. Swings up of enthusiasm, greed, and euphoria exaggerate returns to the upside. And eventually an equal force in the opposite direction, driven by disappointment, fear, and pessimism, exaggerating returns to the downside.

I often describe this as the race the hare ran. Aggressive sprints that expanded his lead versus the tortoise, then lazy and prideful rest that led to his ultimate defeat. As advisors, we often talk about “behavioral coaching” and the value we provide when helping clients avoid big mistakes in down markets. I don’t think there is enough written about the “behavioral coaching” in the frothy markets where one needs to be convinced that good returns are the target, not best returns.

I promise you, as much as you think you want to participate in all of the boom, you don’t. Why? Because if you partake in the boom, you won’t avoid the bust. It’s these boom-and-bust cycles that will cause the most damage to an investor, financially and psychologically.

Tell-Me-More

So, how about that Hawaiian vacation? A free trip too good to be true? Yes.

When interviewing, my favorite quality in a candidate, after coachability, is an insatiable curiosity. I want the same for you as an investor; I want your bent to be tell-me-more. I don’t want you to get enamored with outcomes, but rather inquisitive about what is driving those outcomes.

I love basketball, and I don’t have time to watch every game. So, I regularly check the recap of scores around the league. If I see a surprise blowout, where an underdog really gives a beating to a contender, I always want to see the box score. I go straight to shooting percentages, and if I see that a team shot 50% from the three-point line, then I know this is (1) what won them the game – a great shooting night and (2) not something that is easy to replicate on a regular basis. We need to pull on those same box score threads when we are assessing our investment portfolio or a potential investment. We can’t stop at the excitement of the outcomes and final scores; we need to understand the why.

Again, I can’t teach you to be an analyst in a short article like this, but I hope I have better equipped you with this framework and the simple reminder to lean into inquiry over excitement.

Until next time, friends…