Guest Author – James Andrews

Building Elevators

My dad has spent over 40 years building elevators & escalators all over the world. He chose a trade school in lieu of college, studied motor control systems and has worked for almost half a century building every variation that exists today (ever seen the world’s first spiral escalator in Las Vegas?). As you can imagine, he is excellent in his field and has a high degree of confidence working with his hands. When I purchased our home a few years ago, Dad was all-in with helping me finish the renovations. After all, if he could build an elevator all the way in Japan, then surely a home project in sunny Orange County would be a no-brainer. Turns out that rigging up elevators is not the same as stringing backyard lights. I recall one weekend where the simple task of stringing lights in the backyard took us at least three trips to Home Depot and over 9 hours. His competence in building elevators did not always translate to stringing lights or building furniture. In other words, the gap between what he knows and what he thinks he knows can sometimes make life more difficult. (In all fairness, I wouldn’t survive one month of homeownership without him – love you, Dad!)

Play to Your Strengths

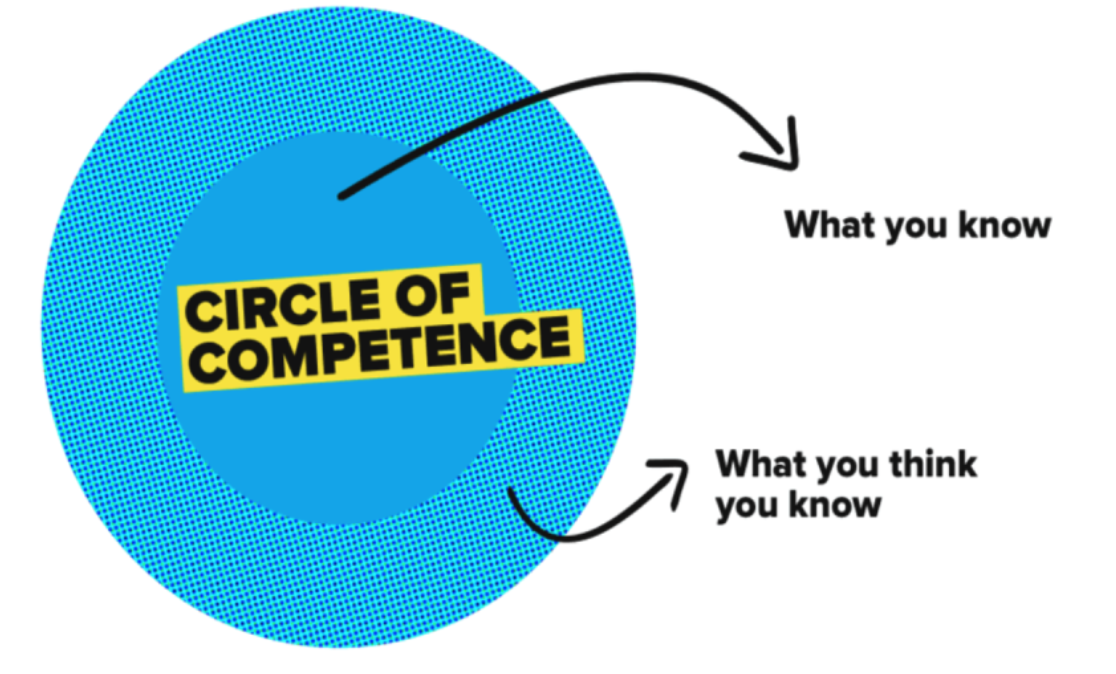

As we continue to learn about Mental Models, those decision-making tools that allow us to learn from fundamental truths, we enter the world of Warren Buffett and his belief in Circles of Competence. Circles of Competence are those areas where you have a unique skill that gives you an advantage. For my dad, his circle of competence is building elevators and escalators. He’s built them for many years and has accumulated a deep well of technical knowledge and experience that makes him an expert, but that does not always translate to other projects. Warren Buffett coined this idea in his 1996 Shareholder Letter. He saw that we all have two circles of competence when it comes to investing:

“What an investor needs is the ability to correctly evaluate selected businesses. Note that word “selected”: You don’t have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

*For Illustrative Purposes Only

Smart in Spots

Everyone has a circle of competence, which is to say that each of us has unique talents, experience and perspectives that allow us to excel in a given field. For many of us, that core competence is tied to our career. It’s where we have the most education, mentorship, experience, knowledge, and passion to grow. This philosophy was embraced by Tom Watson, the Founder of IBM, who shared:

I’m no genius. I’m smart in spots – but I stay around those spots.”

