The Big Four Zero

Correlations can change over time.

Let me give you an example…

Next year I am turning 40. So, naturally, I am enjoying my last year as a thirty-something. Being on the tail end of this decade, I’ve become well acquainted with a correlation that never really existed before. All of a sudden, what I eat and how much I eat has a direct impact on how much I weigh. This is a very unfortunate correlation and one that was absolutely not invited.

The deterioration of my once beautiful metabolism has started to rear its ugly head. I used to be able to eat anything and as much as I wanted of that anything, and it had no impact on the scale. Oh, those were the days.

Again, correlations can change over time.

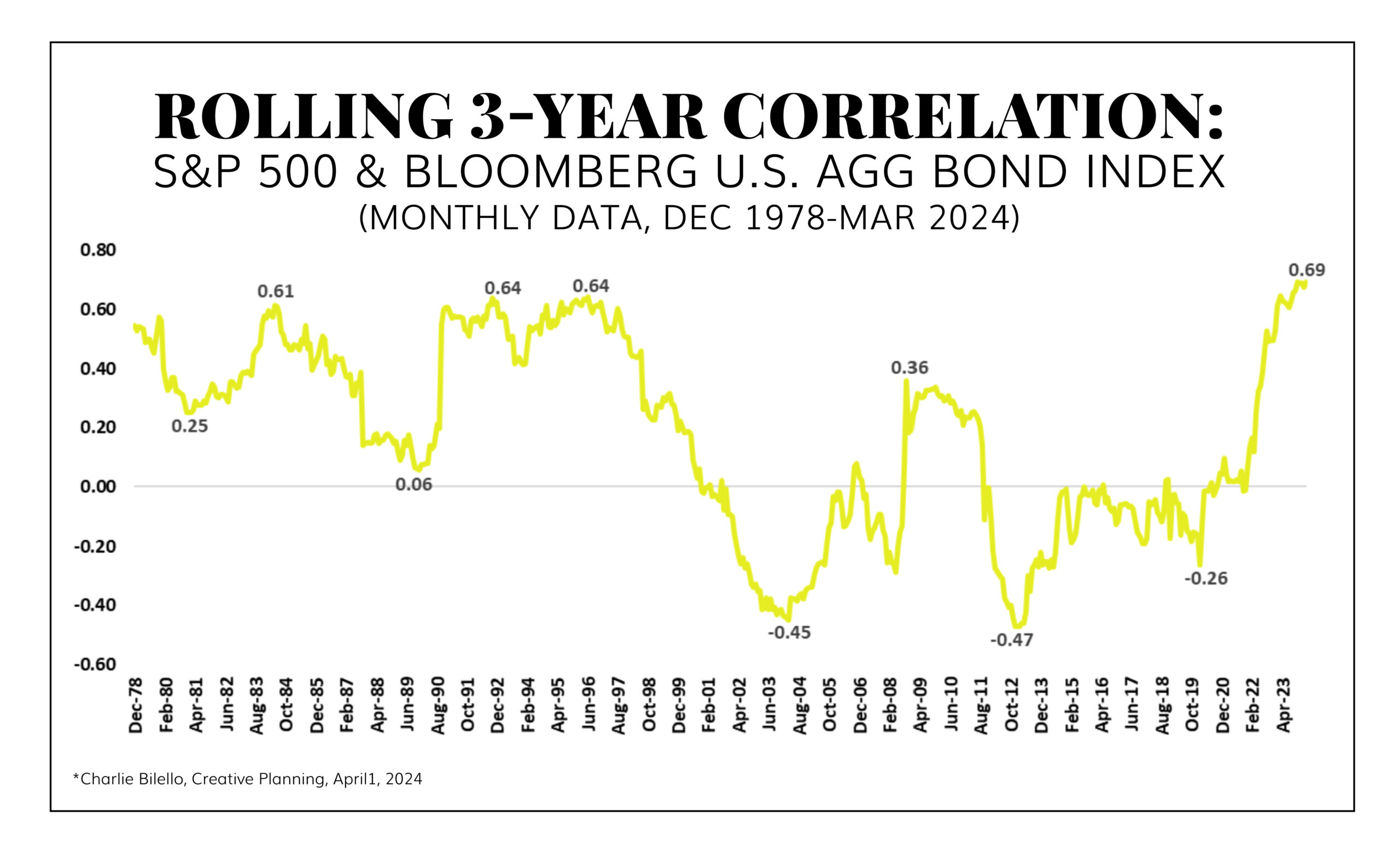

Twins: Stocks & Bonds

Here’s an interesting tidbit about 2024 that David Bahnsen shared recently:

The correlation between stocks and bonds is stronger today than it has been in the last 40-plus years.

