Don’t Judge a Book by its Cover

A bit of a funny title for this week’s article. That gambling saying, “Playing with house money,” has two connotations – one which will apply to today’s discussion and one which will not. It primarily refers to when you are on a winning streak, and your chip stack is primarily made up of winnings versus what you bought in for. This adage can also infer being reckless with your wagers because you are playing with house money.

When your investment account compounds over time, much of it will be “house money.” This is to say that the balance will primarily consist of earnings rather than contributions. And, of course, we will not encourage reckless financial behavior so we will simply reject the secondary inference.

With that clarification, on to the show…

A Picture is Worth 1,000 Words

Have you listened to the Thoughts On Money podcast before? If not, I would encourage you to do so.

We typically have two or three advisors in the recording room, and we have an unfiltered conversation about the weekly topics covered here on Thoughts On Money. Personally, I really enjoy recording these podcast episodes. I get to use the article as a launch point and discuss some of the ideas and concepts with my colleagues/friends.

I say all of this because last week I provided a visual on the podcast that I wanted to dive a bit deeper into today. I mentioned that I grew up in Napa and spent a lot of time in San Francisco, where my parents grew up and my grandparents lived. I remember learning to drive a manual transmission vehicle in the city; that was an adventure. Steep hills plus stop signs at the peaks of those hills was not too friendly for a rookie in a stick shift.

I am a glutton for word pictures and analogies – I guess it’s just how my brain works. The visual we discussed on the podcast helped me to express two things: (1) how compounding works and (2) how your balance sheet can get away from you – grow beyond your expectations – which makes legacy planning challenging (a good problem to have, I suppose).

Anyhow, back to that visual. Imagine me shooting hoops out front on Filbert St. You have the backdrop of the bay and these near vertical hills leading the way down to the water, looking like a set of stairs built for a giant. My shot goes up, bangs the front of the rim, and that ball starts to bounce away from me. I need to act quickly; If I don’t grab that ball within a few seconds, it’s headed straight to the bay, gaining more and more momentum along the way.

This is how compounding works. It may be slow rolling in the beginning, but given enough time, the velocity becomes parabolic. As described, once that basketball gets far enough out of reach, you can consider it as good as gone. That is the second aspect of this article: wealth begins to compound faster than you can spend it, creating a snowball effect on your balance sheet. Again, it is a good problem to have, but this wealth doesn’t come without responsibility – stewardship and legacy are key here.

A Chart is Worth 1,000 Words

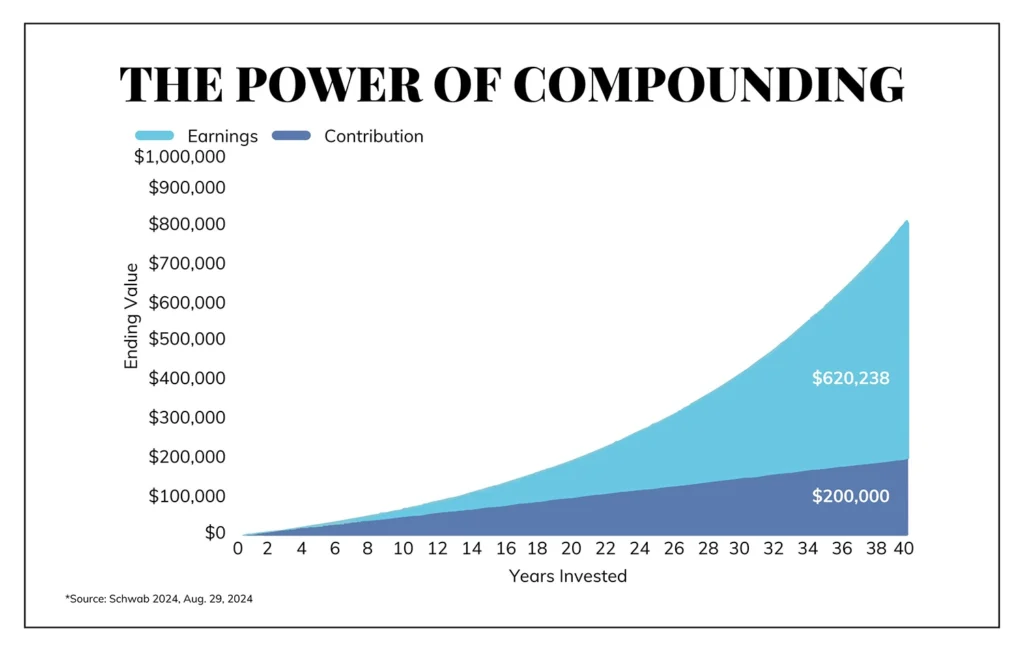

Perhaps analogies and word pictures aren’t your thing. Maybe you are more of a chart guy or gal. Let’s take a look at this impact graphically. Here (see below) is an investor saving $5,000 a year for 40 years, growing at 6% – dark blue represents the investor’s contributions, and light blue represents the value of those compounding returns. Essentially, the summation of the dark blue and the light blue represents the total value.

The main highlight here is that contributions are everything in the early years, but in the later years, the lion’s share of value is made up of those compounded returns. Specifically, 75% of the value in the end is attributable to growth.

Source: Schwab 2024

A Penny Saved…

Next, let’s take this one step further. Let’s assign some figures to help create a hypothetical that is common to what I often see. There seems to be a high correlation – from my experience – between healthy balance sheets and prudent spending habits. Call them thrifty, call them frugal, call them whatever you’d like, but it’s often this very quality that led to a savers sizeable balance sheet. There is a financial prudence that allowed these investors to (1) build wealth and (2) retain wealth.

Perhaps this is why many professional athletes and lotto winners go broke. A windfall, without the strength and experience to shoulder that wealth, doesn’t typically end well. So, in the common case I am referring to, the investor ends up with a balance sheet that dwarfs or overshadows their spending habits.

Wealth Begets Wealth

Add one more ingredient to a growing income and modest spending: time. After many years of investing, the surplus creates even more surplus.

Eventually, someone realizes they don’t have much time left, so their attention turns to legacy.

For most of these cases, I think I could’ve forecasted the trajectory of that successful 70-something when they were 40 or 50 years old. If I had a time machine, I would’ve gone back and started the discussion on legacy planning much earlier.

This is a healthy reminder that we are not immortal and that our surplus and leftovers need to be directed to go somewhere. Compounding is a beautiful thing, it acts in your best interest, but with enough time under its belt, it can get quite aggressive. Again, think snowball.

All this is to say that there is wisdom in planning early and often, when it comes to your legacy. To meditate on your desires and wishes, and to recraft your financial plan to begin fulfilling some of those legacy wishes now versus later—all beautiful conversations to have with your advisor.

Take Aways

Here’s what I hope you walk away with.

I hope today was a healthy reminder that compound interest truly is the 8th wonder of the world (h/t Albert Einstein), even if it is boring and slow-going in the beginning. Remind yourself that you are planting seeds that will bear abundant fruit in the decades to come.

Next, I hope today encouraged you to start thinking about legacy today. Whether you are 22 or 82, this topic should be front of mind. List your legacy aspirations now and see which ones you can start ticking off the list sooner rather than later. This type of planning often gets put on the back burner when it should be front of mind.

The hills are steep, trust me – don’t let that ball get too far from you.

With regards,