As a 14-year-old, my first job was as a bicycle mechanic in my dad’s bike shop.

Despite my lack of mechanical skills, I enjoyed biking. My preference was for BMX and mountain biking, and at the time, I had no interest in joining the spandex-clad group of road cyclists.

These customers would enter our shop laser-focused on optimizing every detail. Lighter saddles, carbon fiber water bottle holders, strange-shaped helmets—it all seemed excessive. A metal water bottle cage was good enough, right?

Then came my college soccer training a few years later. Hitting the road on a bike for endurance training changed my perspective. Wind resistance became a real force, and those seemingly insignificant tweaks by the road cyclists suddenly made perfect sense.

Tax Drag

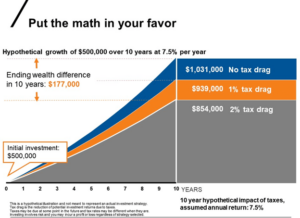

As investors, we talk a lot about investment returns. But while the gross return is fun to tout, what really matters is our after-tax investment return.

If my investment made $2 last year but the tax bill was $1, my wealth increase was not $2. The after-tax return (and corresponding increase in net worth) was $1.

With the top federal tax rate at 37% and a top state tax rate in California of 14.4%, 20 miles per hour on the bike can become 10 miles per hour very quickly.

Notice the ending wealth difference in the figure below.

*Source: Russell Investments, March 21, 2024

Tax Sheltered vs. Taxable Accounts

In the investing world, there are two types of accounts: Tax-Sheltered accounts and Taxable Accounts.

Tax-Sheltered: Examples include a Roth IRA, IRA, 401(k), Health Savings Account, or a 529. As the name implies, they are sheltered from any tax burden unless you distribute money out of the account. Picture an umbrella over your money, protecting the underlying dividends, interest, and capital gains from being taxed year-over-year. With tax-sheltered accounts, you avoid tax drag.

Taxable Accounts: Common examples include Individual, Joint, or Trust accounts. Dividends, interest, and capital gains are taxed each year, thus creating the annual drag of taxes—the wind resistance against your investments.

The Basics

Like a cyclist wearing aerodynamic gear, a good starting point (depending on your liquidity needs) is to maximize (or increase contributions to) tax-sheltered accounts. Contributions might lower your current tax bill, and your investments compound without annual tax bites.

Beyond the traditional retirement accounts, some investors might utilize strategies known as the “Backdoor Roth” or “Mega-Backdoor Roth” to stuff more money into tax-sheltered accounts.

Beyond the Basics: Supercharge Your Aerodynamics

The accounts described above have contribution limits, which means high-income earners are often forced to save a significant amount in taxable accounts, exposed to the annual taxation of dividends, interest, and capital gains.

Here are a few ways you can be more aerodynamic with your taxable accounts.

Charitable giving: The statistics are clear – for most Americans, the bulk of our assets are held in non-cash forms (home/business equity, stocks, etc.). Yet most individuals who give charitably do so from cash. Donating appreciated assets (if you’ve held them for at least one year) is often more tax-advantageous than donating cash.

Individual stocks vs. Mutual Funds: Most mutual funds pay a “capital gain distribution” in December each year if the underlying securities have appreciated. Regardless of whether you’ve personally sold any shares in the mutual fund, the distributions (which are taxable) can vary widely depending on the year. Individual stocks, on the other hand, do not pay capital gains distributions. One only pays capital gains taxes if he or she sells the stock. Because of this, individual stocks tend to be more tax-efficient than mutual funds, although every situation is unique.

Asset Location: If possible, it’s generally best to place investments with significant taxable income (like bonds) in tax-sheltered accounts while keeping more tax-efficient assets (like stocks or potentially real estate) in taxable accounts.

Tax-Loss Harvesting: Being diversified means you will likely have some securities that are up and some that are down. Being careful not to overfocus on taxes and underfocus on the underlying investment, tax-loss harvesting can be an effective technique to reduce taxable income.

Municipal Bonds vs. Taxable Bonds: With current money market fund yields in the 5% range, it can be tempting to go “cash-heavy.” Yet if the cash is subject to a combined 50% state & federal tax rate, 5% becomes 2.5% after taxes, which happens to be less than the current rate of inflation. In contrast, Municipal bonds often pay lower rates of interest than taxable money market funds or bonds, yet their income may be free of state & federal income tax.

Day-Trading: With the rise of digital trading platforms, average stock holding periods have drifted shorter and shorter. According to an analysis of New York Stock Exchange data conducted by Reuters, the average investor holds shares for 5.5 months. In the 1950’s, a typical investor held onto their shares for eight years on average.

Besides being a questionable investment strategy, day trading can rack up your tax bill. Any security held for 365 days or less is subject to ordinary income, whereas long-term securities are typically subject to much lower tax rates.

Thoughtful Planning

There are many additional strategies that can help reduce your tax drag (depreciation rules with real estate investments, advanced strategies with life insurance policies or annuities, etc.), all of which may or may not be right for your unique circumstances.

Blind Spots

Every year, our team scans and analyzes hundreds of tax returns to spot inefficiencies, blind spots, or opportunities. One of our goals is to reduce the silent drag of taxes.

Blind spots are not visible to us for a reason. It often takes a proactive review to uncover them.

As you think about your portfolio, have you taken advantage of the low-hanging fruit of tax-sheltered accounts? Beyond that, have you thoughtfully constructed your taxable account to maximize not your total return but your after-tax return?

Optimizing your financial aerodynamics requires a deep understanding, thoughtful planning, and tailoring to your specific situation. But with this approach, you may be able to compound your wealth with less wind resistance.