If you’re anything like me, you like a juicy life hack. You know – those little pearls of wisdom or insight that give you an edge. And if your social media feed is anything like mine, it is filled with bio-hacks, from blue-light blocking glasses to ashwagandha supplements to vagus nerve resets. It might be more fun to write about the bio-hacks my wife is inflicting upon me, but it would be wildly off-topic and probably run afoul of our compliance team because I’m not a doctor and don’t play one on TV.

And so, I’m going to offer some hacks in the area of finance that impacts most of us – mortgage lending. NOW JUST WAIT A MINUTE. Don’t bail on this article yet. Even if you’ve paid off your house or were fortunate enough to lock a sub-3% rate during COVID, please read on. You may be able to pass this along to people in your circles who could use a little guidance. The only thing better than getting a life-hack is giving a life-hack!

In college speech class, we learn that after giving the teaser-intro (above), the next priority is to establish your ethos with the audience. You know, your street cred and authority on the topic. In this case, my credentials are that I have been a licensed real estate and mortgage broker for 20 years. I’ve been a producing-manager originating over $1 billion in loans and have run teams in CA and TX. And over that time, I’ve seen just about everything you can imagine – from the wild west days prior to the GFC in 2008 to the hay-days of negative interest rates during COVID. It’s been quite a ride, and I have wisdom to share. And so off we go…

HACK 1 – Banks, Direct Lenders, and Brokers… Oh my!

First things first – where should you go to find the best financing? This is trickier than it sounds because of all the options consumers have. They can choose from big brick-and-mortar banks, non-depository mortgage-only banks, or independent mortgage brokers. There are nuances to each, but generally, I recommend finding a well-established mortgage broker to work with. There are three major reasons for this:

- Brokers are not captive to a single funding source, so they have more optionality in rate selection and loan structure/execution.

- Broker incentives are directly aligned with client motivations because they ONLY make money by closing mortgage loans. Banks and direct lenders have other revenue streams and are often not as “hungry” to put your deal together. Banks will often leverage the perceived equity of their name-brand to offer higher rates to supplement revenue when other parts of their business are lagging. The big “one-stop shops” have a lot of expenses to cover, and they are passed onto consumers.

- Brokers will generally execute a more efficient, user-friendly process because they are not beholden to the additional guidelines banks and direct lenders often impose on borrowers.

The possible exception to this hack is for jumbo loan borrowers at the high-end of the market. For clients with significant liquid/investable assets, some big brick-and-mortar banks offer rate incentives contingent upon assets being banked with them. This involves trade-offs because those liquid assets may be better invested elsewhere. However, this can be an advantage in certain situations.

