On A Mission

If you live in South Orange County (California) and you are involved in Youth Ministry, there is a good chance that you’ve attended a short-term mission trip to Mexico.

If you attended high school in California and you were required to take a second language course, there is a good chance that you took Spanish.

I check both of those boxes.

These short-term mission trips have ranged from helping to build homes, serving at orphanages, or even hosting local youth events. I’ve helped lead many of these trips, and most of the attendees were high school and college-age students.

¡Ay, Caramba!

Now for a funny story…

Students with very little Spanish training will try to stretch their language-competency and engage with the locals during these trips. Often the most significant mistakes are just poor sentence structuring or conjugating verbs erroneously. But there is one story that comes to mind where the message was definitely lost in translation.

A young woman, a friend of mine, who was in college at the time, was in discussion with one of the workers working alongside in a construction project. As you can imagine, with a limited Spanish vocabulary comes a very limited set of topics one can discuss – weather, hobbies, likes, dislikes, etc. The young lady intended to say to her fellow worker that it was a hot day and that she was definitely starting to feel the temperature. Based on how these words translated to Spanish, she actually said it is not appropriate for TOM – this is a family-friendly blog. Let’s just say that she insinuated about herself something similar to how we’d describe in English that a “dog is in heat,” an eagerness to mate.

Obviously not her intent, but often what is said and what is heard is not always the same thing, whether we are speaking the same language or a different language.

Today, we will discuss how investors and advisors face this same lost in translation issue.

Advisors are from Mars, Investors are from Venus

When an advisor is seeking to decipher a clients risk profile, the advisor might ask a question like,

“What is your risk tolerance?”

Now, let’s look beyond the words in this inquiry and discuss what the advisor means by this question and what the investor actually hears when asked this question.

For investors, the word “risk” is a trigger word. Investors associate risk with sky diving and gambling. When the advisor asks, “What is your risk tolerance?” the investor hears, “How comfortable are you with losing some or all of your money?”

But, what did the advisor really mean by this question? The advisor means to say, “How negative do things need to get before you bail on your investment plan?” Advisors seek to understand an investor’s “breaking point” because the advisor knows that the key to success is one’s ability to stick to one’s plan.

This risk conversation lacks clarity. The advisor wants to know if the client will endure, and the client thinks the advisor is asking them about losing money. The discussion becomes lost in translation.

A Compounding Problem

Here’s the problem, the advisor will use the answers to these misunderstood risk questions to dictate how the entire portfolio is designed – yikes! Furthermore, this portfolio allocation will have a compounding negative impact on the client’s financial plan, as long as the two parties – client and advisor – continue to miss on this communication.

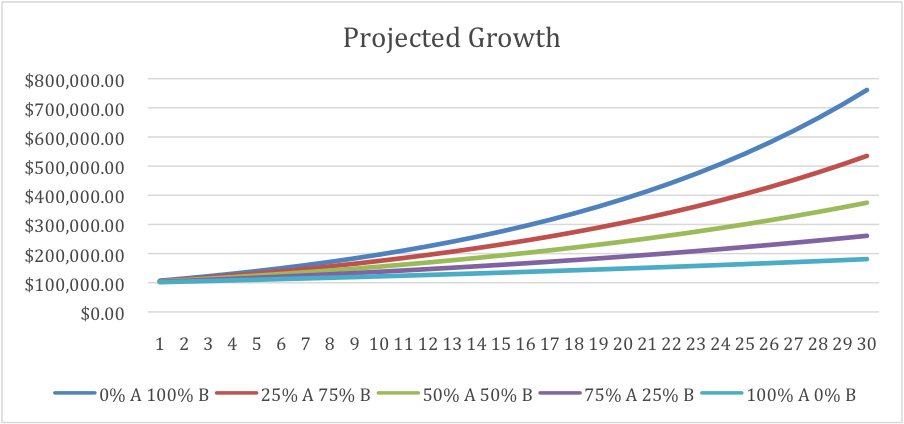

For a hypothetical, let’s assume two investment choices – “Bucket A” and “Bucket B.” Bucket A investments have stable prices and have a low expected return; let’s assume 2%. Bucket B investments have unstable prices (high volatility) and have a higher expected return; let’s assume 7%. After the client and advisor have their risk conversation, a portfolio is designed with a portion of each investment.

Here are 5 different potential portfolios that could be designed based on how that risk conversation goes:

| Portfolio | Bucket A | Bucket B |

| 1 | 0% | 100% |

| 2 | 25% | 75% |

| 3 | 50% | 50% |

| 4 | 75% | 25% |

| 5 | 100% | 0% |

As you will see in this graph, the outcomes of these portfolios over 30 years will be very different:

If an investor could choose their strategy in hindsight, they’d all choose the portfolio with the highest outcome. Still, I assume we all know that the path to that outcome won’t be as smooth as what is depicted in our simple hypothetical graph.

This is why the conversation about risk needs to go deeper than the surface questions about whether someone is conservative, moderate, or aggressive.

Clarifying Expectations

So much of what causes fear around investing is the uncertainty of it all. Investors desperately want someone to tell them what the future has in store, and they want this message delivered with the highest conviction. Yet, no one – and I mean no one – knows what tomorrow has in store. The best we can do is to have a deep and intimate understanding of history and use that to guide our expectations.