Let me give you a bit more context for what this data means and why it should matter to you. In math, when a correlation is 1, it means that the two things being compared move in lockstep together – one goes up, the other goes up. A correlation of -1 means that as one goes up, the other does the exact inverse. Anything between -1 and 1 simply represents the magnitude of that connectedness.

Correlations remind me of a swingset on the school playground. Imagine you are back in 4th grade, and you and your recess pal are swinging together. The challenge you propose is to try to swing in unison—matching speed and height and staying in sequence as you swing back and forth. This rhythm is difficult to find, so sometimes you are in synch, and then small variations take you out of the pattern. This is a lot like correlations and how they can modify and/or evolve over time.

All Your Eggs

Again, why does this matter? Well, the age-old wisdom in personal finance is to be diversified. You’ve heard the old adage, don’t put all your eggs in one basket. Diversification is all about picking investments that are not perfectly correlated. Simply put, you hope that when your stocks are struggling, your bonds will buoy your portfolio and vice versa.

Yet, when these correlations change, as the chart reflects, you lose the potency of that diversification. This is one of the key issues that investors have been facing over the last few years. For example, in 2022 both stocks AND bonds delivered a negative double-digit return, a very ahistorical event.

Let’s pull on this thread a bit more. Why is diversification important? To get this answer, I think we need to first ask what is the purpose of our investments? The purpose is to grow wealth that will be spent later. The spending part is the key. You want diversified investments that don’t behave similarly or mimic one another so that when you need to sell and spend a portion of your investments, you have options of what you could sell. If your stocks are down, you resource your bonds. If your bonds are down, you resource your cash. You get the idea.

In a world where stocks and bonds are starting to copy each other’s every move, you have a potential problem. In a year like 2022, you either had to sell some stocks that were down 20% or sell some bonds that were down 10%. This problem begins to amplify if bad results start to recur multiple years in a row (sequence-of-returns risk).

An Alternative Approach

So, what is an investor to do? For the reasons explained above – and others – is why we [The Bahnsen Group] prefer to manage a portfolio of diversified income sources. Investments that produce income distribute that income and grow that income on an annual basis. We will look to buy a collection of investments like dividend stocks, income-producing real estate, private loans, etc. The intent of this portfolio is to produce tangible income – that you can touch, see, and spend – whether you need to spend it now or later. If later, you resource it to buy more shares. Then, when you are ready to spend it, you allow that income (dividends, interest, rental income, etc.) to simply be deposited into your checking account on a monthly basis, just like a paycheck.

At the heart of diversification is this desire to combat volatility and stabilize the value of your portfolio SO THAT you can reasonably withdraw from that portfolio on a consistent basis. This is where you get that classic “4% Rule,” based on some comprehensive research that concluded what is a sustainable withdrawal rate from a portfolio. This is where you derive the need for Monte Carlo simulations, an exercise that stress tests your portfolio through different potential market outcomes to test the probability of you outliving your nest egg.

A portfolio built around a core strategy of dividend growth complemented with other diversified income sources really allows you to tune out the 4% rule and Monte Carlo simulations. Instead, you focus on building a diversified income that can sustainably support the lifestyle you want to live. This concept and approach should offer relief. It should take away a lot of the anxiety, speculation, and guesswork out of your financial plan.

In Closing…

It’s also important to remember how stable investment income is compared to investment prices. Sure, dividend stock prices can jump around much like that of the general stock market. Yet, a thorough study of history will reveal that dividend income measured year-over-year is actually not subject to the same volatility. It is rare that the year-over-year dividend income of the stock market would decrease. Furthermore, in most cases of an income decrease, the pay cut is marginal. This is a truth that you won’t hear on daytime finance television because it’s much less exciting than discussions around the second-by-second moves of stock prices.

So, if your current approach to investing is causing you stress and anxiety, perhaps it’s a good time to go back to the drawing board. Perhaps you will come to the same conclusion that I have, and you’ll choose to diversify via dividends.