Have you ever played the memory game? I am sure you have. It comes in all different formats, but the basic premise is that you have a collection of cards face down, organized in rows and columns. During each player’s turn they get to flip over one card and then another and if they make the match they pull the cards off the board. This was a childhood favorite of mine and I look forward to playing this with my son when he’s old enough.

Such a simple game, but it seems to beat the test of time as its popularity doesn’t fade. People like matching things. I am sure you have that friend who loves to play cupid and match friends together or the entrepreneur friend who is the connector and always has an introduction for you or perhaps you even have a favorite cheese that pairs oh so nicely with that certain bottle of wine. There is just something innate and or fulfilling about realizing that this, goes great with that.

As you might have guessed, this is not going to be an article about the art of matchmaking or a how-to on networking or even a wine and cheese review. Today’s issue of TOM is all about how you match the right account to the right goal. The idea is to fund certain types of accounts that provide the greatest benefit for the stated future goal. Today’s lesson will be very practical and applicable, and as always, all questions are welcome. You can reach me at . Ok, so off we go…

More Accounts & More Goals, Doesn’t Always Mean More Benefits

As you can imagine, being a financial planner, I review a lot of accounts. What I have learned along the way is that each person has their own style and format for organizing their financial life. One common theme that I see amongst these reviews is that people are really good at earmarking accounts for different future goals. Accounts for vacations, accounts for taxes, accounts for their kids, accounts for a future home purchase, etc. etc. etc. This is great for segregating the accounts and easily measuring your progress towards that goal, but it doesn’t provide many benefits beyond that. These are often just basic bank savings accounts with the account titles customized to reflect a goal e.g. “Vacation Savings.”

I mentioned earlier that I was a big fan of the memory game when I was a kid and I suppose that passion for finding that right match has been refocused towards financial planning. We all have our own unique goals, but we also have a lot of goals that share a common thread: future education costs, charitable giving, saving for medical expenses, etc. Today we will use these three examples to show why matching goals to the right account type is important. The take away from this is simple: for each goal we have, we should seek the vehicle (account type) that yields us the greatest benefit.

Note that these are meant to be examples and not recommendations. It is best to review options with your trusted financial professional before implementing any changes.

Example #1

GOAL: Funding future college expenses

ACCOUNT TYPE: 529 Plan

BENEFITS: Tax-free growth and tax-free distributions for qualified college expenses (some states provide additional benefits)

So, here’s an easy one, some of us have kids that we plan on sending to college. Maybe it’s not your own child, maybe a grandchild or nephew/niece. We could set aside a little bit of money each year in a general savings account and label it our “college savings” account, but we wouldn’t get much tax benefit that way would we. A 529 plan, on the other hand, is a perfect account to earmark for college savings and it does provide us with additional tax benefits.

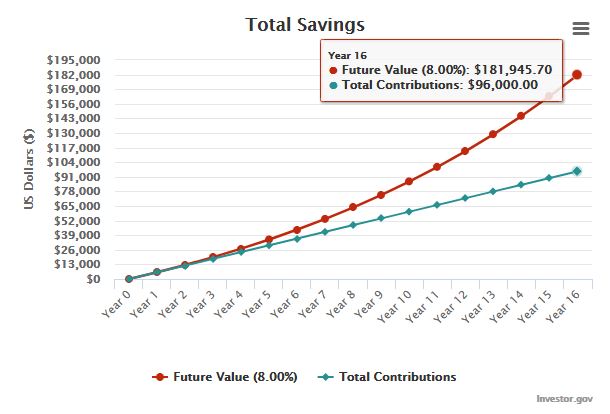

What might these benefits look like over the life of the account? Great question. Let’s say that you have a child that is 2 years old and over the next 16 years you plan to set aside some money to help them with college. Let’s say that you estimate an 8% return on the investments within your 529 plan. This is what it would look like:

Source: www.investor.gov

Your total contributions were $96,000 and the account is now valued at $181,945.70, which means you experienced a gain of $85,645.70. In a general savings account or brokerage account, these gains would be taxable, but the 529 plan shelters us from that when using these funds for college. That is a HUGE benefit and these are the type of benefits I am always looking for when matching accounts with goals.