HACK #1: ALL THINGS BEING EQUAL, WORK WITH A BROKER

HACK 2 – How Rates Are Quoted

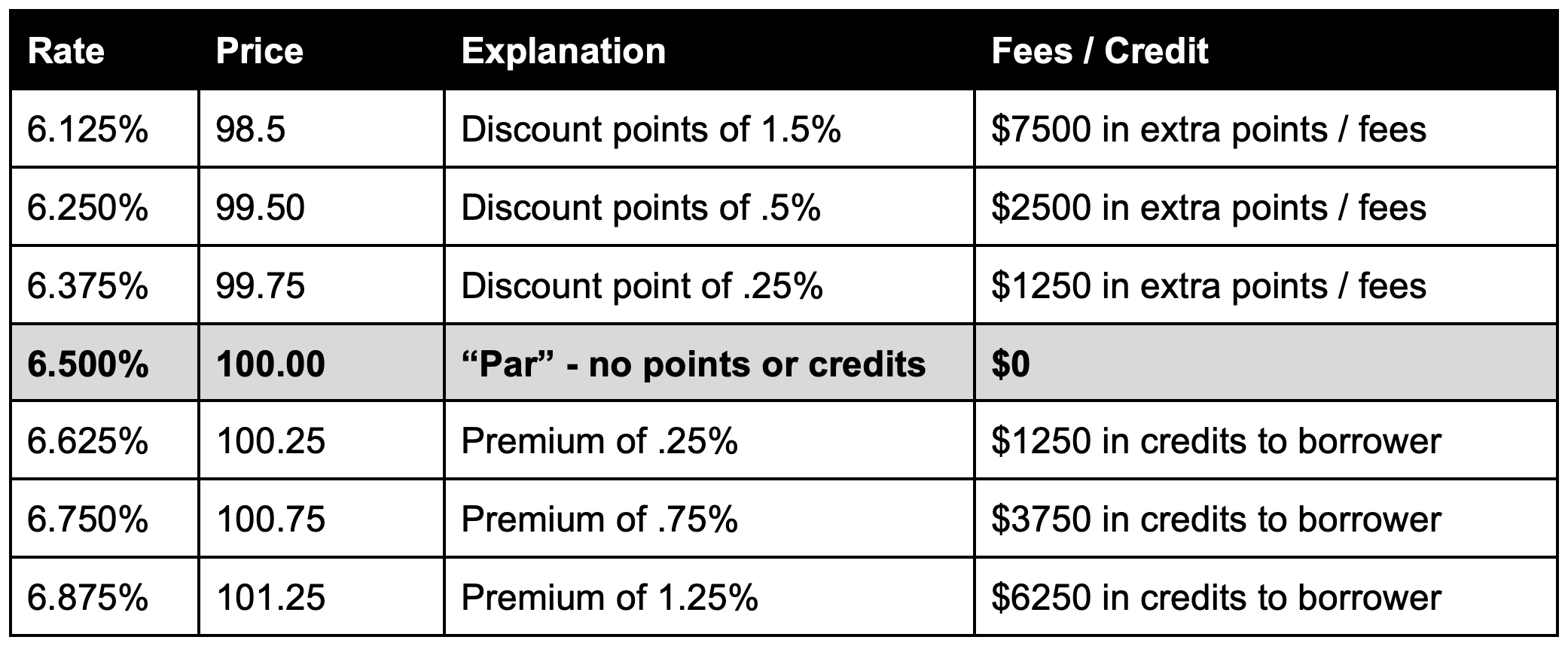

One of the most important things for people to understand is that when a loan originator is evaluating rate options for a borrower – there is NOT ONE rate to offer. In fact, there is a range of rates available based on the risk-adjusted profile of their scenario. Let’s start by understanding the concept of the range of rates. Originators see pricing tables for every borrower scenario that show:

- Par Rate: This is the central “going-market rate” on a particular day

- Discount Rates: A range of rates lower than par that require upfront “discount points” (fees) from the borrower to the lender.

- Premium Rates: A range of rates above par that generate monetary credits from the lender towards borrower closing costs.

So, for a particular loan term – say 30-year fixed – a lender sets their “par” market rate for a super low-risk situation. Let’s say that par rate is 6% – with no discount fee points from the borrower and no premium credits from the lender.

Next, a borrower’s individual risk is measured by two primary factors – their mid-FICO score (more below) and their loan-to-value ratio (the debt/equity in the deal). These risk factors result in a “rate adjustment.” For example, let’s say someone has a 680 FICO (not terrible, not great) and an LTV ratio of 80% (also not terrible, not great) – resulting in a risk adjustment of .5% to the par market rate. The central “par” rate for that borrower’s risk profile is no longer 6% – it is now 6.5%. Their rate table is adjusted higher for greater risk.

The risk-adjusted pricing table (680 FICO / 80% LTV) the originator sees might look like this for a hypothetical loan amount of $500,000:

For Illustrative Purposes Only

I apologize for going into math, but I hope you’re hanging in there with me. The principle is that you want to understand your risk-adjusted table to understand your range of rate options. If you’re going to be in the home/loan for the long haul, it may make sense to pay discount points for a lower rate. Conversely, if you’re not sure how long you will be in the home or if you’re tight on cash, it may make sense to take a higher rate to offset loan costs.

The point is that it is helpful to know that there is not just ONE rate available to you. Just because a loan originator is quoting a rate with discount points – that doesn’t mean it is “the best rate.” The best rate isn’t always the lowest because of the extra costs associated with it. Sometimes the best rate is the one that offers lender credit to offset closing costs. As Trevor loves to say, “It depends.”

HACK #2: ASK TO SEE YOUR SPECIFIC RATE RANGE / TABLE

HACK #3 – Lender Paid vs. Consumer Paid Originator Comp

Now we’re really going to tumble down the rabbit hole. When an originator (especially a broker) quotes your rates, they have a choice of how to structure their own compensation. Specifically, their compensation can be paid directly by the borrower through closing costs, OR by the lender they broker the loan to. What is the difference?

- Borrower Paid Compensation: The borrower is offered the raw risk-adjusted market rate table (see above) and is charged an origination fee on their closing costs – normally 1-2% of the loan amount. This fee can be paid out-of-pocket by the borrower or added to the loan amount.

- Lender Paid Compensation: The borrower is offered a rate table with higher rates that embed the originator’s compensation within the rates offered. The broker’s compensation is shown as a lender credit (rather than a fee) on the closing statement and keeps upfront financing costs low.