It seems like the entire finance industry wants to define risk as volatility – the up and down movements of prices – but as we described with our investor and advisor, this isn’t really what we interpret as risk. For the client, risk means losing it all or running out of money – that’s risk. For the advisor, risk means the investor makes an emotional decision (often driven by fear or greed) that derails their financial plan, leading to losing it all or running out of money – that’s risk.

Risk is not unique to just investing, and we deal with risk daily. We typically manage risk by creating coverage or insurance that provides a safety net if we experience an unfortunate outcome. Professional football teams have backup quarterbacks, and you and I have car insurance – both of these solutions are built as a safety net.

Building in Redundancies

If we agree that the real risk is losing some, all, or running out of money, let us discuss how we can solve it. After building a well-diversified investment portfolio, we need to understand that there will be some level of price fluctuation (volatility) to this portfolio. Let there be no uncertainty about it – there will be up and down gyrations with your portfolio. The reward (return) associated with investing is compensation for your willingness to accept (endure) these fluctuations.

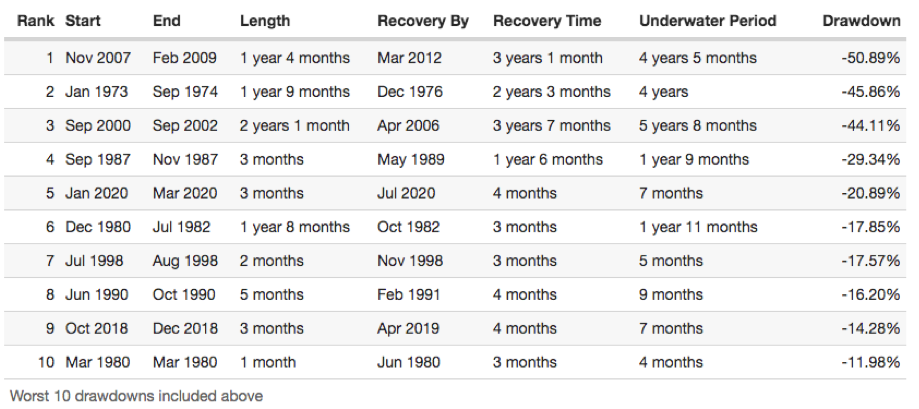

We typically don’t mind volatility when it’s trending upward; it’s the downside that bothers us. In investing, we measure how deep the price drops from its former highpoint, and we call that measurement a “drawdown.” When an investment is climbing its way out of that drawdown, we measure the time elapsed back to breakeven, and we call that a “recovery period.” For a well-diversified equity (stock) portfolio, we can use history as a guide to understanding how deep these drawdowns can be and how long these recovery periods have been in the past. Let’s take a look:

Source: Portfolio Visualizer

Again, history is used just to provide context. A future event could very well surpass the magnitude of a former drawdown and the length of a previous recovery period – records are constantly being broken. The chart above, representing the last 50 years of the US equity market, shows us that the largest drawdown was 50.89% and the longest recovery period (labeled underwater period) was 4 years and 5 months.

When building your portfolio, you should decide upfront what the maximum drawdown you are personally comfortable with. Clarify that with your advisor and build guardrails into your portfolio’s design with the expectation of not breaking that drawdown threshold. This discussion will also lead to a dialogue about how long the expected underwater or recovery period would look like for your tailored portfolio. Again, so much of this is setting the expectations upfront, so that you are not surprised when the inevitable happens.

Next, you build in safety nets. Just like we talked about earlier, you need a backup quarterback. You have a general idea of how your investment portfolio will behave, and you need some “safety redundancies” built into your plan. Let me give you some examples of the “safety redundancies” I have built into my personal financial plan:

- I have sufficient cash on hand (emergency fund) to cover 6 months worth of expenses

- I have a line of credit with sufficient coverage to cover an additional 12 months worth of expenses

- I have an investment portfolio that generates approximately 4% income (dividends and interest) that can be withdrawn without needing to liquidate positions

- I have the majority of my non-retirement investments in highly liquid securities that could easily and quickly be converted to cash if an emergency were to arise

From my perspective, I know investing can sometimes feel as scary as swinging in the air on a trapeze, so it is comforting to know that I have three or four built-in safety nets in case I miss the bar.

Take a Hard Look

I want to reiterate a point I made earlier, the finance industry does you (the investor) a great disservice by confusing volatility and risk. Again, volatility is what you accept in exchange for returns – you should welcome volatility. An obsessive focus on volatility is missing the forest for the trees; volatility is obvious in the present but nearly indistinguishable when looking back at a meaningful period of time.

The real risk that you need to be careful of is… you. You are the conductor, the captain, the el jefe, and you call the shots. You are the most likely person to disrupt your financial plan.

So, it would be best if you prepared yourself. You need a clear understanding of what to expect from your investments – you need context around what type of drawdowns should be reasonably anticipated, how long recovery periods may be, and what realistic return expectations are. Surprises and not meeting your expectations are typically precursors to risky modifications to your plan.

If you don’t feel like you have clarity in some of these areas, that’s ok. Seek out that clarity today, reach out to your advisor, and start the discussion. So much of your success will depend on crafting an appropriate plan, designing a fitting portfolio, and committing to stick to that plan/strategy for the long run.

If you have questions or comments about today’s discussion, feel free to reach out to me at . And, of course, I will be back next week with more of my Thoughts On Money.