Years ago, my days were not spent crafting investment plans and partnering alongside clients for their financial hopes and dreams. My days were instead focused on scoring goals on the soccer pitch.

In soccer, there are two basic strategies to score goals. The first strategy is called the “build-up” approach. Your team strings together 10, 20, or 30 passes in a row, slowly working the ball up the field towards the opposing net. Once you get close enough, you hope for your team to get a quality shot on net.

The second strategy is the “counter-attack.” Your team purposely sits back on defense, letting the other team have possession of the ball. You wait, wait, wait, but as soon as your defense takes the ball, you counter-attack by sending all of your players forward as fast as possible.

The ultimate goal is the same as the build-up approach – to get a quality shot on net. Yet, the approach is vastly different. The counter-attack provides a greater opportunity to score a quick goal but also carries more risk (as you no longer have defenders on your own side of the half).

What do these two approaches to goal-scoring in soccer have to teach us about finance?

We’re going to look at two approaches to investing cash you might have on the sideline. The first is via lump-sum, and the second is via Dollar-Cost-Averaging.

Cash, Cash, and More Cash

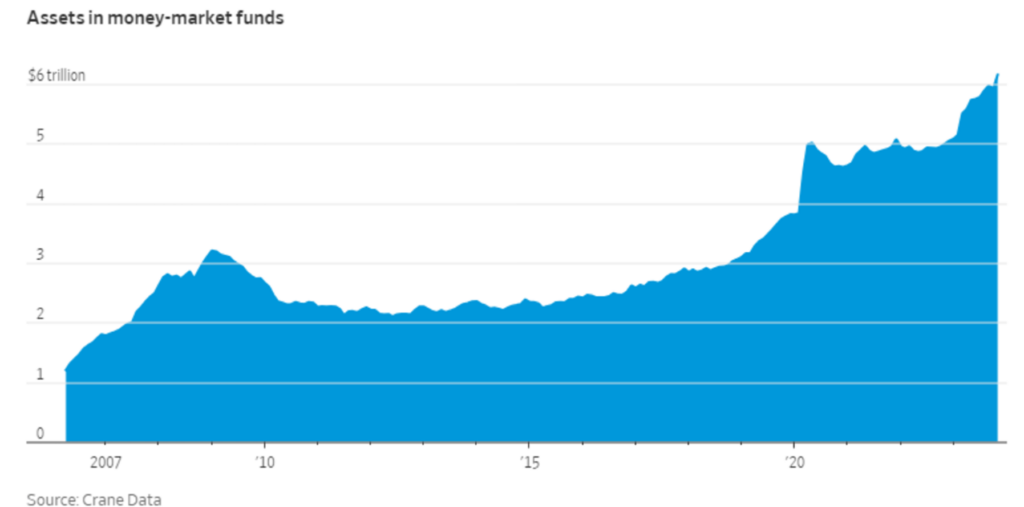

Investors have more cash (and cash-like instruments) than ever sitting on the sidelines. Whether it is from a home sale, business liquidation, sales of stocks and bonds, or simply building cash over time, assets in money-market funds have reached an all-time high (over $6 trillion – see picture below).

*Source: Crane Data, Jan. 19, 2024

With high current valuations in the stock market, many investors have become paralyzed. Most investors know they should do something about that cash on the sideline (see: What is Risk Anyways), especially with the Fed set to cut rates later this month (and therefore income on cash set to decline). However, in my conversations with investors, many simply don’t know how to effectively get back into growth-oriented investments.

Let’s explore a couple of the options…

Lump-Sum Approach

Assume an investor sells a vacation home for $1.2m. After receiving the proceeds in cash, he decides to invest all $1.2m at once. To revisit our soccer analogy, this is the counter-attack (or “all-in”) approach. The goal is to get invested as fast as possible. The idea is quite intuitive to most people, yet it comes with timing risk. What if the market plummets the day you invest all of the cash?

Dollar-Cost-Average (DCA) Approach

The principle behind a DCA strategy is that an investor takes cash-like investments and, instead of investing it all at once, they invest a small portion every month (or week, or quarter, etc.) over a defined timeframe. For our investor selling a $1.2m vacation home, he might decide to invest $200k/mo for the next six months.

This parallels the “build-up” approach in soccer. The goal is to slowly, methodically “move the ball up the field” toward the ultimate goal of being fully invested in a diversified portfolio. You might miss out on some upside, but it mitigates much of the timing risk. Some also like this approach due to the fact you buy more shares if the market declines, and you buy less shares if the market increases. Buy low, right?

So, Which One?

From a pure numbers standpoint, an investor typically ends up with more wealth at the end of the period by utilizing the lump-sum method. This is because of the simple fact that the market tends to increase more than it decreases (see Records are Made to be Broken).

But “ending wealth” is not always the ultimate goal. From a psychological perspective, DCA’s can be very helpful to mitigate the fear and regret that can potentially be triggered from investing all at once. A DCA approach can also unfreeze a paralyzed investor, and allow them the opportunity to slowly add money back to growth-oriented investments.

A question I enjoy asking is, “What would make you feel worse? 1.) You invest all your money, and the market immediately goes down 20%, or 2.) You DCA your money slowly over time, and the market immediately goes up 20%?”

The answer to this question is illuminating.

Splitting the Difference

Of course, you don’t have to do either the lump-sum OR the DCA approach. You can do both. Our friend who sold his vacation home might choose to invest $600k upfront, and then DCA $100k/mo over the next 6 months. This mitigates some of the timing risk (if the market happens to drop when the initial $600k is invested), but it also gets the money working quicker than a straight DCA approach might.

Food for Thought

- The biggest piece of advice I have is… DON’T OVERTHINK IT! Our readers are likely aware that cash is not the best long-term investment. So, choose one of the three approaches above, and stick to it. One of the worst things an investor can say is, “I’ll get in when I feel good about things”. When things “feel good”, it’s often too late, as the market prices in both bad news and good news.

- Diversify – If you’re shifting from cash to the S&P 500 index, know that the top ten stocks account for 37% of the index as of June 24th, according to FactSet data*. That doesn’t sound very diversified to me. A well-diversified portfolio may have some US stocks, international stocks, preferred stocks, fixed income of various durations and credit ratings, and private markets exposure. For an overview of how The Bahnsen Group thinks about building portfolios, see Trevor Cumming’s article titled “Magnify Revisited.”

- Built-in DCA – For clients who are accumulating, know that a DCA approach is built into our system of Dividend Growth stocks. Imagine I have 100 shares of stock worth $100 each ($10,000). This hypothetical stock pays a $5/share dividend. If the stock stays at $100, my annual dividend is reinvested to purchase 5 additional shares. If the stock decreases to $80, however, my dividend just bought 6.25 additional shares. For an accumulator, volatility becomes your friend over the long run.

If you have a lot of cash on the sideline, know that you’re not alone. The allure of money market funds yielding 5% has tempted many investors. But with yields set to decline, consider a disciplined approach to adding money back into growth-oriented investments.

As trusted advisors to our clients, we love coming up with solutions that help ensure you stay on track to reach your financial goals.

As always, reach out to discuss which plan might work best for you.