My Friend Reggie …

He’s a great guy, works hard, good saver, and is doing what he can to prepare his financial future. Reggie reads about investing here and there; he’s interested in knowing what’s going on in the world, but also likes to devote a majority of his time to family and work.

Reggie wants to retire in 15 years, so he reaches out to me to have a look at his investments and give him some feedback. Reggie owns a slew of different stocks – some domestic, some international, some small companies, some large companies, and ranging across all different industries. He tells me that he designed his portfolio this way intentionally; he wanted to diversify. So, I ask, “Reggie, why don’t you own any bonds?” and without missing a beat, Reggie responds, “Are you kidding me!? I’ve done enough reading to know that stocks are always better than bonds if I have 15 years until retirement.”

Reggie’s response really got me thinking. I understood what he meant by this, but any statement described with always and never are worth inspecting a little further. For the casual investor and even the well-informed professional, this can often be the assumption – stocks over bonds when the holding period exceeds 10 years. Today on TOM, we will explore whether this is always the truth, and if Reggie might benefit from owning some bonds.

And off we go…

What’s a Stock? What’s a Bond?

Let’s start off simple and learn what the difference is between a stock and a bond.

If you own a stock, then you are a partial owner of that company. If you own one share of a very large company, then your ownership may be very small, but nonetheless, you are an owner. The people working inside this company are working day in and day out to make it a better company, and as they improve the business, the value of the company grows. This value is expressed in the stock price. You, the shareholder (owner), will benefit from this growing value. That’s a stock.

A bond is much different. If you are a bondholder, you are not an owner of the company; you are a lender to the company (or government). You are giving that company your money in exchange for fixed interest payments over a stated time period. At the end of that time period, the company pays you back what they borrowed. The company will, in turn, use this borrowed money to try and improve upon their business, but as a bondholder, you are most concerned with being paid back rather than the fluctuating value of the business.

Bonds pay interest payments that are predictable. Stock prices fluctuate and are less predictable. This lack of predictability or uncertainty is often referred to as risk.

So, if stocks have more risk (uncertainty) than bonds, it would be assumed that the returns should be greater. An investor should be compensated for this elevated level of risk.

Beyond Diversification

Do bonds help to diversify a portfolio? Yes, but that is not what today’s conversation is about (see The Exercise of Diversification). Reggie said that stocks are always better than bonds over longer periods and he was referring to the returns. How about this question, do bonds ever outperform stocks for long time periods? Yes.

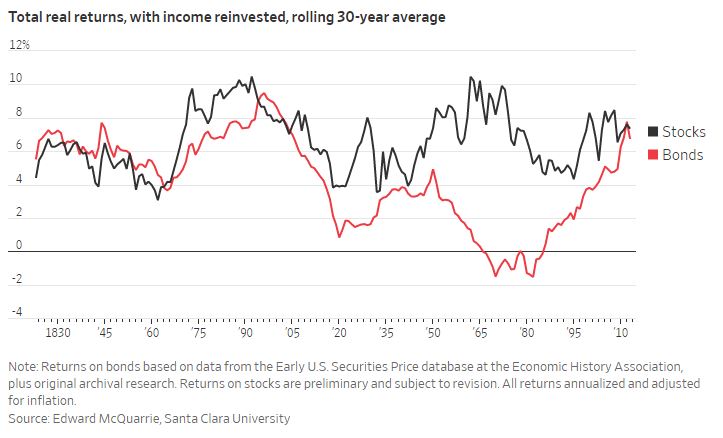

On November 2nd, 2018, Jason Zweig wrote a piece in the Wall Street Journal titled “Sometimes, It’s Bonds For the Long Run.” Zweig covers a research article written by Professor Edward McQuarrie from Santa Clara University. Professor McQuarrie’s research sought to question this idea if stocks always outperform bonds. McQuarrie’s research did differ from much of the historical research though, as he compared a diversified bond portfolio to a diversified stock portfolio. Traditional research often just compared the 10-year government treasury to a diversified stock portfolio.

The professor’s research compared stocks to bonds over rolling 30-year periods from 1823 – 2013 and found that bonds outperformed stocks about 25% of the 191 time periods observed.

Source: Wall Street Journal

What Makes Bonds Attractive

Are there some potential flaws in this research or some methods that could be challenged? Sure, this is true for all research. Here’s the key takeaway though, there will be some time periods when bonds do outperform stocks. Maybe with where interest rates are today this might not be as likely over longer periods but remember there is a BIG difference between Reggie’s statement of always and this research that documented 25% of the time bonds outperformed.

Furthermore, investing isn’t always about this performing better than that over some certain time period. There are other benefits that are additive to a portfolio beyond returns. These are the attributes that I would argue do make bonds attractive. Bonds dilute the volatility of your stock portfolio, they pay consistent fixed payments that you can rely on for your expense needs, bonds can reduce the drawdowns of a portfolio, some bonds can be more liquid than other investments, and the list goes on.

Textbook vs. Real Life

Now there is a problem with academic research – it’s not real life. When backtesting comparatives, you don’t capture any of the day to day nuances that we experience as investors. Backtests don’t have weddings to pay for and backtests don’t get spooked out of the market during recessions because backtests are mechanical, they aren’t human beings with real lives.

As our world becomes more data-driven, I have a concern that we might become too convinced about what we believe the future has in store. We may feel fully equipped to make predictions and begin to look at things through an always and never lens.

Reggie has 15 years until he is ready to retire, and maybe the textbook might tell him that an all-stock portfolio is most likely to maximize returns. But what if it doesn’t? What if we go through one of those extended time periods when stocks struggle, who is Reggie to blame? His textbook? No, Reggie is a real person and is in need of real advice. Reggie needs to know the pros and cons of each decision and understand the potential consequences.

I love the way our founder David Bahnsen describes what we do, and I think it is the perfect way to wrap up today’s conversation,

“What we do is manage money, and we do it for people – real people – and we implement plans on behalf of those people – sophisticated plans if need be. And we do it all because we love the work, love our clients, and love the capital markets.”

Reggie could have been led astray by a handful of articles he read. He may have felt extremely confident based on this research, and the outcome very well could have been detrimental for his family. For this reason, I am forever grateful for the responsibility and honor I have of helping people like Reggie steward their assets well.