Tom Watson has built an incredible company by focusing on the things he was good at and avoiding the areas where he lacked competence. The concept I like most about the Mental Model is that it underscores the two disciplines required to build lasting wealth: Offense and Defense.

Growing the Nest Egg

Offense is your ability to earn and accumulate wealth. Applying your core competency where the competitive advantage works in your favor and provides the “premium” the market will pay for those talents. As a wealth advisor, I have the unique perspective of working with many families who have built their wealth in a variety of ways. From entrepreneurs to engineers, attorneys to architects. The through-line in their stories is always the same: they honed a marketable talent, spent all their time doing just that and outsourced the rest.

I recall one friend who is an exceptional realtor in Santa Barbara, CA. He learned through experience that the biggest driver of his retirement is selling the next home, not by spending hours crafting the perfect stock portfolio. Considering this, he aggressively outsourced anything that would distract him from his core competency, thereby freeing up his workday to do the things that offered the most value. Like Tom Watson, he knew those “smart spots” and outsourced the rest.

Protecting the Family Jewels

If offense is the accumulation of wealth, then defense is protecting what you have earned. For many families, defense is their ability to minimize financial mistakes. The discipline to avoid the areas where (a) your experience isn’t as deep, (b) the education hasn’t been acquired, and (c) you’re more likely to miss an important detail. I often call these actions unforced errors or mistakes that were caused by a lack of understanding rather than a market-moving event.

As I consider this topic, the application that causes me the most concern is this: how to understand the difference between what I truly know and the things I only think I know. In other words, how do I score points on the offense (the things I know) and reduce my chances of losing on the defense (the things I only think I know)?

Exposing Your Blind Spots

Below, I have identified three practical steps that can help you avoid those unforced errors I mentioned earlier. By their nature, blind spots are unanticipated gaps in your knowledge where overconfidence or misinformation can bring more harm than good. As someone whose career depends on providing helpful advice to families, I am acutely aware of the dangers my own blind spots can cause for clients. Over the years, I have developed a series of habits that help to reduce the likelihood of walking into a blind spot. You may find some of these to be applicable in your life.

- Diversify Your Research: We live in a world where the biased news cycle and sophisticated computer algorithms push us into echo chambers that mirror our personal preferences. Challenge yourself to diversify your news sources and expose you to different perspectives. If the content you consume does not challenge your ideas or make you feel uncomfortable, perhaps it’s not diverse enough.

- Understand Your Boundaries: Mastering a topic to the point you can teach it to others is a great way to ensure a deeper understanding. For example, my wife has zero interest in anything to do with finance. So, if I’m going to make a financial maneuver, I should have a level of mastery to teach the nuances to my wife in a way that she also understands the technique. (My poor wife has had to sit through many of these exercises). In tandem with this, meet with individuals whose circle of competence clearly overlaps with the topics you are seeking to learn.

- Time Buffer on Decisions: I avoid giving immediate advice at all costs. Unless deadlines dictate a quick response, my preference is to marinate on all recommendations for at least a week, sometimes longer, depending on the magnitude. Do not make financial decisions lightly or quickly. What is done cannot always be undone.

In Closing

There is perhaps no greater contributor to wealth creation than understanding your Circle of Competence. This simultaneously offers you the greatest opportunity to build the nest egg while also bringing awareness to the limitations that can veer you off-course. Over time, I encourage you to expand your Circle but always be realistic about where it stands today.