The priority here is to understand which compensation model the broker is using – and I tend to favor borrower-paid compensation if optimizing your rate is the primary goal. However, if you are tight on cash to close and/or don’t want to add to the loan amount, lender-paid compensation is a great way to keep fees low. This should be discussed openly with your broker, not hidden from view.

HACK #3: UNDERSTAND THE BROKER COMPENSATION PLAN AND WHICH RATE TABLE IS BEING APPLIED

Hack 4 – YOUR FICO SCORE

This deserves its own TOM article, but it is important to keep a handful of things in mind. First, the credit scores individuals can see for themselves are NOT the same as what a mortgage lender sees. It turns out there are different credit scoring models with different results depending on who is asking. If an individual consumer makes a credit inquiry, they get a consumer inquiry score. If an auto dealer makes a credit inquiry, they get an auto dealer score. And if a mortgage lender makes an inquiry, they get a mortgage lender score. And guess which one will be the strictest? You got it – the one with the most risk – the mortgage lender inquiry.

This is important because it is not unusual for borrowers to think their FICO score is 720, but when it is run for a mortgage lender, it comes out to 690 or something like that. It is not always wildly different, but keep your expectations in check. Just because a website says your score is “x,” take it with a grain of salt.

Second, each borrower will get three scores – one from Equifax, TransUnion, and Experian. Lenders go by the mid-score of the lowest borrower if there are multiple borrowers (for example, a husband and wife), The scores are not averaged, and one bureau is not favored over another. It is just a straightforward case of using the lowest mid-score as the benchmark for the risk profile.

Third, the reality is that once your FICO score is over 740, you are generally in the optimal risk bracket relative to FICO scores. Congratulations on having a score of 800+, but it doesn’t really matter from the standpoint of your risk-adjusted rate table. I suppose you could create a congratulatory plaque and hang it in the living room, but alas, that is about all it is worth when it comes to mortgages. This is not to disparage people with high FICO scores – it is just a reality check on how much a super high score moves the needle.

Finally, beware of FICO repair schemes. There are legitimate ways to bring your score up in a relatively short period of time. For example, if you can bring your credit usage on each card under 30%, you can probably see a meaningful jump in your credit score. But if someone is offering to magically jump your score by 100+ points for a fee… I would generally advise against it. The best way to repair your credit is to legitimately clean up any debt messes that are out there.

HACK #4 – EXPECT YOUR MORTGAGE FICO SCORE TO BE LOWER THAN WHAT YOU SEE ONLINE

Hack #5 – Online Rates and Liar’s Poker

I know it is hard to hear this, but don’t believe everything you read on the interwebs. Believe it or not, a lot of companies are creating click-bait, so you go to their website and get into their ecosystem. We all like the instant gratification that comes with Amazon Prime-like services, but in this case, I urge you to practice a little patience.

The reality is that while there are a ton of regulations governing how mortgage advertising is supposed to work, they are not well policed or enforced. If you’re tempted to click on a banner ad showing some low rate – or even if you go to a more sophisticated rate comparison aggregator, remember that this is usually an online game of Liar’s Poker. The game is to get enough consumers to go deep enough into a pre-application process that they hesitate to start over. It is a skillfully applied version of the sunk-cost fallacy, but I digress.

Your best bet is not to try to click through ads or sites to price your scenario. I can almost assure you that the result will not be where you started. Instead – find a solid broker through a personal referral or your professional network. Most good brokers will be happy to do an initial consultation with some solid back-of-the-napkin numbers to establish a reliable reference point. If the broker is worth their salt, you’ll know it because they will make some of these issues plain to you. The best brokers are not order-takers – they are consultants who will educate you on your options and guide you based on your priorities. When you find that kind of broker, you’re probably in the right place and will be well taken care of.

HACK #5: USE A BROKER TO GET YOUR BEARINGS, NOT ONLINE CLICK-BAIT

A Final Word…

This was a lot to digest, and there are more issues that deserve discussion. In the interest of time and space, I would like to give a final pseudo-hack for those who are on a home-financing journey. Notice the difference between mortgage originators who are simple order-takers / clerks and those who are professional consultants. The former will simply quote numbers – rates, fees, points, etc. The latter will take time to ask good questions and provide the “why” behind their recommendations. If you find yourself in front of a simple order-taker, politely move on and find a more skilled person to guide you. There are large and important decisions to be made, and you want to feel empowered to make them well.

Here’s to cutting to the marrow on money matters. Until next time, this is Bonecutter signing-off.

Brett Bonecutter

Private Wealth Advisor