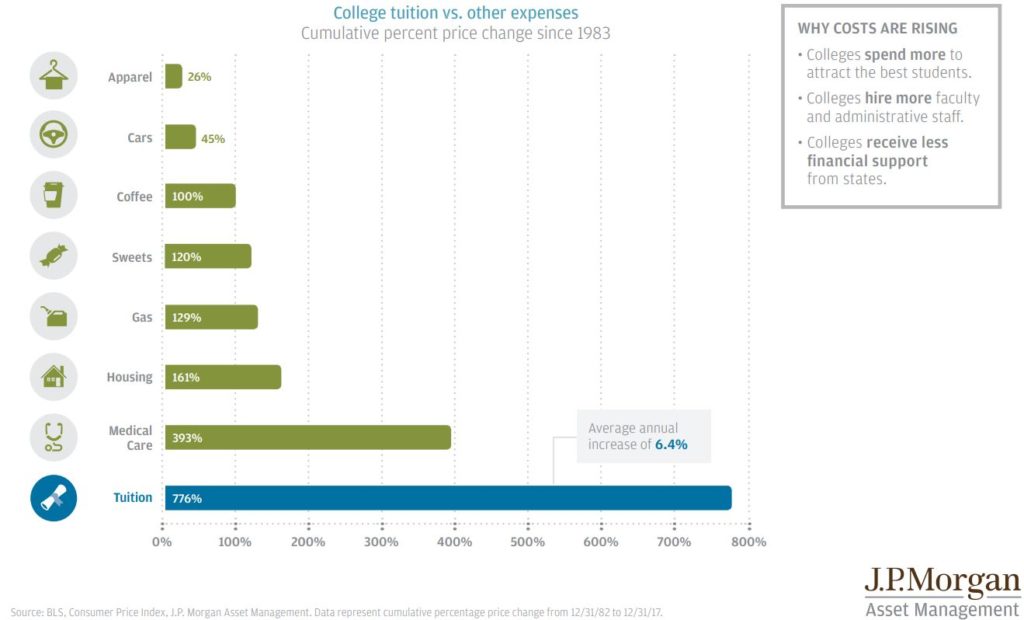

Ok, so since we are on the subject of college, if you are wondering why saving early and often is so important, check out the cumulative inflation on tuition from 1983 to 2017:

Source: www.am.jpmorgan.com

Example #2

GOAL: Giving to charity

ACCOUNT TYPE: Donor Advised Fund

BENEFITS: Ability to receive tax benefits now and assign gift later. Provides one organized record and receipt of giving.

Raise your hand if you love tax season! I hope a majority of us did not raise our hand. It can be a stressful time and just preparing can be so time-consuming. In the past, one of the most annoying things for me was having to organize and collect the giving receipts from the organizations I donated to. This would range from a school jogathon to my church to a local non-profit, and for those of us that itemize this is a headache.

So, here it is again, I had a goal and I was just in search of an account that would provide me the most benefit for that particular goal. The Donor Advised Fund was a great solution. This account allows a donor to fund the account, receive the tax benefit now, and grant the money to a public 501(c)(3) today or in the future. For a finance nerd like me, I also enjoyed the fact that the money could be invested and grow, as I was deciding where I wanted to grant it.

Oh, and the tax receipt “headache” I mentioned above – solved! By running the donations through the Donor Advised Fund, you are able to create one central record and receipt for all the donations. Giving is such an enriching experience, so it was nice to remove some of the hassles.

Example #3

GOAL: Paying for future healthcare needs

ACCOUNT TYPE: Health Savings Account (HSA)

BENEFITS: Tax deductible, grows tax-free, distributes tax-free for qualified medical expenses

One of the biggest concerns for a lot of retirees is how they are going to cover future medical costs. Some may want to retire before Medicare and others may have needs that go above and beyond the future coverage they have allotted to them. This can be a scary thought exercise because it seems like medical costs have no ceiling but who wouldn’t spend what they needed to if a family member needed care.

So, is there a way that would help fund this future need and provide us with some extra benefits? You betcha! For those of us that have medical benefits that the IRS deems a “high deductible” plan, we can contribute to a Health Savings Account. As the descriptor above explains, your contributions to these plans are deductible, the investments within the account grow tax-free, and the distributions are tax-free when they are used to cover medical expenses. Within the industry, this is often touted as the only “triple-tax-free” account. Another less known benefit is that after the age of 65 you can withdrawal from this account for non-medical expenses and although this will be considered taxable income, there is no penalty.

Now, to avoid being redundant I would direct you to Example #1 where both graphics are relevant to this example as well. The compounding growth of an HSA will provide HUGE tax benefits over time, much like the 529. Additionally, do you know what the second highest inflation category was behind tuition? Yup, medical expenses.

Summing it all up …

My intention for this article was to choose three very diverse goals. The idea was that these goals, common to many of us, would be met with a planning technique that provides better solutions and more benefits in the end. As I mentioned, this list was far from exhaustive and know that there are countless planning strategies that can be implemented for a large array of different financial goals, which is why this topic is so important. Again, see a skilled advisor for a customized solution for you.

The examples are not intended to be definitive recommendations, as they each have some nuances that should be considered – their own list of pros and cons. The whole point is finding the right tool for the right job. I suppose you could hammer in a nail with a wrench, but I think we’d agree that the hammer is probably a better fit. While that analogy would be easily considered as common knowledge, financial planning requires a bigger tool kit!

I will end this entry with the advice I often provide, today’s subject matter makes for a GREAT conversation with your trusted advisor, whoever that might be. Having the right tools for the job is sometimes the most important part of getting the work done 😊

This is TOM signing out, until next time, friends.